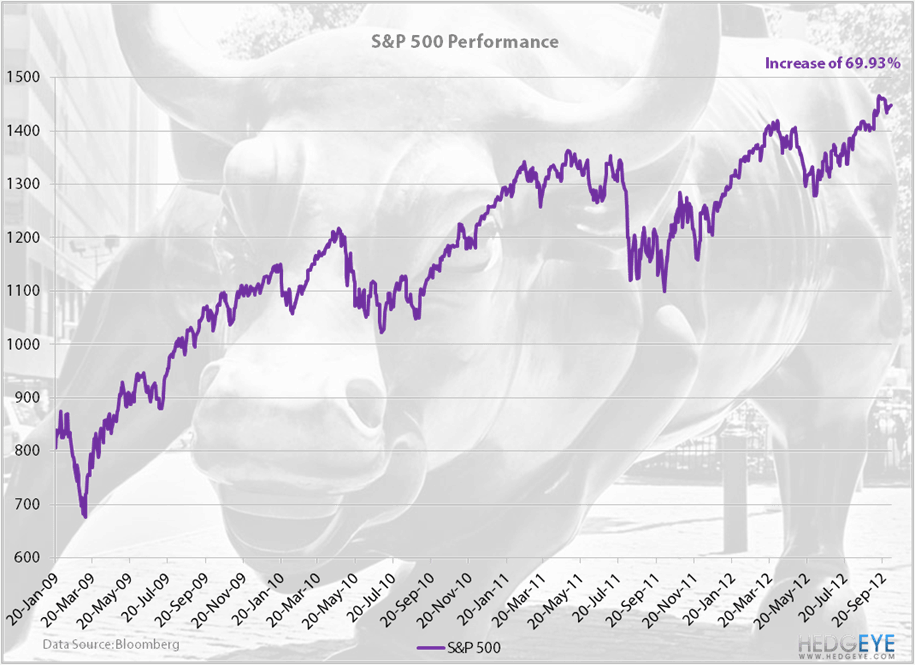

The S&P 500 has had a good run under President Obama's current term, increasing +69.9% since he took office in January of 2009. By comparison, George W. Bush saw the index falll -28.2% during his second term in office. Looks like Bernanke and Federal Reserve's nonstop quantitative easing have treated the President well.

In honor of tonight's presidential debate, we've examined the performance of several different asset classes and their performance from January 20, 2009 to today to see just how well President Obama has done during his first term.