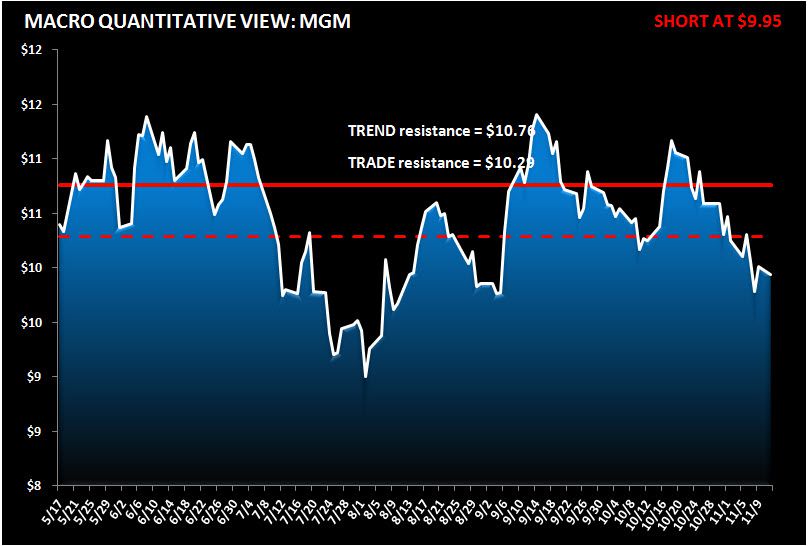

Keith shorted MGM in our Real-Time Positions at $9.95. MGM's TRADE and TREND resistance is at $10.29 and $10.76, respectively.

As MGM nears its 52-week low, we think there is further room to the downside. A difficult macro environment and a secular decline in slot demand should continue to pressure results. We're below the Street on Q4 and 2013. Slot volumes, which we believe is the ultimate barometer of the health of Vegas, have fallen in five out of the last six months. According to our trend projection model, we expect the downward trend to continue for the rest of 2012. September was up slightly but the month contained two extra weekend days - a calendar boost that will reverse in October. Management did say they are seeing better Strip trends in early Q4 but they said the same last quarter and missed expectations badly.