This note was originally published at 8am on September 17, 2012 for Hedgeye subscribers.

“I wouldn’t give much for a man who warms himself with the comfort of vain hopes.”

-Sophocles

Hope is a lot of things, but it’s not a risk management process. The higher commodity and stock market inflations go, the less likely it is that the global economy recovers.

With a 0% asset allocation to commodities and a time stamped short position in the SP500 (SPY), I obviously lost last week’s battle with Ben Bernanke. That doesn’t make this war with Keynesian Academics over. It means it has just begun.

If Bernanke thinks that compressing the next 3 years of Equity returns into the last 3 months before a US Election is “price stability”, that probably means things are just about to get volatile, again.

Back to the Global Macro Grind…

I get things wrong. But when I do, I don’t put the country’s long standing liberties and structural employment at risk. Bernanke does. If I have one sincere hope for this country, it’s that this un-elected man thinks about that before he goes to bed at night.

To obfuscate the truth about currency debasement and real-time inflation expectations is one thing. To not be held accountable to these economic realities by the President of the United States is entirely another. Both Bush and Obama own this legacy of Bernanke’s economic storytelling.

Immediate and intermediate-term facts about Inflation Expectations:

- 10-yr breakevens (Inflation Expectations) moved right back to record highs last week (not YTD highs, record highs)

- CRB Commodities Index Inflation just crashed to the upside, +2.9% wk-over-wk, and +20% since June

- Oil price inflation (Brent) was up over +2.7% last week, +33% since June; US gas prices are now pushing back to $4

Sure, US and Russian stocks were up +1.9% and +7.4%, respectively, last week on that – but that’s nothing compared to the +153% YTD move in Venezuelan stocks post a Chavez currency devaluation! What did that do for the economic health of the Venezuelan people again?

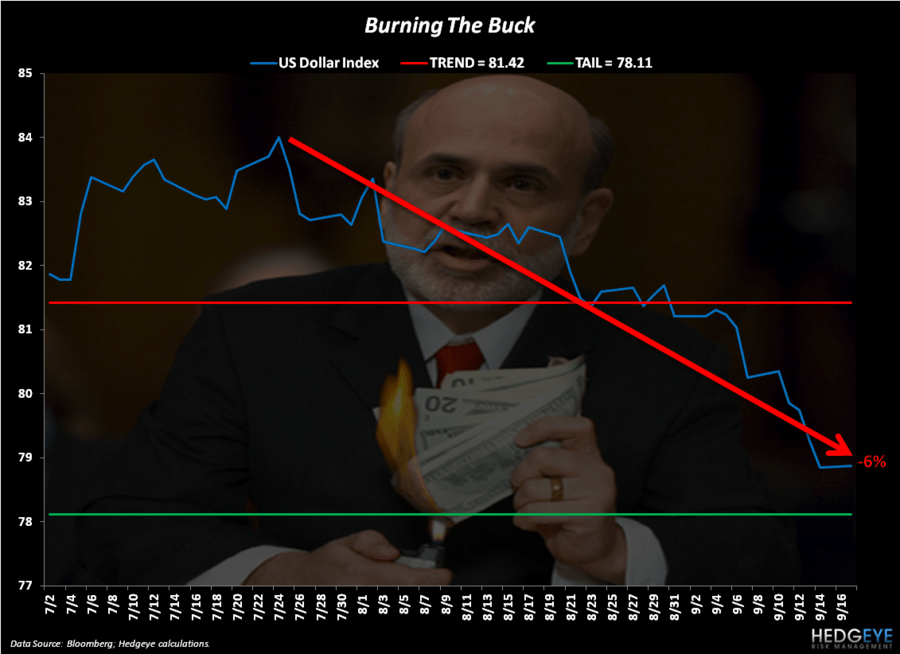

With Bernanke Burning The Buck (see Chart of The Day), the US Dollar Index was down for the 5th consecutive week. In the face of its -1.7% wk-over-wk inverse “to infinity and beyond” money printing move, here’s what other things priced in Dollars did:

- Coffee +11.1%

- Natural Gas +10.4%

- Rubber +6.7%

I know, I know. Instead of picking Copper, Gold, and Oil that inflated +2-6% last week, I’m cherry-picking some stuff you might need as you take tax-payer funded car service to your office in Washington D.C. every day.

Heck, maybe there’s going to be what Keynesian students of economic theories-failed call “substitution” and “multiplier” effects… and you’re going to start drinking Red Bull instead of coffee in the morning – right pumped to chase the market even higher!

Another way to look at Inflation Expectations Rising is, of course, the futures and options markets (CFTC data):

- Last week’s CFTC options contracts were up another +0.3% at all-time highs (1.33 million contracts outstanding)

- Gold contracts = up another +14% wk-over-wk (after being up +35% and +10% in the 2 wks prior) to their February highs

- Oil contracts shot north of 203,000, their highest level since Oil topped in February-March 7% higher than Friday’s close

People who trade market expectations, run long-term money, and/or do math obviously get this. That’s why the biggest macro call I missed in the last 6 months was probably issued during a super special deflationary dinner in Jackson Hole in August.

Do you think Bernanke and his boys told anyone he was going to do this? That’s just a question, not an answer – and one, looking back, that you should have asked yourself during the Hank Paulson TARP. Does it help people trust our markets more or less?

Sadly, this is how the Old Wall still works - but where it counts for The People (cost of living, jobs, etc.), it’s not working. If this man thinks his Vain Hope of a +2.5-3% US GDP recovery in 2013 is kidding this accurate GDP Growth forecasting firm, he’s going to be in for a long battle with some fact-based Tweet-heat. If anything, the probability of a US Recession in 2013 just went up.

*2007-2012 Federal Reserve Money Printing Fact: Policies To Inflate via currency devaluation slow real-inflation adjusted economic global growth. China’s stock market fell -2.1% last night (down -15.5% since May) after Singapore reported a nasty -10.6% export growth report for August as commodity price margin pressures continued to rise, dampening demand.

My immediate-term support and resistance risk ranges for Gold, Oil (Brent), US Dollar Index, EUR/USD, UST 10yr Yield, and the SP500 are now $1731-1784, $114.83-116.94, $78.57-80.31, $1.28-1.31, 1.70-1.87%, and 1433-1473, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer