McDonald’s reports its 3Q results on Thursday before the market open. The sales results, and outlook, will likely drive the stock price reaction. Global growth slowing is a significant headwind for McDonald’s. We believe that September same-restaurant sales in the US grew in line, or slightly ahead of, what consensus is expecting.

Plenty Becoming Concerned About “Plenty To Be Concerned About”

The sell-side has gradually become less bullish on MCD since April 23rd, when we highlighted our concerns about the macro environment and lack of a new product pipeline in the US that could maintain sales momentum through the summer. We wrote that there was “plenty to be concerned about” for MCD going forward and saw JACK as a better long idea at the time. Six months later, we believe that we are nearing a point where MCD becomes attractive on the long side, but would reiterate our call to remaining on the sidelines through this print and for the time being.

We expect further negative revisions to McDonald's earnings estimates as several headwinds come into view. Difficult compares in the US for 4Q and 1Q, driven by strong underlying performance and favorable weather, and continuing macro headwinds in Europe, are the primary pillars of the bear case. We believe that there could come a point where, from a US sales perspective, consensus becomes too bearish. In general, McDonald’s finds a way to translate economic growth in the US into consistent sales and profit growth in its business by virtue of its omnipresence throughout the country and management’s continuing investment in the product pipeline and asset base. As the chart below indicates, industrial production has led the general trend of MCD US comparable sales growth over the last few years. This is not useful from a quarter-to-quarter perspective, but we use this metric when considering consensus expectations 6-12 months in the future. In conjunction with other analysis, we using this chart to ascertain if and when consensus becomes too bearish on McDonald’s trends.

Sales Preview

Below we go through what we would view as good, bad, or neutral comparable restaurant sales numbers for McDonald’s three regions in September. For comparison purposes, we have adjusted for historical calendar and trading day impacts (but not weather).

Compared to September 2011, September 2012 has one less Thursday, one less Friday, one additional Saturday, and on additional Sunday. We expect this to have a positive impact on September’s headline numbers. On average, we expect the impact to be in the region of 1.5%.

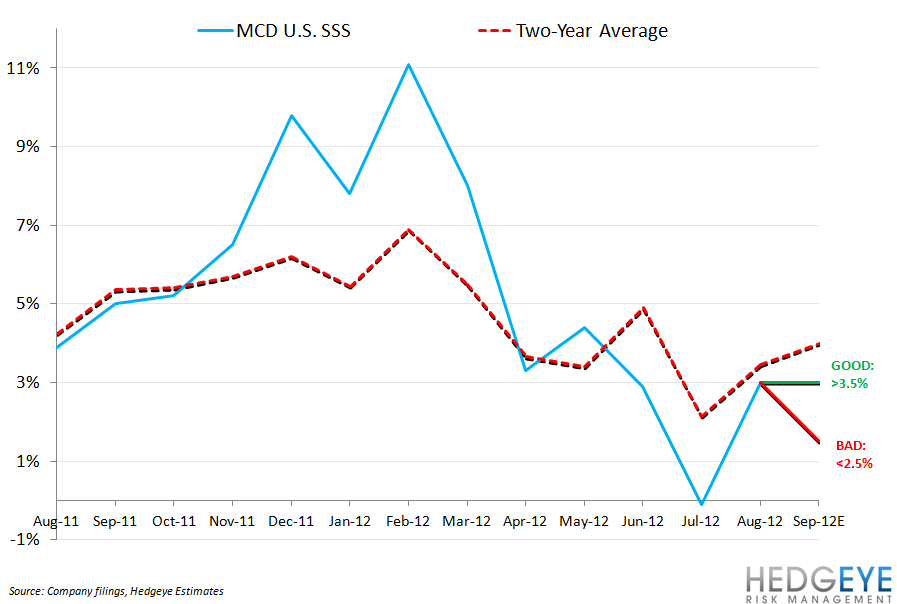

United States – facing a compare of 5% including a calendar shift of +0.4% to +1.2%, varying by area of the world:

GOOD: A print above 3.0% would be received as a strong result by investors as it would imply calendar-adjusted two-year average trends in line with August. Additionally, following negative traffic in August with a sequential improvement to flat-to-positive guest counts would be encouraging. We are anticipating a print of 2.5-3.0% for McDonald’s US business in September.

NEUTRAL: Same-restaurant sales growth of 1.5-2.5% would be received as neutral by investors as it would imply roughly flat calendar-adjusted same-restaurant sales and traffic growth versus August. Consensus estimates misrepresent the true expectations of the sell-side, in our view, due to consistent outliers to the downside month after month. We think investors are anticipating a print of 2.5% versus 2.1% Consensus Metrix.

BAD: A headline comp of less than 1.5% same-restaurant sales growth would be negative for MCD, especially given that the company is taking roughly 3% price in the US.

Europe – facing a compare of 6.9% including a calendar shift of +0.4% to +1.2%, varying by area of the world:

GOOD: A print of more than 1% would be received as a strong result by investors as it would imply acceleration in calendar-adjusted same-restaurant sales growth from August to September. We expect continuing strength in Russia, the UK and France but, even in the event of an upside surprise versus consensus, we expect investors to proceed with caution where Europe is concerned. We expect a print of between 0-0.5% for McDonald’s Europe business in September.

NEUTRAL: A print of 0-1% would be a neutral result for Europe as it would imply trends roughly in line with expectations and would provide some reassurance of MCD’s ability to take share on an ongoing basis.

BAD: Negative growth in Europe for the month of September would imply the second such disappointment of 3Q. McDonald’s has not printed two negative months in the same quarter in Europe for 29 quarters.

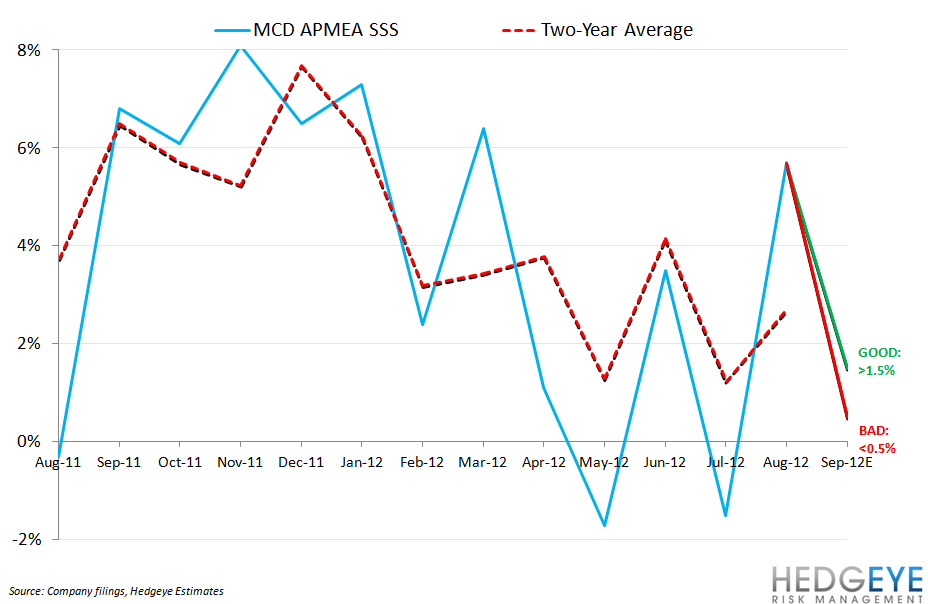

APMEA – facing a compare of 6.8% including a calendar shift of +0.4% to +1.2%, varying by area of the world:

GOOD: Same-restaurants sales growth of 1.5% or more would be received as a good result as it would imply an acceleration in calendar-adjusted two-year average trends versus August. With the backdrop of negativity on China’s economic outlook, an acceleration in trends into the end of 3Q could be encouraging. We are anticipating a print of 1.0% for McDonald’s APMEA business in September.

NEUTRAL: A print between 0.5% and 1.5% would be considered neutral for investors as it would be roughly in line with consensus, per Consensus Metrix.

BAD: Below 0.5% would imply continuing weakness in calendar-adjusted two-year average trends.

Howard Penney

Managing Director

Rory Green

Analyst