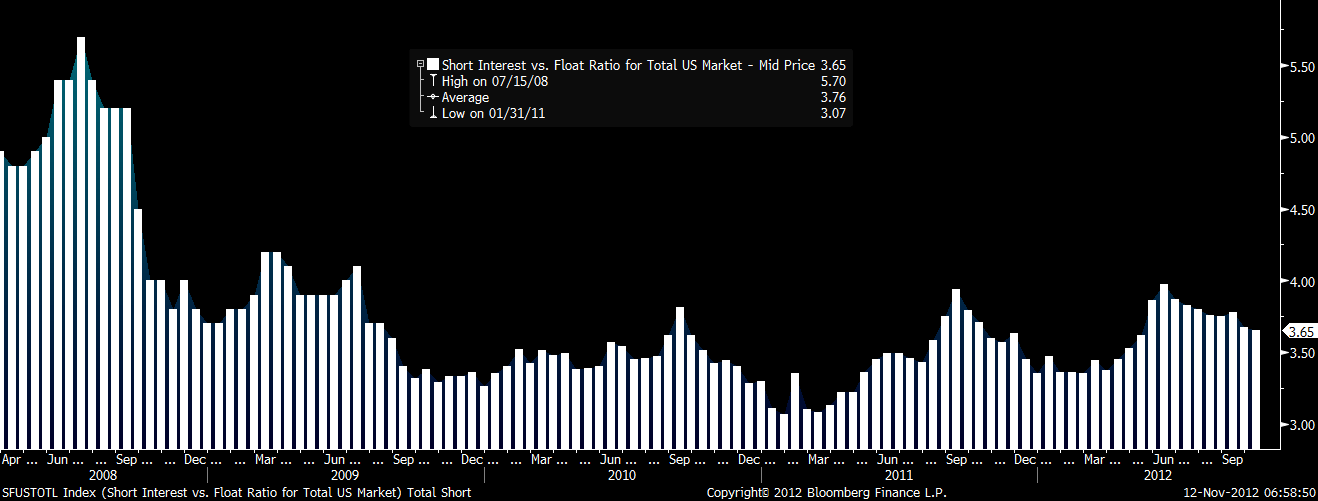

Short interest for the NYSE, AMEX and NASDAQ currently indicates a bearish overtone for stocks. For the two weeks ended 10/15 short interest for NYSE, NASDAQ and AMEX combined ticked down to 3.65% of the float from 3.67% prior. That’s the lowest ratio since the two weeks ended 5/15. We bounced off of 1364 in the S&P 500 (TAIL support) last week and are quite capable of re-testing that level this week.