The baby apparel market is getting increasingly crowded with the latest entry of Gilt Groupe. The company best known as a flash-sale pioneer is introducing Little Gilt as its first private label line highlighting a void in upscale baby essentials such as onesies, footies, and whatever else you care to swaddle your little one in.

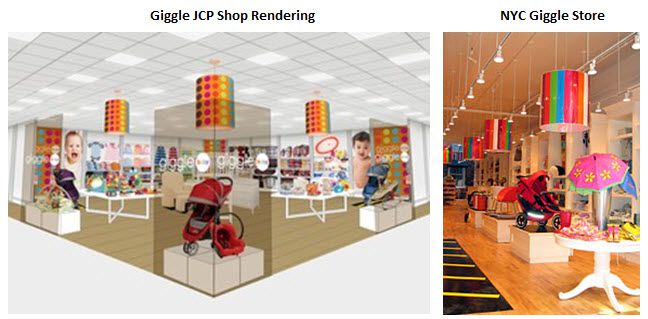

This comes just weeks after JCP announced that it will be opening both Carter’s and Giggle shops for kids. While the Carter’s announcement was largely expected, not much was made of Giggle. We think this presents an underappreciated competitive threat to what is understood as broad channel fill for CRI at Penney's. Now we have Gilt entering the space. This isn’t exactly a direct competitor for CRI, but it’s the second announcement in the past month suggesting the Big 4 in children’s apparel (PLCE, Gymboree, Dressbarn, and Carter’s) are going to see increasing competition for their share of the market.

This is notable for a couple reasons:

- Gilt Groupe isn’t a start-up company/brand making yet another push into the space, but one that is quickly closing in on $1Bn in revenues with a significant online presence. The baby category is one of its largest. If we assume that it accounts for 20% of the business then were talking a retailer with nearly 2% share making a concerted effort to expand.

- Giggle is largely unknown due in part to the fact that it’s a smaller concept with only 13 retail stores – but not for long. At the risk of being anecdotal, we were in a Giggle store for the first time the week before the announcement and remarked at the time at what a great retail concept it was. It’s more one-stop-shop than apparel store, but as a result it’s a grandparents’ and parents’ dream for gifts or simply picking up a ‘couple’ things. It too is at the higher end compared to Carter’s, but they will compete in apparel. More importantly, Giggle will offer shoppers gift giving alternatives to basics that will likely pressure CRI’s traffic at JCP.

With much of Carter’s growth over the last decade coming from Playwear where it competes with Old Navy, the core baby business (36% of sales) has largely been considered untouchable. We won’t argue the merits of CRI’s baby business – we think it’s great, and more importantly, so do the retailers and consumers. But increasing competition at the higher end of its pricing scale and availability of baby products both online and at retail (i.e. Giggle) provides consumers with more alternatives. At a minimum, that keeps the value proposition honest and price in check.

What this ultimately means for CRI is that it will have to spend more to protect its share of the pie. With the company also ramping less productive store growth in order to drive revenues, we see SG&A deleverage over the next three years continuing to pressure operating margins. The Street expects SG&A deleverage this year, but this year only. Based on the factors we’re seeing, we think the dynamics of the baby retail market are starting to change on the margin. As such, the rebound in CRI’s margins are likely to be less profound than expectations currently suggest.