After nearly a decade of speculation, the timing finally aligned for PVH to capitalize on WRC’s operating shortfalls through 1H. With a business over-indexed to Europe and WRC in search of a transformative deal, Manny Chirico (CEO) moved in earlier this summer sealing a deal just 8-months into Helen McCluskey’s tenure. The reality is that a combined PVH/WRC makes sense and initial accretion projections are likely conservative. This is a win/win for both as the 22% increase in aggregate market cap today suggests, but we see further upside with $10 in FY14 EPS on the horizon.

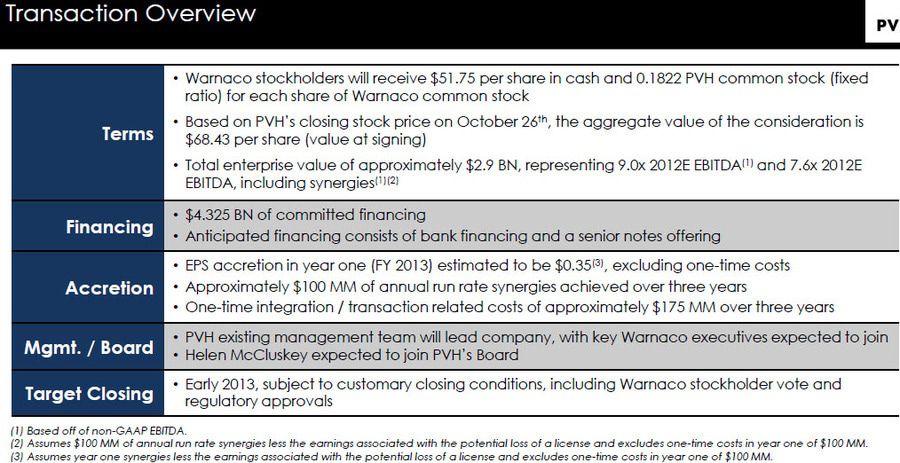

- Based on our estimates, Calvin Klein accounted for ~70% of WRC’s revenue base and ~80% of total EBIT. With the transaction valuing WRC at ~$2.9Bn and assuming a 5x EBITDA multiple for WRC’s Heritage businesses(Chaps, Speedo, and intimate brands Olga and Warner’s), the deal implies PVH paid a ~9.5x multiple for the CK business on FY12E estimates and under 8.5x FY13E pre synergies. This isn’t exactly a steal, but if you believe that WRC’s numbers are depressed, then it is attractive enough for a brand that has grown at a +13% CAGR at retail since it was acquired by PVH in 2003 and is expected to grow +8%-10% over the next 5-years.

- At risk of stating the obvious for a deal so widely expected, the strategic fit here makes sense given that WRC is PVH’s biggest licensee. Layer WRC’s core business over PVH’s infrastructure while complimenting each company’s regional strengths – PVH in NA and Europe, WRC in Latin America and Asia. Not to be overlooked is the ability for PVH to control the presentation of CK in its entirety at retail, which should help reignite a struggling ~$700mm CK Jeans franchise.

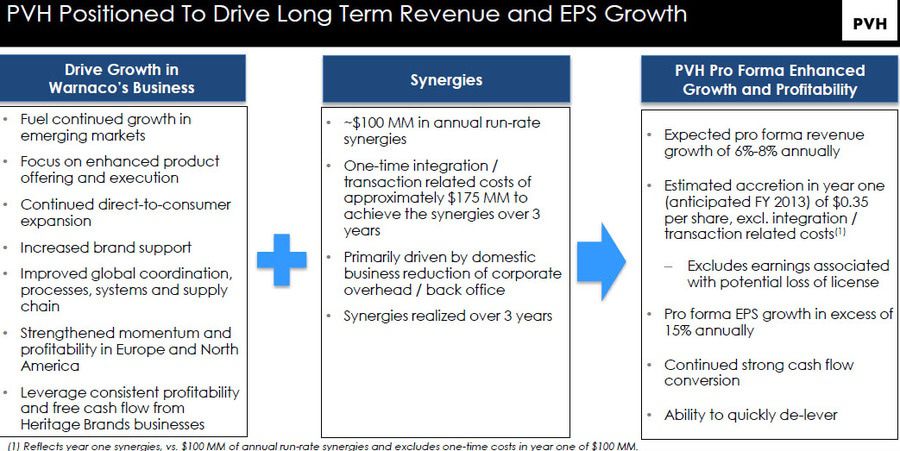

- With $100mm in costs targeted for elimination over the next 3-years as well as MSD-HSD revenue growth, PVH is looking to grow operating margins by nearly 50-75bps over each of the next 3-years.

- With $1.00 in EPS accretion by 2015 likely conservative, investors will start looking at FY14 EPS approaching $10.00. With margin expansion under the combined entity expected to drive a high-teens earnings growth rate over the next 3-years, we think multiple expansion is likely. However, even if we simply take the upper end of PVH’s historical EPS multiple over the last decade of 16x, we’re looking at a $160 stock over the next 12-24 months suggesting a 20%+ annual return even after today’s 18% move.

- Targeting early 2013 for closing the transaction.

Additional Highlights from the Call:

- WRC operating teams expected to stay on to operate various brands with headcount reductions expected to be primarily in back office

- PVH expects to pay debt down by $400mm/yr over the next 4yrs – focused on delivering as they did post Tommy deal

- Looking to finance the deal with a $4.324Bn financing commitment in the form of both bank financing and unsecured notes

- PVH will have more favorable leverage ratio post WRC deal (3.4x) than 2yrs ago when it bought Tommy (3.6x) – goal to get back down below 2.5x

- With this deal PVH hurdles RL in retail second only to VFC in revenues

- Deal shifts ~$100mm in WRC royalty revs to owned leaving a ~$170mm royalty base going forward

- Plan to leverage Tommy’s European expertise to drive stronger CK apparel presence in Europe beyond today’s $1Bn in revs

- Tommy growth opportunities via WRC’s Asia/Latin America presence upside to today’s plan – but don’t want to risk significant growth opportunity for CK by integrating Tommy too early (3-5yrs out)

- Operate a $200mm Tommy business in Latin America today and $600mm Tommy business in through licensing

partners that present an opportunity to integrate in the future - PVH assuming Chaps license (RL) does note continue re its accretion assumptions – currently in discussions with RL about this now

- ‘no intention of selling it at this point’ – re strength of Speedo business.

- Though ~$400mm+ PVH could get for Heritage business could help toward delivering if need be

- WRC’s store growth plans under review. Underwear stores work, but would like to put underwear and jeans under same roof