-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Long German Bonds (BUNL); Short EUR/USD (FXE)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed down -0.1% week-over-week vs +1.3% last week. Bottom performers: Italy -3.8%; Russia (RTSI) -3.8%; Finland -2.7%; Hungary -2.5%; Austria -2.3%; Czech Republic -1.5%; France -1.4%. Top performers: Greece +4.4%; Slovakia +3.1%; Denmark +2.1%; Cyprus +1.7%. [Other: UK -1.1% and Germany +0.5%].

- FX: The EUR/USD is up +1.09% week-over-week. W/W Divergences: GBP/EUR +1.24%; TRY/EUR +1.10%; SEK/EUR +0.94%; CHF/EUR +0.42%; NOK/EUR +0.05%; DKK/EUR -0.01%; HUF/EUR -0.25%; RUB/EUR -0.75%; PLN/EUR -1.76%; CZK/EUR -1.99%.

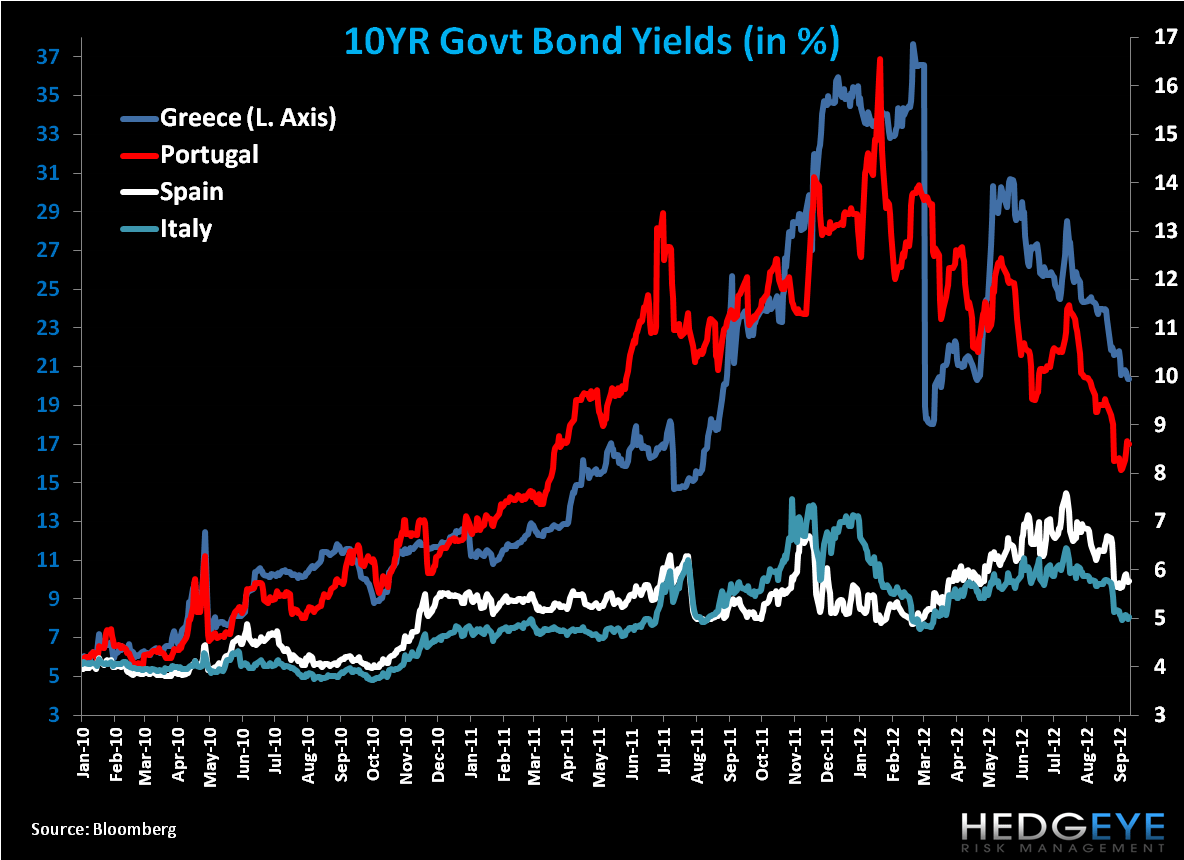

- Fixed Income: The 10YR yield for sovereigns were mixed week-over-week after peripherals fell decidedly in the last two straight weeks. Greece saw the largest decline, -45bps to 20.34%, followed by Germany’s -10bps move to 1.60%. Portugal gained the most, rising +51bps to 8.60% and Spain gained +12bps to 5.76%. Italy gained +5bps to 5.02% while most other countries were flat.

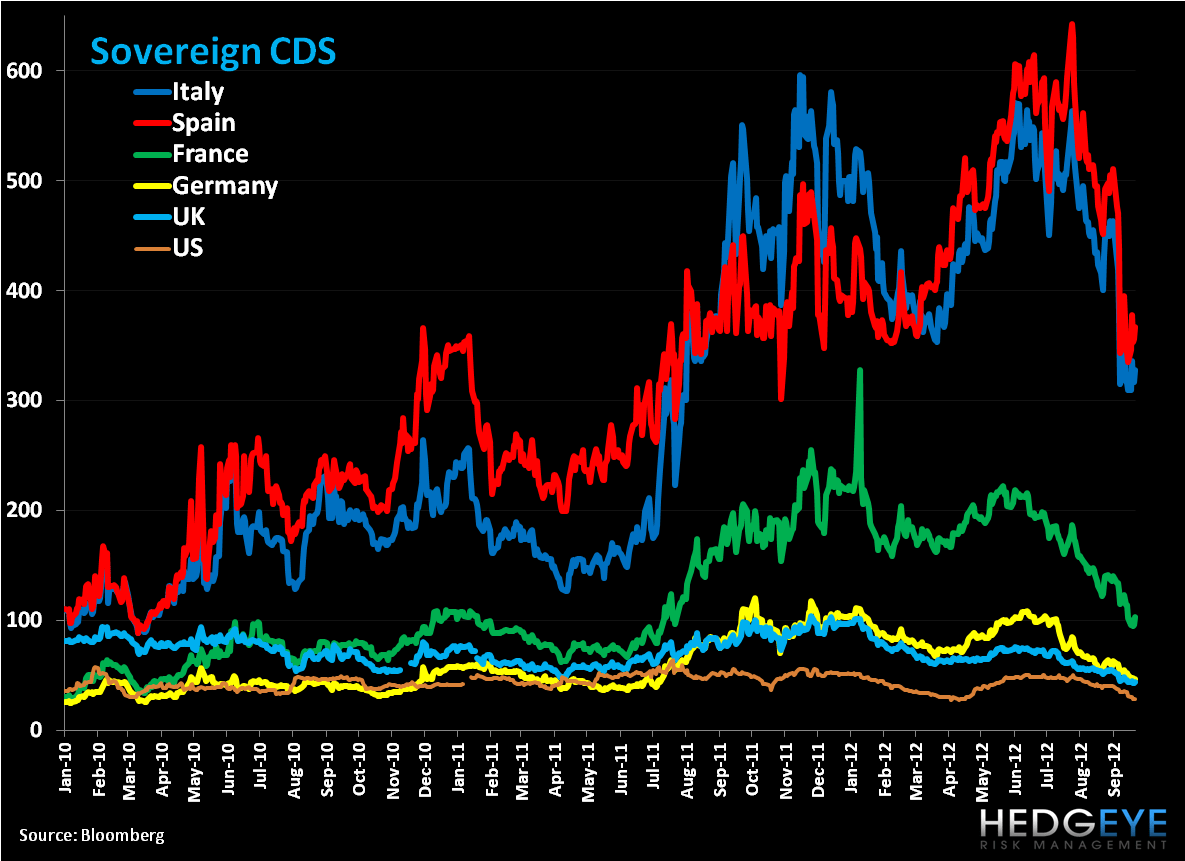

- Sovereign CDS: Sovereign CDS were mostly higher on the week. On a week-over-week basis Spain led the charge at +32bps to 367bps, followed by Italy +18bps to 328bps, and Portugal +10bps to 474bps. Ireland was a notable exception falling -12bps to 277bps and Germany fell -3bps to 47bps.

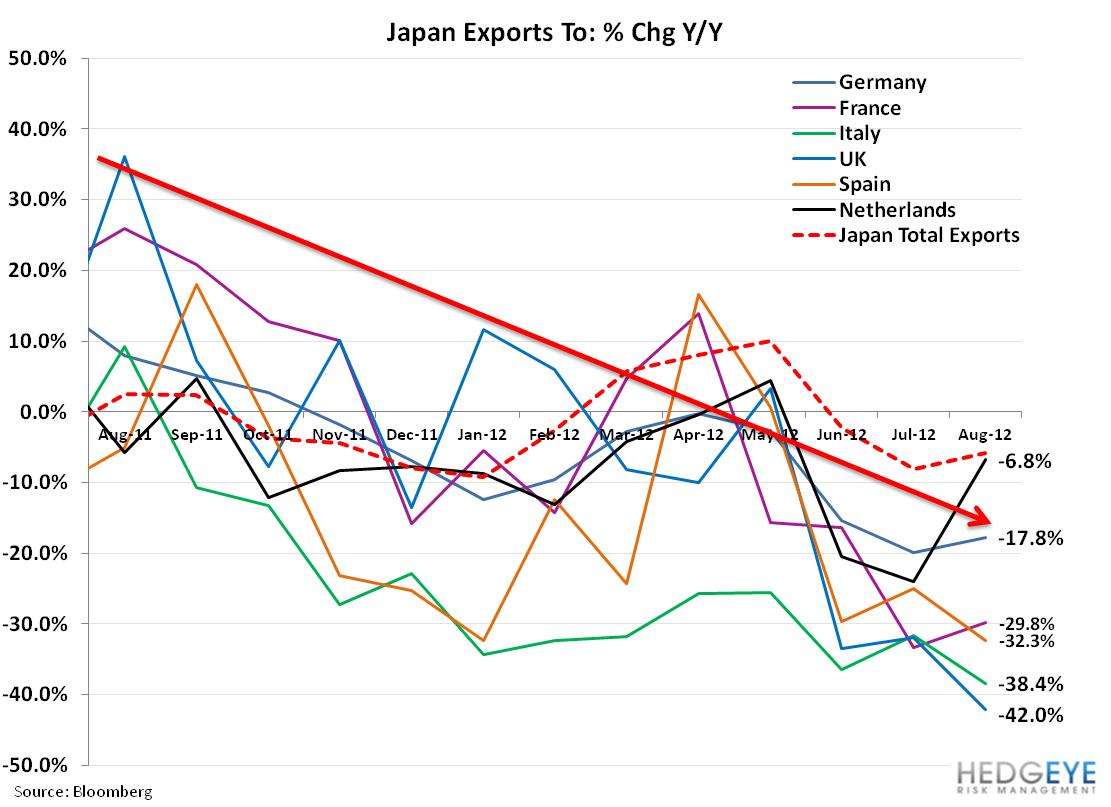

Charts of the Week

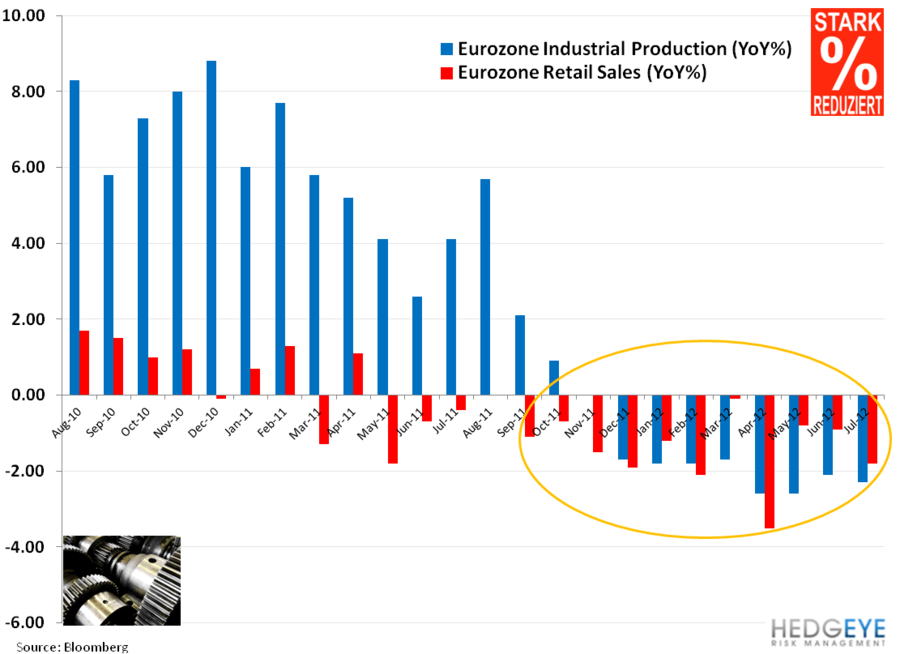

Due to the Central Banker Waves in recent weeks we’re focusing on the data this week vis-à-vis charts. We’ll continue to identify the risks we see across Europe and frame the political developments, however here we’ll let some of the more salient charts of the week do the talking. While Draghi has certainly made great waves with his newest “unlimited” sovereign bond purchasing program, we think there remains great risk in the market due to the constrained nature of the Eurozone; Eurocrat indecision on a concrete path forward; and grave hurdles in creating a fiscal and banking union across the Eurozone (and/or EU).

What should remain is an environment of growth slowing, especially across the periphery, and to levels well below current consensus. Some of the forces acting on growth include: austerity, lower government tax revenues, high unemployment rates, reduced trade demand from key trading partners, all of which should continue to reduce confidence and spending across the economies.

Today we received a money card that we had long been expecting: Italy cuts its GDP forecasts for 2012 to -2.4% vs -1.2% prior and in 2013 to -0.2% from +0.5% prior. It also revised its public deficit estimates for this year from 1.7% of GDP to 2.6% and next year from 0.5% of GDP to 1.8%. These are massive misses!

In short, there’s a significant disconnect between fundamentals and market performance. We’re currently on the side lines given the risk profile and not playing into Draghi’s “unlimited” hand.

EUR/USD:

Our immediate term TRADE range for the cross is $1.29 to $1.31. Our long-term TAIL line of resistance is also $1.31. While Draghi’s “unlimited” promise has boosted the currency pair, we see a heavy line of resistance at our TRADE and TAIL resistance level that we do not expect to be overcome. We’re currently short the EUR/USD via the etf FXE.

Data Dump:

Eurozone Labor Costs 1.6% in Q2 Y/Y vs 1.5% in Q1

Eurozone Economic Sentiment -3.8 SEPT vs -21.2 AUG

Eurozone Construction Output -4.7% JUL Y/Y vs -2.8% JUN

Eurozone Composite 45.9 SEPT Flash (exp. 46.6) vs 46.3 AUG

Eurozone PMI Manufacturing 46 SEPT Flash (exp. 45.5) vs 45.1 AUG

Eurozone PMI Services 46 SEPT Flash (exp. 47.5) vs 47.2 AUG

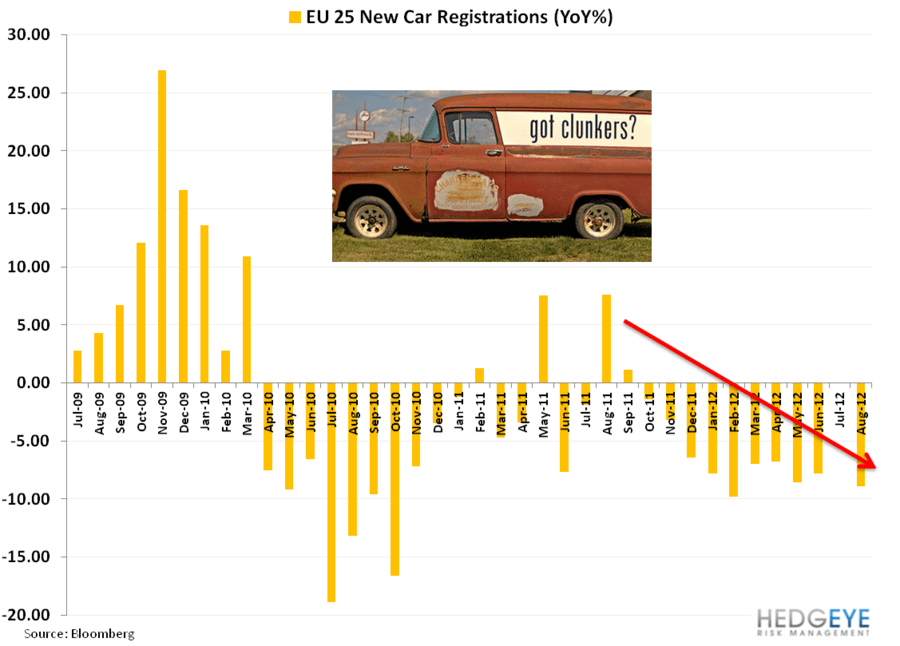

EU27 New Car Registrations -8.9% AUG Y/Y vs -7.8% JUL

- Volkswagen (VOW.GR) 204,034 +1.6%

- PSA (UG.FP) 81,562 (12.3%)

- GM (GM) 53,586 (17.7%)

- Renault (RNO.FP) 61,749 (13.0%)

- Fiat (F.IM) 37,687 (17.7%)

- Daimler (DAI.GR) 39,464 (0.3%)

- Toyota (TM) 32,214 (5.5%)

- BMW (BMW.GR) 42,894 (12.4%)

- Nissan (NSANY) 22,668 (4.8%)

- Honda (HMC) 8,567 +18.7%

- Ford (F) 43,401 (28.7%)

Germany Producer Prices 1.6% AUG Y/Y vs 0.9% JUL

Germany ZEW Current Situation 12.6 SEPT (exp. 18) vs 18.2 AUG

Germany ZEW Economic Sentiment -18.2 SEPT (exp. -20) vs -25.5 AUG

Germany PMI Manufacturing 47.3 SEPT Flash (exp. 45.2) vs 44.7 AUG

Germany PMI Services 50.6 SEPT Flash (exp. 48.5) vs 48.3 AUG

France PMI Manufacturing 42.6 SEPT Flash (exp. 46.4) vs 46 AUG

France PMI Services 46.1 SEPT Flash (exp. 49.5) vs 49.2 AUG

Italy Industrial Order -4.9% JUL Y/Y vs -10.8% JUN

Portugal Producer Prices 4.0% AUG Y/Y vs 3.0% JUL

UK CPI 2.5% AUG Y/Y (exp. 2.5%) vs 2.6% JUL [0.5% AUG M/M vs 0.1% JUL]

UK RPI 2.9% AUG Y/Y (exp. 3.1%) vs 3.2% JUL

UK Retail Sales w Auto Fuel 2.7% AUG Y/Y vs 2.3% JUL [-0.2% AUG M/M vs 0.3% JUL]

Spain Mortgages on Houses -17.5% JUL Y/Y vs -25.2% JUN

Spain Mortgages-capital Loaned -27.4% JUL Y/Y vs -20.4% JUN

Switzerland Credit Suisse ZEW Survey of Expectations of Growth -34.9 SEPT vs -33.3 AUG

Switzerland Exports 0.9% AUG M/M vs -0.7% JUL

Switzerland Imports 2.4% AUG M/M vs -0.7% JUL

Switzerland Money Supply M3 8.5% AUG Y/Y vs 9.5% JUL

Netherlands Consumer Confidence -29 SEPT vs -32 JUL

Netherland Unemployment Rate 6.5% AUG vs 6.5% JUL

Netherlands Consumer Spending -1.5% JUL Y/Y vs -0.5% JUN

Netherland House Price Index -8% AUG Y/Y vs -8% JUL

Ireland Q2 GDP 0.0% Q/Q vs -0.7% in Q1 [-1.1% Y/Y vs 2.1% in Q1]

Ireland PPI 6.0% AUG Y/Y vs 4.5% JUL

Slovakia Unemployment Rate 13.2% AUG vs 13.3% JUL

Slovenia Unemployment Rate 11.7% JUL vs 11.5% JUN

Poland Producer Prices 3.1% AUG Y/Y (exp. 3.0%) vs 3.7% JUL

Czech Republic PPI (Industrial) 1.9% AUG Y/Y vs 1.3% JUL

Croatia Unemployment Rate 17.5% AUG vs 17.5% JUL

Lithuania Industrial Production 10.9% AUG Y/Y vs 6.2% JUL

Latvia Producer Prices 2.2% AUG Y/Y vs 2.1% JUL

Russia Disposable Income 7.2% AUG Y/Y (exp. 2.7%) vs 2.2% JUL

Russia Real Wages 7.8% AUG Y/Y (exp. 9.6%) vs 8.1% JUL

Russia Retail Sales 4.3% AUG Y/Y (exp. 4.6%) vs 5.4% JUL

Russia Unemployment Rate 5.2% AUG (exp. 5.5%) vs 5.4% JUL

Russia Investment in Production Capacity 2.3% AUG Y/Y (exp. 3.5%) vs 3.8% JUL

Turkey Consumer Confidence 91.1 AUG vs 92.8 JUL

Turkey Unemployment Rate 8% JUN vs 8.2% MAY

Interest Rate Decisions:

(9/18) Turkey Benchmark Repo Rate UNCH at 5.75%

(9/19) BOE minutes show vote to keep rates and asset purchases on hold was unanimous 9-0

The European Week Ahead:

Monday: Sep. Germany IFO Business Climate, Current Assessment, Expectations; Aug. Germany Import Price Index (Sep. 24-30); Sep. UK Nationwide House Prices (Sep. 24-28)

Tuesday: Mario Draghi will discuss the state of economic and currency union in the Eurozone with German Chancellor Angela Merkel in Berlin; Oct. Germany GfK Consumer Confidence Survey; Aug. UK BBA Loans for House Purchase; Sep. France Own-Company Production Outlook, Production Outlook Indicator, Business Confidence Indicator; Aug. Spain Producer Prices, Budget Balance: Sep. Italy Consumer Confidence Indicator, Aug. Hourly Wages

Wednesday: Sep. Germany Consumer Price Index – Preliminary; Sep. UK CBI Reported Sales; Sep. France Consumer Confidence Indicator; Aug. France Jobseekers; Jul. Italy Retail Sales

Thursday: Sep. Eurozone Consumer Confidence – Final, Business Climate Indicator, Economic, Indust. and Services Confidence; Aug. Eurozone M3; Sep. Germany Unemployment Data Released by Federal Labor Agency, Unemployment Change, Unemployment Rate; Sep. UK Gfk Consumer Confidence Survey; 2Q UK GDP – Final, Total Business Investment – Final, Current Account; Aug. Spain Retail Sales; Jun. Spain Total Housing Permits; Sep. Italy Business Confidence

Friday: Sep. Eurozone CPI Estimate; Jul. UK Index of Services; Aug. France Producer Prices, Consumer Spending; 2Q France GDP – Final; Sep. Spain CPI - Preliminary; Jul. Spain Current Account; Sep. Italy CPI - Preliminary; Aug. Italy PPI; Jul. Greece Retail Sales

Matthew Hedrick

Senior Analyst