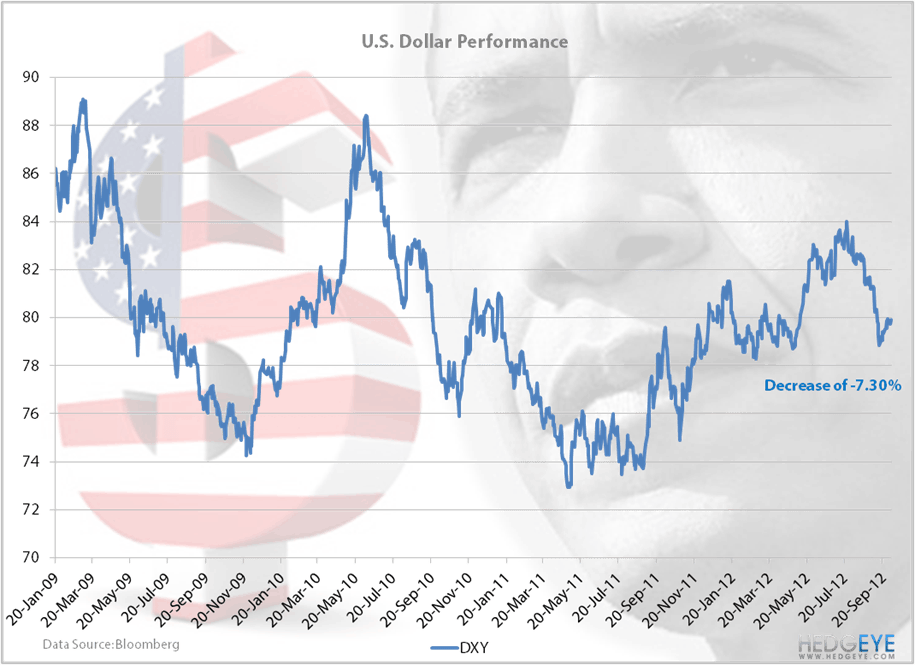

It should come as no surprise that while the S&P 500, Crude Oil and Gold all have stellar performance records under Obama's first term as President of the United States of America, the US dollar doesn't quite make the cut. The US Dollar Index has dropped -7.3% since January of 2009, due in part to the Fed's insistance on devaluing the currency in support of quantitative easing. We think that Romney should focus more on removing Bernanke as Chairman of the Fed and strengthening the dollar, but to do that, he has to win the election in November. Tonight's the night for him to prove he can do it.

In honor of tonight's presidential debate, we've examined the performance of several different asset classes and their performance from January 20, 2009 to today to see just how well President Obama has done during his first term.