This note was originally published at 8am on October 26, 2012 for Hedgeye subscribers.

“An economic model conditioned on the notion that nothing major will change is a useless one.”

-Nate Silver

I’ll reiterate Hedgeye Risk Management’s top Global Macro Theme for Q4 of 2012 this morning: #EarningsSlowing. We are finally seeing Major Changes to buy-side expectations for revenue and earnings. The sell-side’s estimates remain in lah-lah land.

As Nate Silver writes on page 193 of The Signal And The Noise, “anticipating these turning points is not easy.” But I fundamentally believe that if you study history, do math, and believe in the probability of mean reversion occurring, it’s certainly less hard.

“So we should have some sympathy for economic forecasters. It’s hard enough to know where the economy is going. But it’s much, much harder if you don’t know where it is to begin with.” (Silver, page 194). Since March, Global #GrowthSlowing has caught most consensus economists off-sides in 2012. Now #EarningsSlowing (which happens on a lag versus revenues) has analysts off-sides too.

Back to the Global Macro Grind…

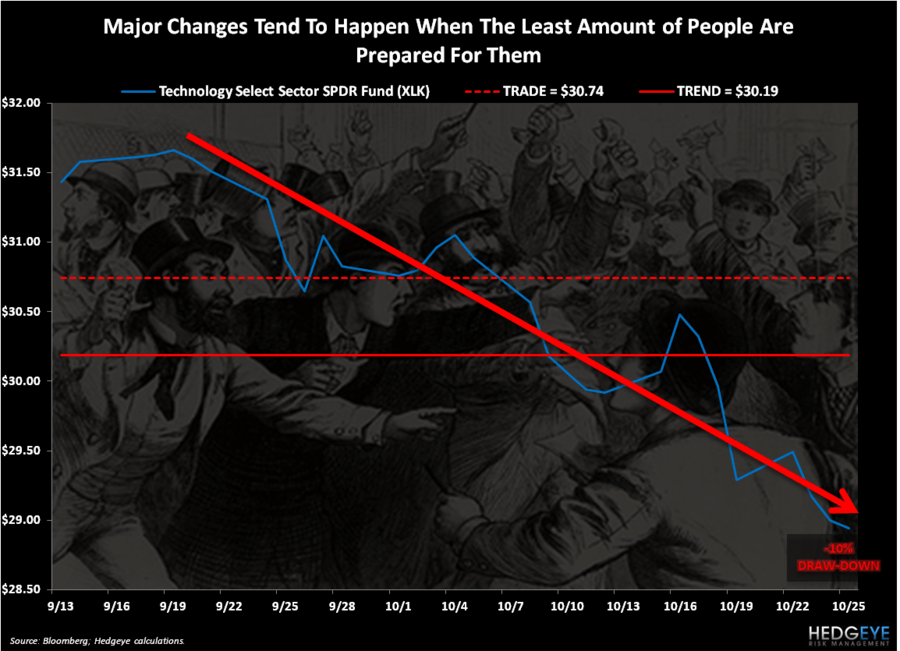

Flying back from California yesterday, I was watching Amazon (AMZN) and Apple (AAPL) earnings roll across my tweet-tape, and I couldn’t help but think, ‘gee, wouldn’t it have been nice if all the bulls warned us that both companies would miss and guide down?’

The risk that needed to be managed in AMZN and AAPL isn’t what you’ll see when the stocks open today - we’re already 5 weeks into what’s turning into a very serious draw-down in Tech (XLK) overall.

From the Bernanke Top (September 2012):

- Technology (XLK) = down -10%

- Apple (AAPL) = down -14%

- Amazon (AMZN) = down -15%

Remember, AAPL represents 20.6% of the Tech Sector (XLK) ETF. So Tech is outperforming AAPL at this point (and the SP500 is outperforming Tech). That means that anyone who was outperforming being long AAPL until September is probably now underperforming. Typically when this kind of rotation starts to happen in your portfolio, beta starts to eat your alpha.

Overall, beta (the SP500) is outperforming both Tech, AMZN, and AAPL. Since the Bernanke Top, the SP500 is in what we call a correction (down -4.2%). A draw-down is different than a correction. When you have double digit losses in a position, the next question isn’t “what is the stock down on the open?; it’s will this position start to crash?”

We define “crash” as a peak-to-trough price decline of 20% or more. Russia is teetering on moving back into crash mode this morning (RTSI down -1.8% on the session; down -18.3% from the March global #GrowthSlowing top). We’ll give the ole Bernank some credit for that one too – Russian stocks have everything to do with Petro-Dollars – and now we have Strong Dollar, Down Oil.

Away from the market’s leaders missing, that’s the other Big Beta thing going on out there this morning – remember, get the Dollar right, and you get a lot of other things right. Looking at Global Equity risk, the current 60-day Correlation Risk between the USD Index and the broad indices are as follows:

- SP500 = -0.87

- EuroStoxx600 = -0.95

- MSCI World Index = -0.91

So, you can look at risk from a bottom’s up stock perspective and/or from a top down (SECTOR, COUNTRY, or ASSET CLASS) beta risk factoring perspective, and you’ll learn a lot more about what’s really going on out there.

Keynesian economists have been saying that the Fed’s Policy To Inflate has not been causal to Correlation Risk. I say that’s a crock. If Romney wins the election (on that risk factor, probabilities in your conditional Bayesian model should be rising, not falling), there is a very good chance that the most asymmetric risk in all of Global Macro (Strong Dollar) busts a big move to the upside.

If that happens, the aforementioned correlations are probably going to keep moving towards 1.0, and we’ll probably be really right, in the immediate-term on Hedgeye’s 2nd Global Macro Theme for Q4 of 2012: Bubble#3 (Commodities).

I re-shorted the Gold Miners ETF (GDX) with that causal relationship in mind yesterday. I also re-shorted the Industrials Sector ETF (XLI) on green yesterday too.

Jay Van Sciver’s bearish thesis was very cogent in yesterday’s Early Look. If you believe there’s a bubble in Mining Capex, you’re probably in agreement with us that the revenue and #EarningsSlowing risk to pro-cyclical Industrials like Caterpillar (CAT) and Komatsu (KMTUY) remains to the downside as well.

Major Changes aren’t always underway in markets, but when you can get in front of the big ones you can save yourself, family, and clients from losing a lot of money.

Our immediate-term risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, AMZN, AAPL, XLK, and the SP500 are now $1694-1728, $105.98-110.66, $79.64-80.25, $1.28-1.30, $217-228, $591-613, $28.44-29.14, and 1395-1419, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer