Key Takeaways

* U.S and EU bank swaps were wider last week, on the heels of the American presidential elections, mounting fears about the looming fiscal cliff in the United States, and renewed concerns regarding Greek austerity. In the United States the money center banks and the large brokers saw that most widening. In Europe, bank swaps were wider, led by Italy, Spain, and France.

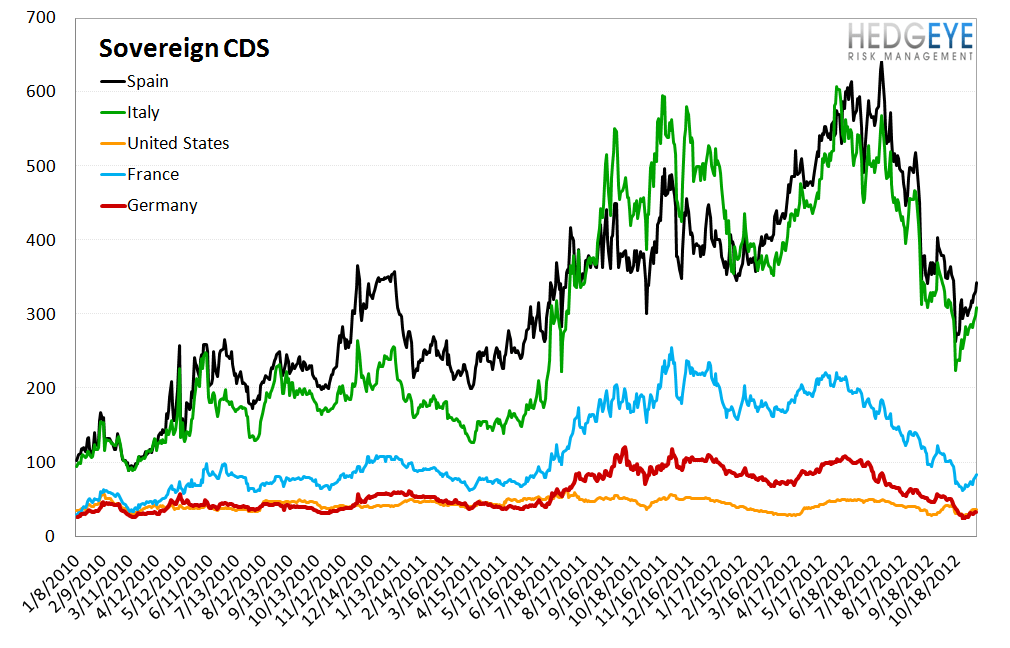

* At the sovereign level, Spain, Italy, Portugal, and France saw their swaps widen notably last week. Meanwhile, U.S. and German swaps both widened by 2 bps. Swaps in Ireland and Japan tightened, dropping by 5 bps and 7 bps, respectively.

* Rates on high yield corporate debt rose 11 bps week-over-week. For reference, this is the third consecutive week that high yield rates have been up or flat.

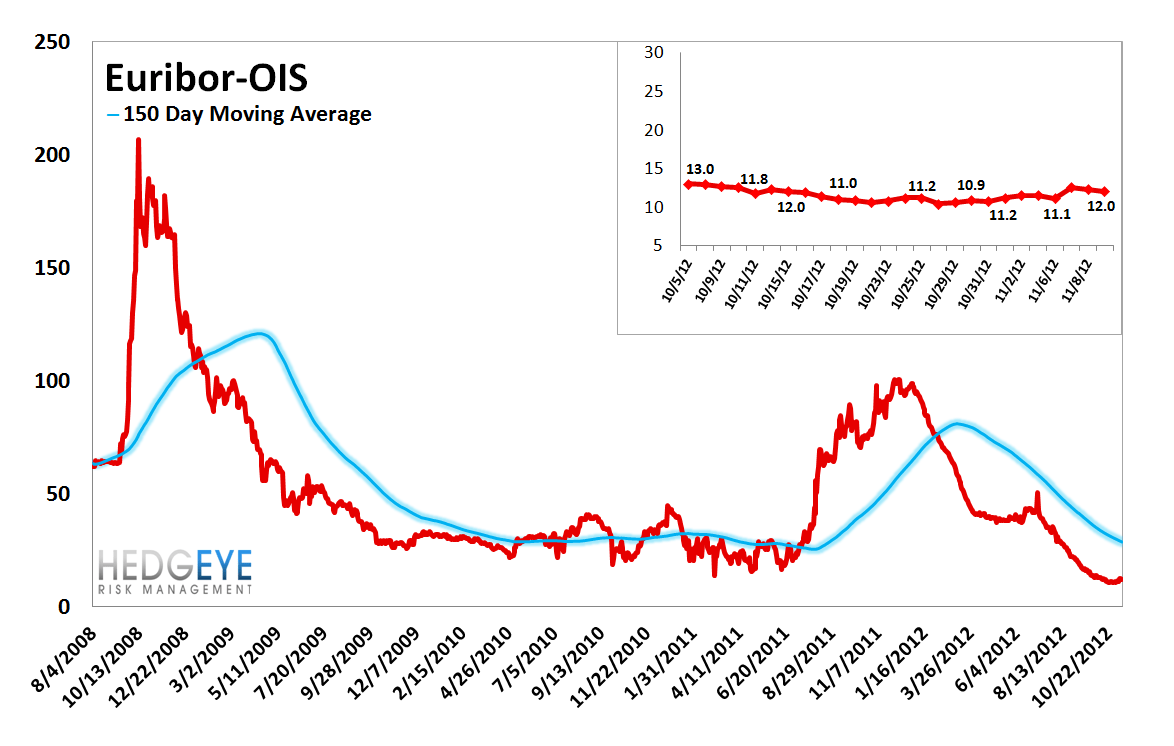

* The Euribor-OIS widened by 1 bp. This is the second consecutive week of WoW widening.

* The 2-10 spread tightened last week, its third consecutive week of tightening.

* XLF Macro Quantitative Setup – Our Macro team’s quantitative setup on the XLF shows 2.3% upside to TRADE resistance and 0.1% downside to TREND support.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 0 of 12 improved / 6 out of 12 worsened / 7 of 12 unchanged

• Intermediate-term(WoW): Neutral / 2 of 12 improved / 2 out of 12 worsened / 9 of 12 unchanged

• Long-term(WoW): Positive / 6 of 12 improved / 3 out of 12 worsened / 4 of 12 unchanged

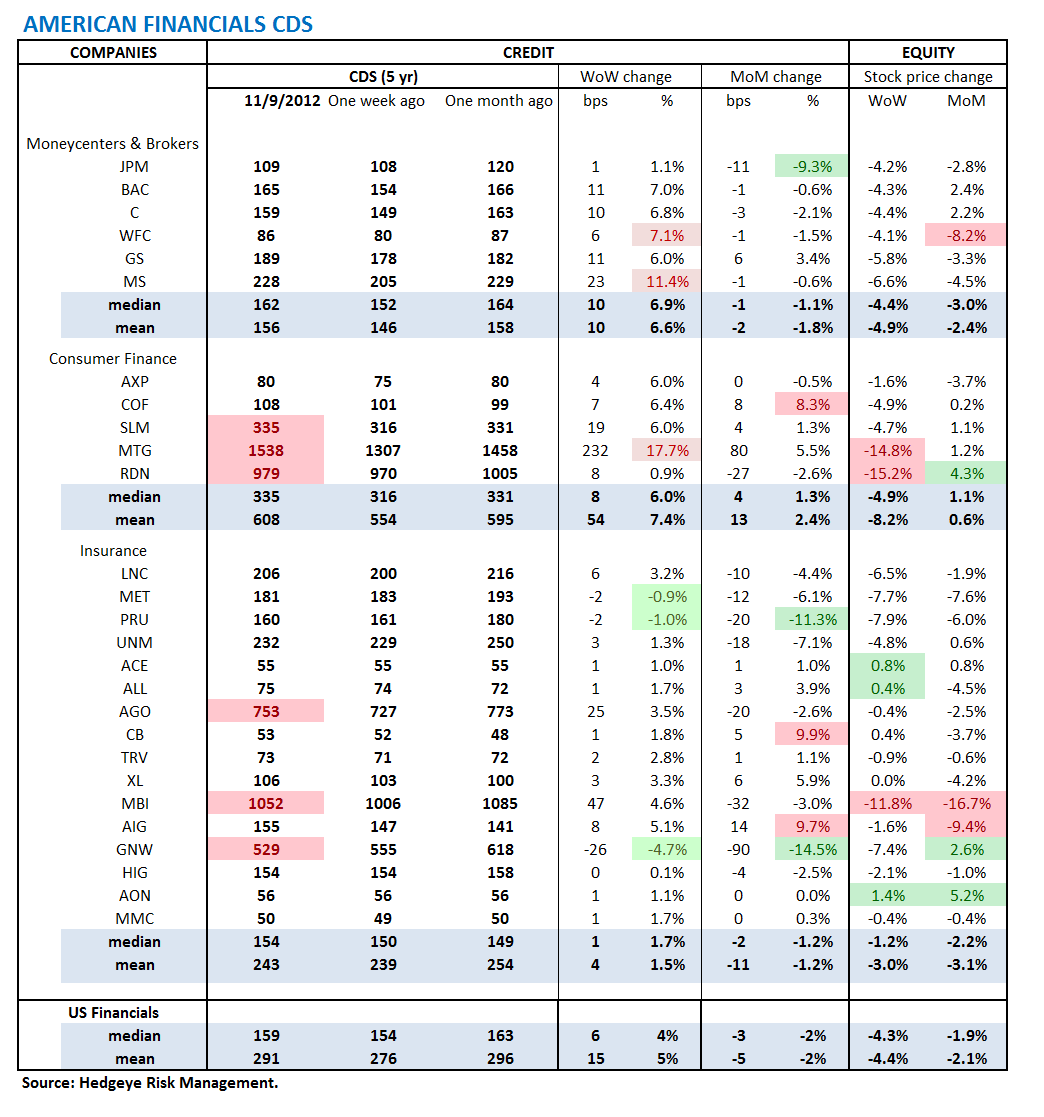

1. American Financial CDS – Big banks all saw their default probabilities increase following last week's election. Morgan Stanley widened by the most (23 bps), reflecting not just the election outcome but also renewed EU fears. Following Greece's budget vote last night, we'd expect MS swaps to cool off a bit. Overall, wwaps widened for 24 out of 27 domestic financial institutions.

Widened the most WoW: MTG, MS, WFC

Tightened the most WoW: GNW, PRU, MET

Widened the most MoM: CB, AIG, COF

Tightened the most WoW: GNW, PRU, JPM

2. European Financial CDS – European financials followed Euro sovereigns, widening wee-over-week. Swiss banks were wider by 6 bps, while Spanish and Italian banks widened by 10-32 bps. French banks widened noticeably, while German banks widened slightly.

3. Asian Financial CDS – Default swaps in Asia were uneventful last week. There were small increases in Chinese banks (1-3 bps), and 3-4 bps increases at Indian banks. Japanese financials were mixed with Nomura the largest mover at +14 bps.

4. Sovereign CDS – European sovereign swaps were wider again last week on renewed Greece concerns. The largest movers were Spain and Portugal, widening 32 bps and 67 bps, respectively. With the passing of the Greek budget last night, we would expect to see some cooling off in the short-term.

5. High Yield (YTM) Monitor – High Yield rates rose 10.7 bps last week, ending the week at 6.77% versus 6.67% the prior week.

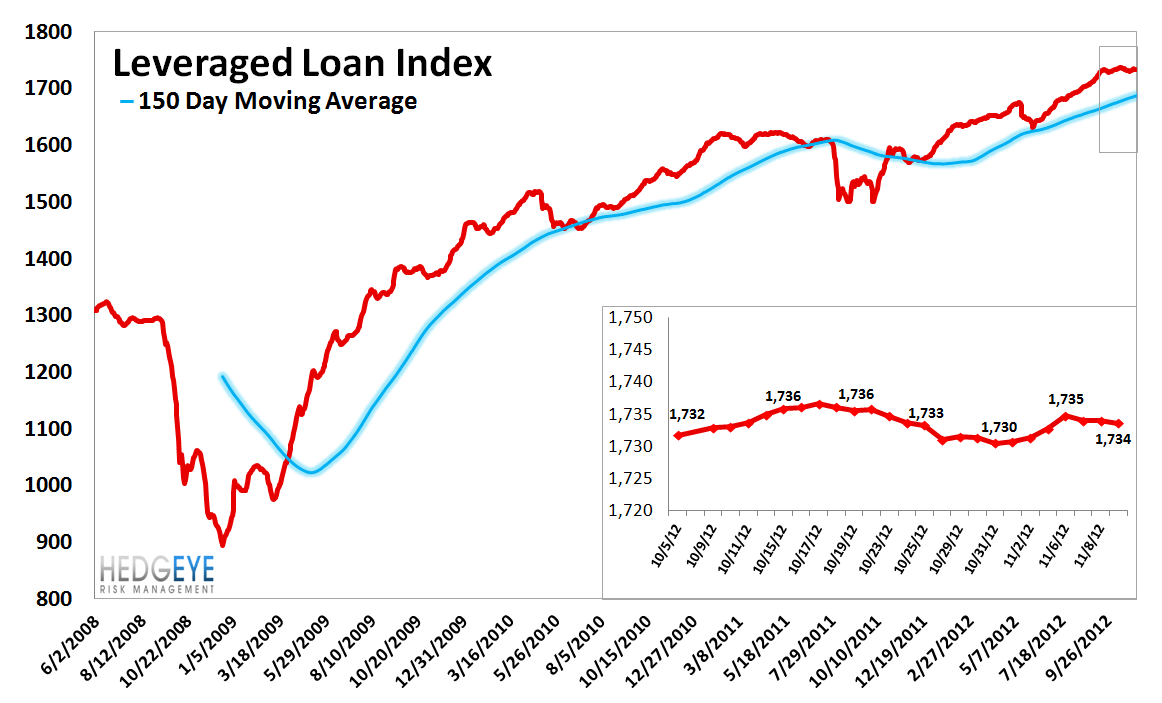

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 2.3 points last week, ending at 1734.

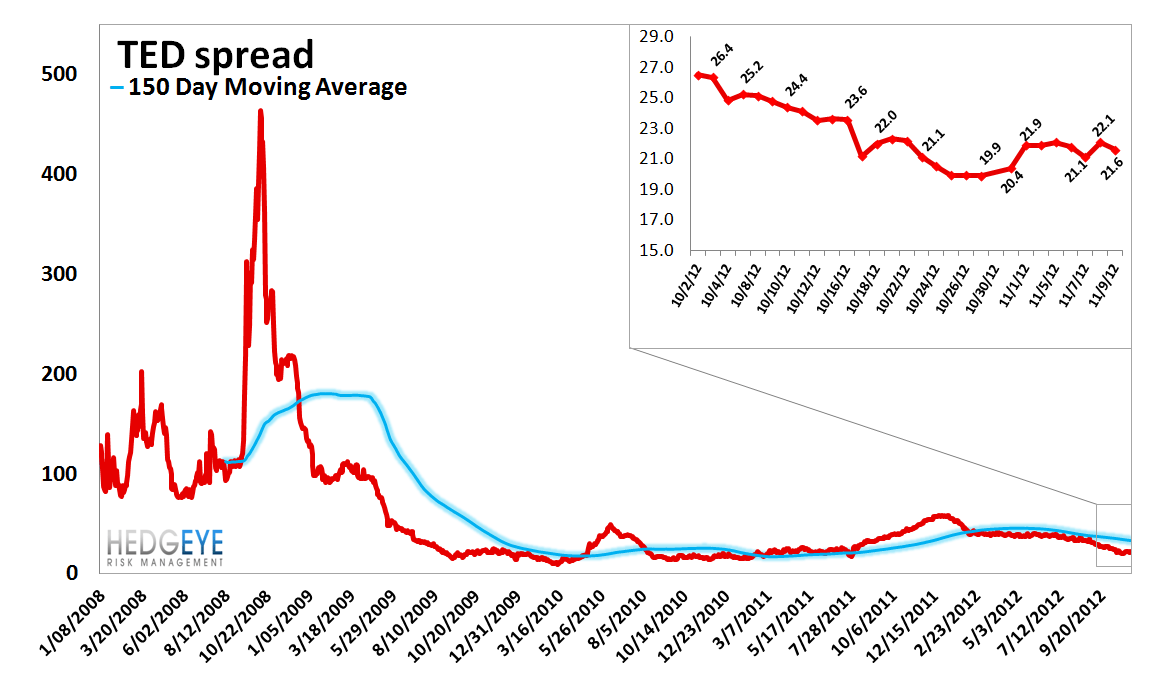

7. TED Spread Monitor – The TED spread fell less than 1 bp last week, ending at 21.6 bps versus 21.9 bps last week.

8. Journal of Commerce Commodity Price Index – The JOC index rose 1.3 points, ending the week at -3.59 versus -4.9 the prior week.

9. Euribor-OIS spread – The Euribor-OIS spread widened by 1 bp to 12 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

10. ECB Liquidity Recourse to the Deposit Facility – No change in the trajectory here - overnight deposits continue to shrink. The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis.

11. Markit MCDX Index Monitor – Last week spreads widened 3 bps, ending at 135 bps versus 132 bps the prior week. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1.

12. Chinese Steel – Steel prices in China fell 0.3% last week, or 12 yuan/ton, to 3738 yuan/ton. Since their lows on Sep 7, Chinese construction steel prices have rebounded ~10.3%. But the downward trend, which started August of last year, remains intact and is a sign of ongoing weakness in the Chinese construction market.. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened 9 bps to 135 bps. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – More upside than downside in the XLF in the short-term. Our Macro team’s quantitative setup in the XLF shows 2.3% upside to TRADE resistance and 0.1% downside to TREND support.

Margin Debt - September: +1.12 standard deviations

NYSE Margin debt rose to $315 billion in September from $287 billion in August. We like to to look at margin debt levels as a broad contrarian sentiment indicator. For reference, our approach is to look at margin debt levels in standard deviation terms over the period 1. Our analysis finds that when margin debt gets to +1.5 standard deviations or greater, as it did in April of 2011, it has historically been a signal of significant risk in the equity market. The preceding two instances were followed by the equity market losing roughly half its value over the following 24-36 months. Overall this setup represents a long-term headwind for the market. One limitation of this series is that it is reported on a lag. The chart shows data through September.

Joshua Steiner, CFA

Robert Belsky