In preparation for CCL's 3Q earnings release tomorrow, we’ve put together the recent pertinent forward looking company commentary

- "In March, we entered into zero cost collars for an additional 19% of our estimated fuel consumption for the second half of fiscal 2012 and fiscal 2013, bringing the total to approximately 38% for this period. We feel comfortable with this level of protection for the next 18 months."

- "We also have zero cost collars in place that cover approximately 19% of our estimated fuel consumption for fiscal 2014 and 2015. We will look to opportunistically increase these percentages over time."

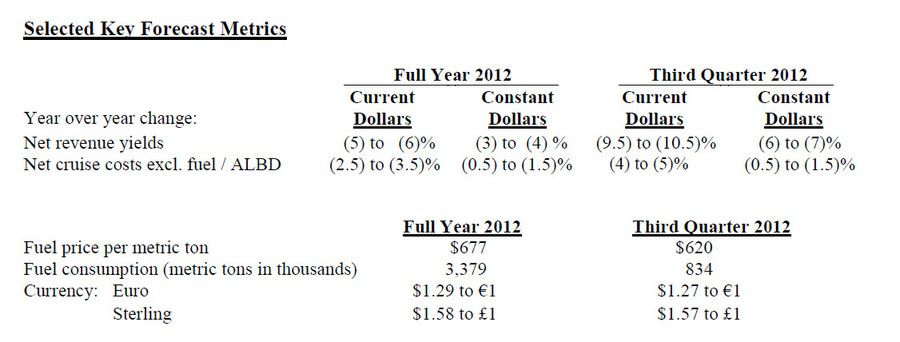

- "The price of Brent was $93 a barrel the other day when we locked off our forecast. The second rule of thumb relates to our current fuel derivatives portfolio where a 10% reduction in the price of Brent for the remaining half of 2012 would result in an additional $0.04 of realized losses on fuel derivatives that would offset the $0.13 per share favorable impact from the reduced price of fuel."

- "A 10% change in all relevant currencies relating to the U.S. dollar for the remaining half of 2012 would impact our P&L by $0.11 per share."

- "The significantly higher air costs for North American passengers traveling to Europe caused bookings for these itineraries to slow and resulted in our having to take further price reductions for these programs."

- "During this past spring North American brands experienced slightly lower pricing than we originally forecasted. North American brand European itineraries experienced the largest declines in pricing, not just because of the slowing North American market but also because of the challenges in locally sourcing business from the softer European markets for these sailings. As a consequence for the remainder of 2012 we have modestly reduced our revenue yield outlook for North American brands for the second half of the year...For the full year North American brand revenue yields are now forecasted to be flat on a year-over-year basis."

- "Revenue yields for our European brands, excluding Costa, are also forecasted to be slightly lower than previously anticipated primarily due to the significant softening in the Spanish markets. Ibero, our Spanish cruise line has suffered a significant decline in revenue yields. Fortunately there are just three ships operating in the brand so the impact of the struggling Spanish economy on our financial results has not been significant."

- "We do expect that when year-over-year occupancy levels begin to normalize, Costa's cruise prices for 2013 should start to firm up. Costa's revenue yields for 2012 are forecasted to be down in the mid-teens levels on a year-over-year basis and we expect Costa's operating loss to be in the range of $100 million."

- "2012 forecasted operating cash flow is expected to be in the range of $3.2 billion, net CapEx for the year is estimated at $1.9 billion, so after the dividend that will leave us with approximately $500 million of free cash flow. 2013, our CapEx is currently estimated at $1.8 billion, so with operating cash flow expected to improve in 2013, there should be further increases in free cash flow come 2013.

- "(Excluding Costa), we are estimating that Q3 and Q4 yields will be down in the same relative range of 3% to 4%."

- "We're incentivizing more going into Q3."

- [Booking ranges for Q3 and Q4] "We are towards the lower end of the ranges (85-95% for Q3, 55-75% for Q4)"

- [Share repurchase program] "At the moment... $330 million that remains on the program."

- "We are seeing some increases in onboard. We were very pleased. In fact, we took the guidance up almost a point on onboard from March to the June guidance, so the trend is very favorable and I hope it is a leading indicator."

- "Onboard was flat on the European brands despite the lower occupancy, so you're actually seeing some additional spending on a per diem basis. So, the onboard spend per person is going up. It was just we had a couple of points less occupancy on the brand. So, flat on a yield basis."

- "We're very pleased with Australia and it's likely that we may be through the worst part of it in terms of the additional capacity. Next year Carnival brings a ship down to Australia and it's performing very nicely right now, so we're very pleased with Australia. In Asia, it's a pretty positive situation. We moved the largest ship into the China market, the Costa Victoria, and it's doing quite well, and we expect that we would be breakeven this year in Asia or maybe make a little bit of positive cash flow and that looks like it's going to be the case so far. So, bookings – pricing in Asia and Southeast Asia and China is quite good right now."

- "Beginning next spring, we're bringing a second Costa ship to Asia, the Costa Atlantica"

- "It's still early because South America season is basically mid December to mid March so it's a very short season and it's still quite early. But, early indications are positive."

- "Direct bookings last year were 19% of our total business. That has moved up year-over-year. We don't have any specific aspirations. I do expect the number will continue to creep up over time."

3Q 2012 excluding Costa

- "Capacity is expected to increase 2.9%, 3.4% in North America markets and 1.6% in EAA at the current time."

- "On a fleet-wide basis, third quarter pricing and occupancy is lower than a year ago."

- "North American brand capacity in the third quarter is 38% in the Caribbean, slightly up from a year ago, 24% in Alaska, slightly higher than a year ago and 25% in Europe, which is about the same as last year. North American brand pricing is lower than a year ago at slightly lower occupancies. Pricing for Caribbean itineraries is in line with a year ago with pricing for both Alaska and European cruises lower versus last year. The occupancies for Caribbean, Alaska cruises are slightly lower versus last year and occupancies for Europe cruises are lower than a year ago."

- "EAA brand capacity in the third quarter is 85% in European itineraries, up from 82% prior year. EAA brand pricing, this excludes Costa again for European and all other itineraries, is slightly lower than a year ago on slightly lower occupancies. U.K. brands pricing is higher than a year ago and German pricing is slightly lower."

4Q 2012 excluding Costa

- "Fleet-wide capacity is expected to be 3% to 4% higher than last year. 3.9% of that is for North American brands, 2.1% for EAA."

- "Fleet-wide pricing, excluding Costa, is slightly lower than a year ago on lower occupancies."

- "North American brands are 43% in the Caribbean, slightly higher than a year ago; 13% in Europe, about the same as last year, the balance is in various other itineraries. North American brand pricing is slightly lower than last year at lower occupancies. Caribbean pricing is higher than a year ago at flat occupancies. Europe pricing is lower versus last year at lower occupancies and pricing for all other itineraries taken together is slightly higher than a year ago on lower occupancies."

- "EAA pricing in the fourth quarter, and this excludes Costa, is higher versus a year ago at lower occupancies. Pricing for Europe cruises, which represents 61% of EAA itineraries are slightly higher on lower occupancies. For all other itineraries taken together, pricing is also higher on lower occupancies. Costa's pricing and occupancies are lower than a year ago. Although pricing for Europe brands excluding Costa is higher at the present time because there are more cabins to fill versus last year, we expect pricing for EAA brands to decline as the quarter closes on a fleet-wide basis. Similar to the third quarter, we're forecasting EAA revenue yields excluding Costa to be lower in the fourth quarter."

1Q 2013 including Costa

- "Fleet-wide capacity for the first quarter of 2013 is expected to be higher by 4%, 3.4% in North America, 4.9% in EAA. Fleetwide occupancies at the present time are lower than a year ago with pricing at the present time slightly lower versus last year."

- "For North American brands taken together, occupancies are flat year-over-year with overall pricing currently lower. However, pricing is higher for most of the North American brands, but lower in total partly due to itinerary changes and the mix of the four brands pricing."

- "Revenue yield comparisons for the first quarter of 2013 versus first quarter of 2012 will be more challenging given our stronger first quarter North American yield performance in 1Q 2012."

- "On a fleet-wide basis, EAA brand occupancies are behind last year with higher pricing. Although still early, pricing on Costa's bookings for Q1 is also higher on a year-over-year basis at lower occupancies."