Positions in Europe: Short EUR/USD (FXE); Short Spain (EWP)

Keith added FXE to our Real-Time Positions at $127.06. FXE’s TRADE range is $126 – 128 with a TREND resistance of $131.

With regard to the trade Keith said: “The Euro bounced right where it should have, off the low-end of our immediate-term Risk Range, but remains bearish TREND.”

Our call is that the EUR/USD will trade within our quantitative levels and reflect much of the daily headline risk (from Spain, Greece, and Italy in particular), however ECB President Mario Draghi’s September announcement that “the ECB is ready to do whatever it takes to preserve the euro” and the resolve of Eurocrats to maintain the Union will prevent levels falling anywhere near parity.

POLITICS

There is still great political uncertainty in Europe right now, which lends support that the EUR/USD will not cross our quantitative long term TAIL line of resistance at $1.31. Further, we believe there is a high likelihood that no significant policy action comes in the remaining weeks of 2012. As a reminder, some of the main topics that Eurocrats are wrestling with are:

- Setting up a Banking Union (with Pan-European Deposit Insurance)

- Setting up a Fiscal Union

- If and when Spain will request another bailout (and will it come from the IMF or ESM, or both?)

In terms of setting up a Banking Union and Fiscal Union, we believe the two are dependent on each other. While more attention has been given to a Banking Union recently, we believe Eurocrats reaching an agreement on a fiscal union over the near term is incredibly unlikely as countries are unwilling to part with their fiscal sovereignty. This could be one factor to put downside pressure in the cross.

On Spain, we think the sovereign asking for a bailout is a question of when and not if. The recent rumor that Spain may look to the IMF for a loan would reflect the likelihood of more favorable terms versus the European Commission and ECB’s ‘conditionality’ for aid via the ESM or OMT.

FUNDAMENTALS

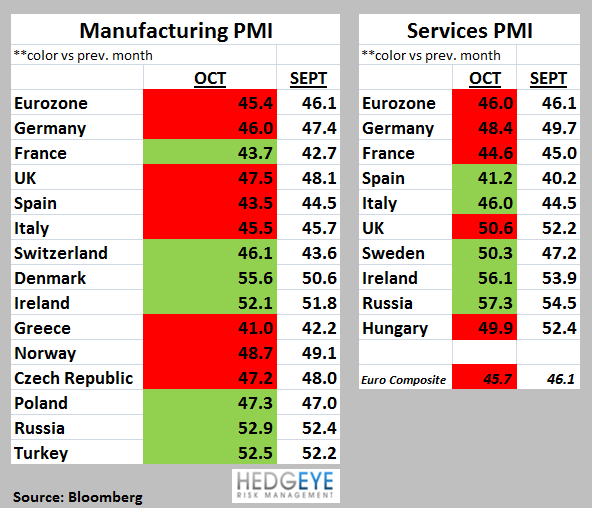

European fundamentals continue to show a down to ugly trend, looking across PMIs, confidence readings, inflation, retail sales and unemployment rates across much of the region. It’s important to note that even the perceived pocket of strength are revealing weakness, with Germany, France, and the Netherlands notable call-outs.

Manufacturing and Services PMIs for October have shown little to no improvement over the last 8-9 straight months, stuck below the 50 line indicating contraction.

Below is notable data out this week:

Eurozone CPI 2.5% in OCT Y/Y (above the 2% mandate and should remain so over the intermediate term)

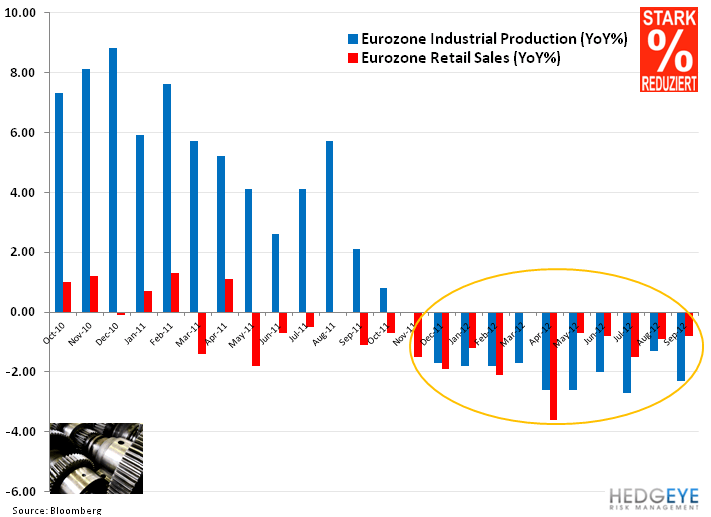

Eurozone Industrial Production -2.3% SEPT Y/Y (exp. -2.2%) vs -1.3% AUG

Eurozone Industrial Production -2.5% M/M vs 0.9% AUG = biggest drop in more than three years

Eurozone ZEW Economic Sentiment -2.6 NOV vs -1.4 OCT

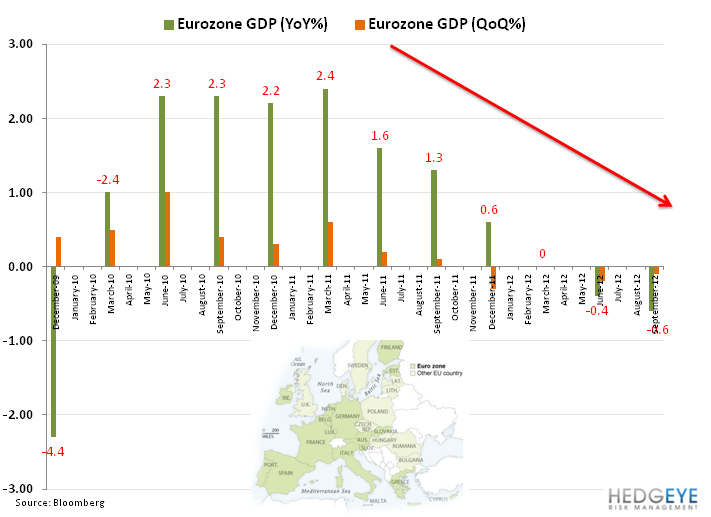

Preliminary Q3 GDP – while many of the core countries beat expectations, growth levels contracted versus the previous quarter and the Eurozone officially slipped into recession:

Eurozone -0.6% Y/Y (inline) vs -0.4% in Q2 [-0.1% Q/Q (inline) vs -0.2% in Q2]

Germany 0.9% Y/Y (exp. 0.8%) vs 1.0% in Q2 [0.2% Q/Q (exp. 0.1%) vs 0.3% in Q2]

France 0.2% Y/Y (exp. 0.0%) vs 0.1% in Q2 [0.2% Q/Q (exp. 0.0%) vs -0.1% in Q2]

Italy -2.4% Y/Y (exp. -2.9%) vs -2.4% in Q2 [-0.2% Q/Q (exp. -0.5%) vs -0.7% in Q2]

Netherlands -1.6% Y/Y (exp. -0.5%) vs -0.4% in Q2 [-1.1% Q/Q (exp. -0.2%) vs 0.1% in Q2]

Germany ZEW Current Situation 5.4 NOV (exp. 8) vs 10 OCT

Germany ZEW Economic Sentiment -15.7 NOV (exp. -10) vs -11.5 OCT

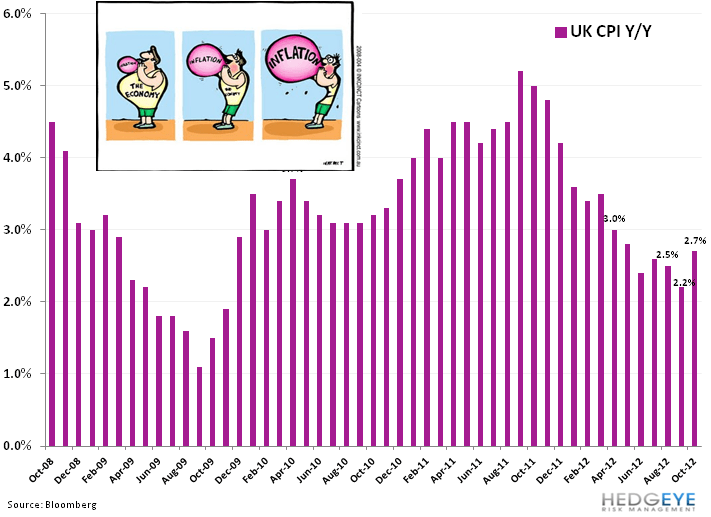

UK CPI 2.7% OCT Y/Y (exp. 2.4%) vs 2.2% SEPT [0.5% OCT M/M vs 0.4% SEPT] – stagflation, continued.

We think slowing growth, sticky inflation, and the structural flaws inherent in creating a Eurozone will continue to present challenges that should prevent appreciation of the EUR/USD above our TAIL line of resistance at $1.31.

Matthew Hedrick

Senior Analyst