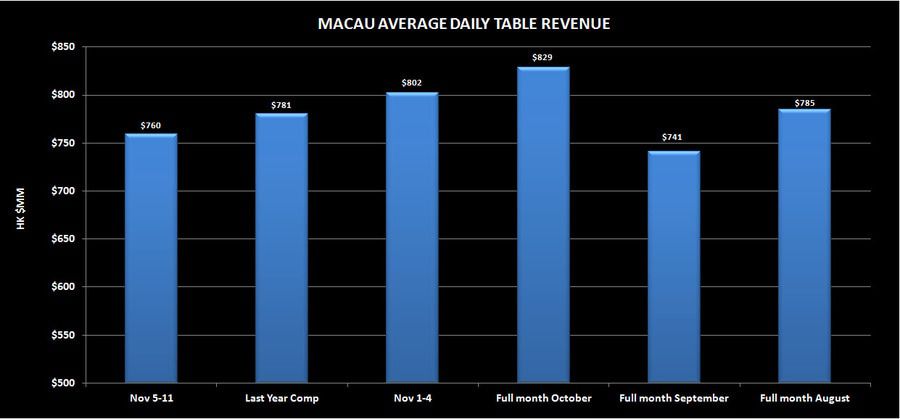

Average daily table revenues in Macau were down 3% YoY to HK$760 million. We’ve ratcheted down our monthly projection slightly to a range of 5-12% YoY growth, still an acceleration from October’s 3% growth.

While still early in the month, SJM and MGM are the clear winners here in November, both with share well above their respective October and trailing 3 month average shares. MPEL and Galaxy have been share givers thus far in November. While down from last week, LVS remains above its 3 month trend.