Industry data continues to suggest that casual dining restaurant companies are at risk of missing consensus expectations in the fourth quarter.

Knapp Track

According to Malcolm Knapp, estimated Casual Dining comparable restaurant sales growth for October 2012 was -0.9%. The sequential change, in terms of the two-year average trend from September to October, was -80 bps.

Guest counts declined -2.8% versus October 2011. The sequential change, in terms of the two-year average trend, was -55 bps. While these results are disappointing, they are not as bad as had been feared intra-quarter. We remain negative on the casual dining category.

Restaurant Value Spread

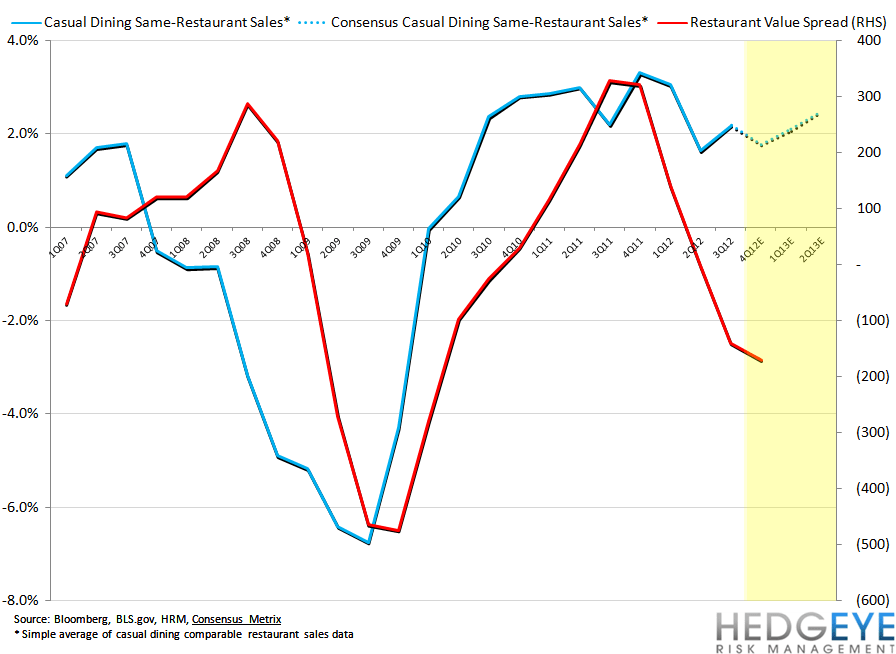

The Restaurant Value Spread, or the spread between CPI for Food Away from Home versus CPI for Food at Home, updated for October CPI data released this morning, is implying that inflation at restaurants continues to outstrip inflation in the grocery aisle. We believe this is a negative for casual dining pricing trends.

<chart1>

Takeaway

We continue to believe that consensus is far too bullish on casual dining top-line trends. Anemic real wage growth is just one of many macroeconomic headwinds that we believe merit caution going forward. Consensus is assuming a strong recovery in industry same-restaurant sales in 4Q12 and 2013. Accelerating negative declines in traffic growth suggest that trends could deteriorate further from here.

Howard Penney

Managing Director

Rory Green

Analyst