-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Short EUR/USD (FXE); Long German Bonds (BUNL)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed down -2.6% week-over-week vs -0.1% last week. Bottom performers: Cyprus -9.7%; Spain -6.3%; Italy -5.6%; France -5.0%; Greece -4.7%; Portugal -4.2%; Ukraine -4.1%; Belgium -4.0%; Netherlands -3.3%; Germany -3.2%. Top performers: Poland +0.1%; Hungary -0.3%; Czech Republic -1%. [Other: UK -1.9%].

- FX: The EUR/USD is down -0.94% week-over-week. W/W Divergences: NOK/EUR +1.23%; SEK/EUR +1.02%; PLN/EUR +0.46%; GBP/EUR +0.44%; RUB/EUR +0.42%; CHF/EUR +0.20%; DKK/EUR 0.00%; HUF/EUR -1.01%; CZK/EUR -1.12%.

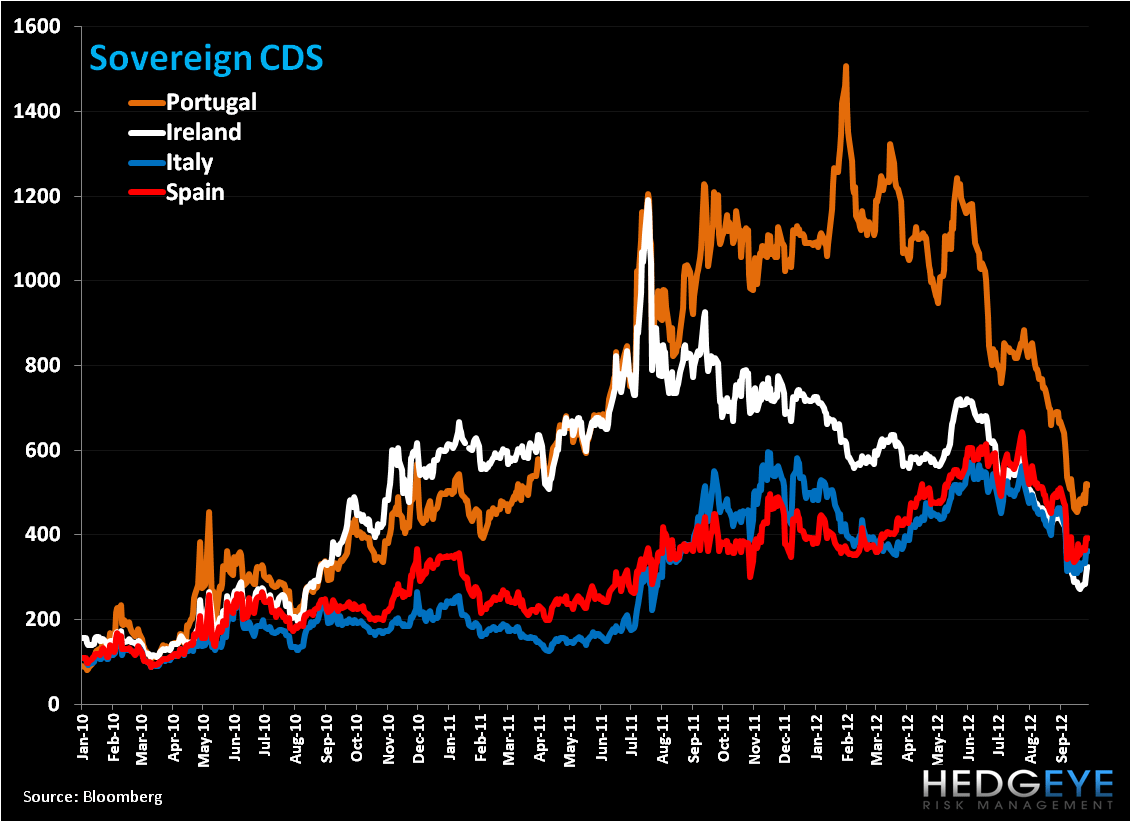

- Sovereign CDS: Sovereign CDS were higher on the week. On a week-over-week basis Ireland led the charge at +46bps to 323bps, followed by Portugal +43bps to 517bps, Italy +34bps to 362bps, and Spain +25bps to 392bps.

- Fixed Income: The 10YR yield for sovereigns were higher on week for the peripherals with the exception of Greece. Portugal climbed the most week-over-week at +40bps to 9.00% followed by Spain +39bps to 6.05% and Italy +15bps to 5.17%. Greece declined a monster -84bps on the week, Germany fell -18bps to 1.42% and France declined -10bps to 2.18%.

Spain – Who Cares?

While Greece in economic terms is a small fry compared to Spain, markets are once again showing the influence that political/economic events in just one country (in this case Spain) can have on global markets. Yet understanding the political developments in Spain this week takes a rather fine-toothed comb and a bit of head scratching on the economic side.

Is Spain asking for a sovereign bailout or not? Is the ESM the funding vehicle by which Spanish banks can tap funds to recapitalize its banks or not?

Both questions are unclear. To the first one, PM Rajoy continues to drag his feet and provide ambiguous responses.

A few considerations:

- Rajoy is simply politicking to play the best cards he can get from the ECB via the OMTs.

- Rajoy see that yields are not astronomical (the 10YR is currently at 6.05% vs a high of 7.58% on 7/24) so there’s no need for a bailout until this changes.

- Rajoy announced his 2013 budget yesterday (more below) and wants to first test the waters of the newest fiscal consolidation measures on his populous.

- Rajoy is waiting for the results of the Catalan elections (brought forward to November 25th) before asking for a bailout. [While the chances of an independent Catalonia appear small, the outcome could have an impact on the political mood which Rajoy will have to address].

To the second question on the ESM, finance ministers of Germany, Netherlands, Finland, and Austria stirred up the proverbial pot (and brought further uncertainty) this week when they said they were against allowing the ESM to take over Spain’s current bank recapitalization scheme. Despite the confusion over the language of this statement, the group is for the ESM “financing” the recapitalization, yet against the ESM (and possibly EFSF) subordinating bond holders in the event of a restructuring.

On Spain’s 2013 Budget

On Thursday Spain released its 2013 Budget. It’s hard to say why the U.S. market bounced on the news (the S&P500 closed up +0.95% on the day) but the IBEX closed down -0.2% on the day. Below are some of the notable tenants of the budget, however what’s critical is the government’s assumption for growth next year was unchanged at -0.5%.

Consensus has 2013 growth down at -1.3 to -1.6% and we think it could be closer to -2%! In short, slower growth will reduce tax revenues and prevent Spain from hitting its deficit target (from 6.3% this year to 4.5% next). You only have to look to 2011 to see how off the target the government has been: it once estimated the 2011 deficit to be 8% vs the most recently stated 8.9%.

- €13 billion ($16.7 billion) of spending cuts and tax increases for 2013 and said it will place new limits on early retirements.

- 58% of the budget adjustment will come from spending cuts, 42% from income measures.

- Increases taxes on lotteries, short-term capital gains, extended a wealth tax, and scraps rebates for large companies and mortgage holders.

- Goal, as presented in July, is designed to cut the deficit by €65 billion through the year 2014.

- Rajoy is chopping €40 billion from his ministries.

- Rajoy took €3B from the €67B pension reserve fund to boost payment for retirees. 1% increase in 2013.

- Budget plan will reduce the deficit to 4.5% of GDP in 2013 from the targeted 6.3% in 2012.

On forecasts:

- 'Soft' recession in 2013 with GDP (0.5%) = unchanged vs previous estimates.

- Hopes 2013 will be last year of recession.

- See's jobless rate at the end of 2013 at 24.3% vs 24.6% at the end of 2012.

- An increase of more than 30% in debt-servicing costs next year.

The Pain Continues

- Spain has over €40B in debt maturities (principal + interest) coming due in the next two months alone.

- Bank of Spain noted that bad loans held by Spanish banks hit a fresh record high in July. Non-performing loans rose to €169.3B in July, or 9.9% of outstanding credit, from €168.4B in July, or +9.4%.

- July bank deposits in Spain were €1.287T, down 7.8% Y/Y.

- Egon-Jones cut Spain’s sovereign credit rating to CC from CC+.

- Today’s audit release from Oliver Wyman’s stress tests of 14 Spanish banks showed a capital deficit of €59.3B, just shy of the €60B expected:

- Bankia was a notable underperformer with a €24.7B capital deficit shortfall.

- Banco Popular Espanol had a €3.2B shortfall.

- Notable lenders without capital needs included: Banco Santander SA, Banco Bilbao, and Banco Sabadell SA.

(Note: Oliver Wyman assumed a real decline in GDP of -4.1% in 2012, -2.1% in 2013 and -0.3% in 2014. It estimated that unemployment would keep rising to 27.2% in two years’ time and the tests factored in the Spanish 10YR yield of 7.4% this year and 7.7% in 2013 and 2014.)

One saving grace in the Spanish drama may be Germany. After all, its banks have the highest exposure in Europe to Spain, at $139.9B, of which $45.B alone is exposure to banks. While the figure is under the cap sum of €190B Frau Merkel pledged via the ESM, we still believe that fear of the repercussions of a Spanish default on the broader region and economy outweighs letting Spain fail in the mind of Merkel.

Otherwise, it’s pretty clear to us that Spain is hostage to the market, which will surely be pricing its debt higher, and that the government is underfunded to take care of its bank recapitalization alone. As always, fears from the sovereign will play into the perceived health of its banks and vice versa. While we can’t pin-point an additional bailout for Spain, we think one is inevitable, and probably before year-end.

EUR/USD:

Our immediate term TRADE range for the cross is $1.27 to $1.29. Our long-term TAIL line of resistance is $1.31. While Draghi’s “unlimited” promise has boosted the currency pair, we see a heavy line of resistance at our TAIL resistance level that we do not expect to be overcome. We’re currently short the EUR/USD via the etf FXE.

In the second chart below we look at CFTC data for net contracts of Euro non-commercial positions. Interestingly, since a high in short positions in the Euro on 6/5/12 (-213.060 contracts), investors have been less bearish (and covering). Week over week, contracts are 18% less bearish, -95,080 to -77,671 as of 9/18.

Data Dump:

Eurozone Business Climate -1.34 SEPT vs -1.18 AUG

Eurozone Consumer Confidence -25.9 SPET Final (inline)

Eurozone Economic Confidence 85 SEPT vs 86.1 AUG

Eurozone Industrial Confidence -16.1 SEPT vs -15.4 AUG

Eurozone Services Confidence -12 SEPT vs -10.8 AUG

Eurozone M3 2.9% AUG Y/Y vs 3.6% JUL

Eurozone CPI Estimate 2.7% SEPT Y/Y vs 2.6% AUG

Germany CPI (Preliminary) 2.1% SEPT Y/Y vs 2.2% AUG

Germany Import Price Index 1.3% AUG M/M (exp. 0.8%) vs 0.7% JUL [3.2% AUG Y/Y (exp. 2.7%) vs 1.2% JUL]

Germany Retail Sales -0.8% AUG Y/Y vs -1.6% JUL

Germany IFO Business Climate 101.4 SEPT (exp. 102.5) vs 102.3 AUG [falls for a 5th consecutive month]

Germany IFO Current Assessment 110.3 SEPT (exp. 111) vs 111.1 AUG

Germany IFO Expectations 93.2 SEPT (exp. 95) vs 94.2 AUG

Germany GfK Consumer Confidence 5.9 OCT (exp. 5.9) vs 5.9 SEPT

Germany Unemployment Change 9K SEPT vs 11K AUG [increased for a sixth month]

Germany Unemployment Rate 6.8% SEPT vs 6.8% AUG

UK Q2 GDP FINAL -0.4% Q/Q (initial -0.5%) and -0.5% Y/Y (inline)

France Consumer Confidence 85 SEPT vs 86 AUG

France Q2 GDP Final 0.0% Q/Q (UNCH) and 0.3% Y/Y (UNCH)

France Own-Company Production Outlook -6 SEPT vs -7 AUG

France Production Outlook Indicator -52 SEPT (exp. -44) vs -44 AUG

France Business Confidence 90 SEPT (exp. 89) vs 90 AUG

France Producer Price 2.6% AUG Y/Y vs 1.3% JUL

France Consumer Spending -0.5% AUG Y/Y vs 1% JUL

Italy Retail Sales -3.2% JUL Y/Y vs -0.5% JUN

Italy CPI (Preliminary) 3.4% SEPT Y/Y vs 3.3% AUG

Italy PPI 3% AUG Y/Y vs 2.2% JUL

Italy Hourly Wages 1.6% AUG Y/Y vs 1.5% JUL

Italy Consumer Confidence 86.2 SEPT (exp. 86) vs 86.1 AUG

Italy Business Confidence 88.3 SEPT vs 87.3 AUG

Italy Economic Sentiment 75.5 SEPT vs 79 AUG

Spain CPI (Preliminary) 3.5% SEPT Y/Y vs 2.7% JUL

Spain Producer Prices 4.1% AUG Y/Y vs 2.6% JUL

Spain Total Housing Permits -37.1% JUL Y/Y vs -49.7% JUN

Spain Retail Sales -2.1% AUG Y/Y vs -7% JUL

Belgium CPI 2.76% SEPT Y/Y vs 2.86% AUG

Netherlands Q2 GDP Final -0.4% Y/Y (vs original -0.5%) and 0.2% Q/Q (inline)

Netherlands Producer Confidence -6.7 SEPT vs -4.6 AUG

Austria Industrial Production 2% JUL Y/Y vs 0.3% JUN

Austria Producer Price Index 1% AUG Y/Y vs 0.2% JUL

Switzerland UBS Consumption Indicator 1.03 AUG vs 1.48 JUL

Switzerland KOF Swiss Leading Indicator 1.67 SEPT vs 1.59 AUG

Portugal Consumer Confidence -51.4 SEPT vs -49.2 AUG

Portugal Economic Climate -4.2 SEPT vs -4 AUG

Portugal Industrial Production -2.2% AUG Y/Y vs -0.3% JUL

Portugal Retail Sales -6.1% AUG Y/Y vs -7.7% JUL

Ireland Property Prices -11.8% AUG Y/Y vs -13.6% JUL

Sweden Consumer Confidence 2 SEPT vs 5.4 AUG

Sweden Manufacturing Confidence -10 SEPT vs -9 AUG

Sweden Economic Tendency Survey 95.8 SEPT vs 96.9 AUG

Sweden PPI -1.9% AUG Y/Y vs -1.1% JUL

Sweden Household Lending 4.6% AUG Y/Y vs 4.5% JUL

Sweden Retail Sales 1.8% AUG Y/Y vs 2.3% JUL

Norway Retail Sales 2.7% AUG Y/Y vs 2.7% JUL

Norway Unemployment Rate 2.4% SEPT vs 2.6% AUG

Finland Business Confidence -8 SEPT vs -9 AUG

Finland Consumer Confidence 3.4 SEPT vs 0.5 AUG

Finland PPI 1.5% AUG Y/Y vs 0.2% JUL

Finland Unemployment Rate 7.3% AUG vs 6.9% JUL

Greece Retail Sales -8% JUL Y/Y vs -9.6% JUN

Poland Retail Sales 5.8% AUG Y/Y vs 6.9% JUL

Poland Unemployment Rate 12.4% AUG vs 12.3% JUL

Hungary Unemployment Rate 10.4% AUG vs 10.5% JUL

Czech Republic Business Confidence 2.7 SEPT vs 2.4 AUG

Czech Republic Consumer and Business Confidence -3.8 SEPT vs -3.6 AUG

Czech Republic Consumer Confidence -29.8 SEPT vs -27.3 AUG

Slovakia Consumer Confidence -31.6 SEPT vs -25.9 AUG

Slovakia Industrial Confidence -0.3 SEPT vs -4.7 AUG

Slovakia PPI 4.1% AUG Y/Y vs 3.6% JUL

Slovenia CPI 3.3% SEPT Y/Y vs 2.9% JUL

Turkey Foreign Tourist Arrivals 9.7% AUG Y/Y vs -0.6% JUL

Interest Rate Decisions:

(9/25) Hungary Base Rate Announcement CUT 25bps to 6.50%

The European Week Ahead:

Monday: Sep. Eurozone PMI Manufacturing - Final; Aug. Eurozone Unemployment Rate; Sep. Germany PMI Manufacturing – Final; Sep. UK PMI Manufacturing; Aug. UK Net Consumer Credit, Net Lending Sec. on Dwellings, Mortgage Approvals, M4 Money Supply; Sep. France PMI Manufacturing – Final; Sep. Italy PMI Manufacturing, New Car Registrations, Budget Balance; Aug. Italy Unemployment Rate Preliminary; Greece Manufacturing PMI

Tuesday: Aug. Eurozone PPI; Sep. UK House Prices; PMI Construction; BRC Shop Price Index

Wednesday: Sep. Eurozone PMI Composite and Services - Final; Aug. Eurozone Retail Sales; Sep. Germany PMI Services – Final; Sep. UK PMI Services, Official Reserves; Sep. France PMI Services – Final; Sep. Spain Services PMI; Sep. Italy PMI Services

Thursday: Oct. Eurozone ECB Announces Interest Rates; Oct. Germany BoE Asset Purchase Target, BoE Announces Rates; Sep. UK New Car Registrations; 2Q BoE Housing Equity Withdrawal

Friday: Aug. Germany Factory Orders; Aug. Spain Industrial Output

Matthew Hedrick

Senior Analyst