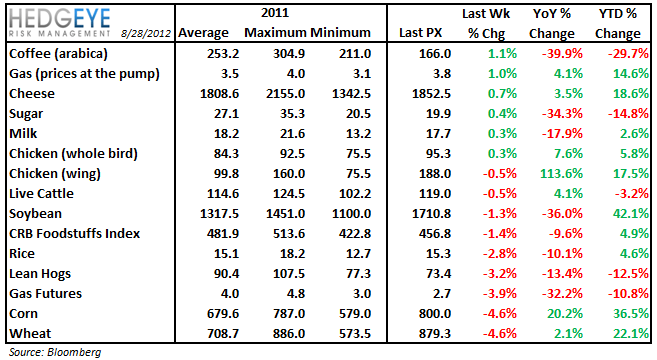

During the most recent earnings season, as we wrote in our recent post titled, “BEAT & MISS TRENDS SHOW TOP LINE IMPORTANCE”, the top line is the key focus for investors in the restaurant space. As we know, the commodity outlook and/or pricing power of restaurant companies are not unrelated. The ability of restaurant companies to raise prices this year is limited given the relationship between CPI for food at home and food away from home. Companies like Darden that are posting decelerating traffic numbers are likely to struggle from a top line perspective and any commodity-related headwinds will only add to the bottom-line impact.

Summary View (charts below)

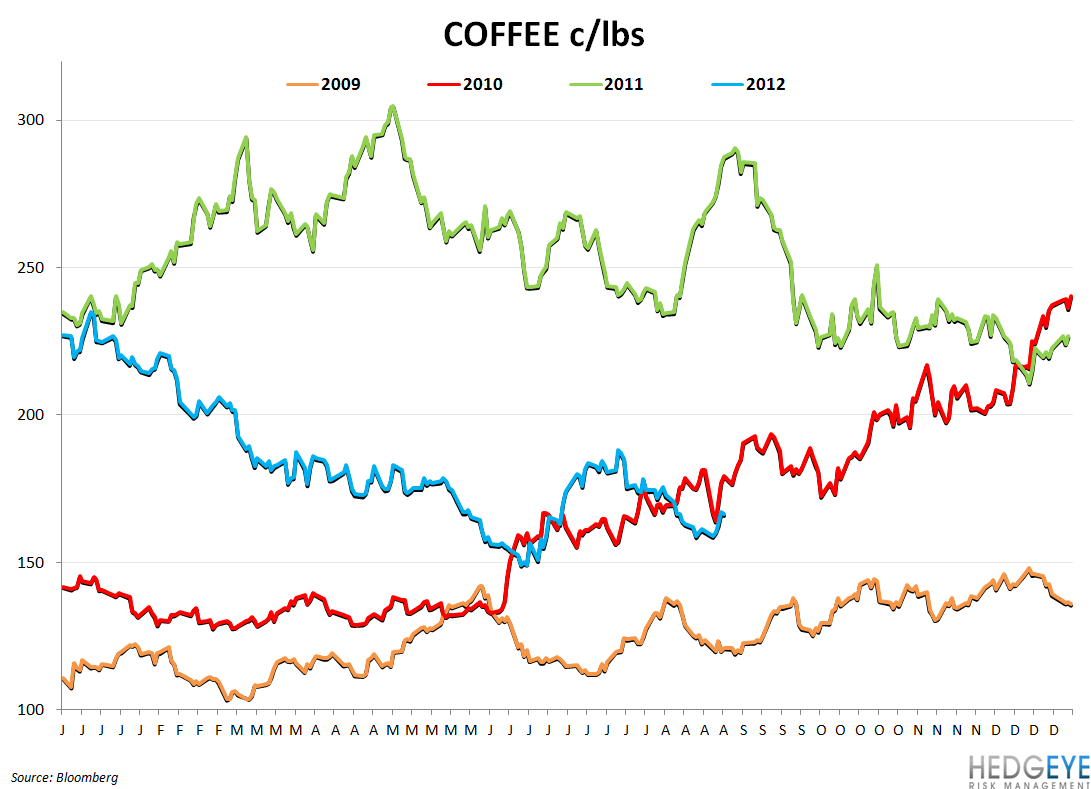

Coffee prices have been the outlier to the upside over the last week, largely due to gains posted yesterday as speculators wagered that Tropical Storm Isaac will “damage beans stored in warehouses in New Orleans”. Robusta coffee is expected to become more expensive in 2012/2013 as demand for the cheaper cousin of Arabica is forecasted to rise roughly 6%, according to Volcafe. All in all, we see the outlook as favorable for Starbucks and other coffee retailers from a coffee cost perspective. (SBUX, DNKN, GMCR, PEET, CBOU, THI)

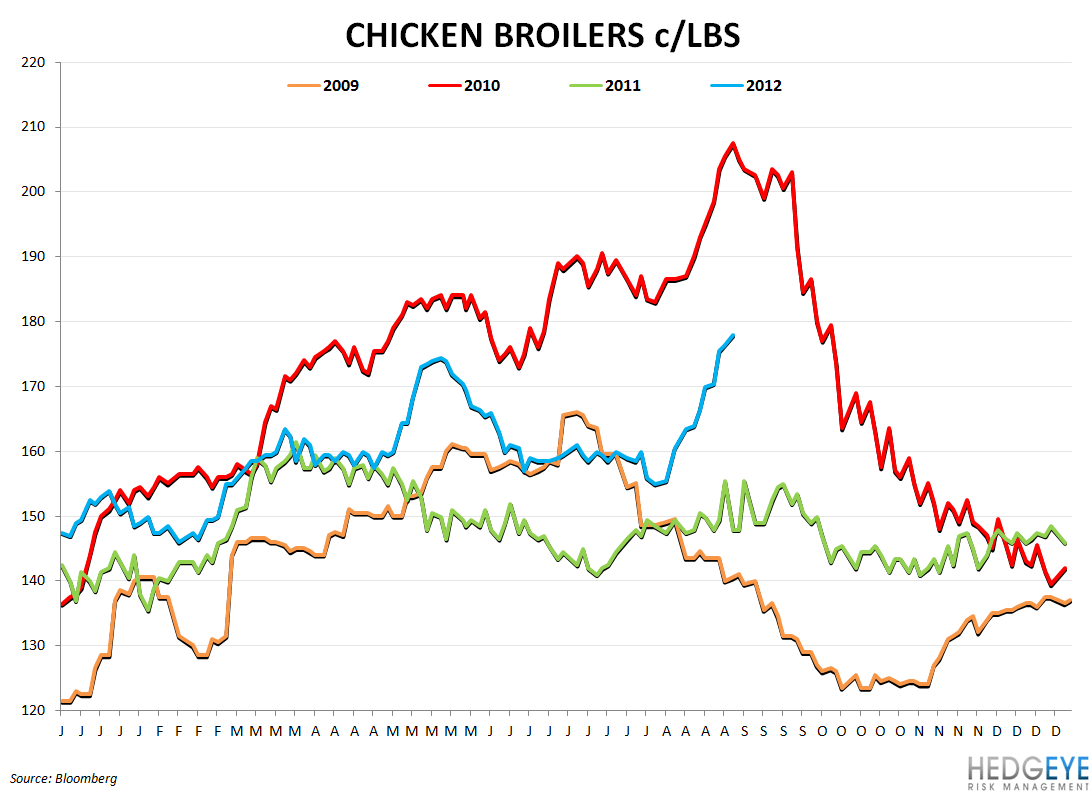

Whole bird chicken prices gained modestly week-over-week. Wing prices did decline somewhat but elevated corn prices spurring food processors (SAFM) to cut back egg production means that BWLD will remain in a difficult position for some time. BWLD CEO Sally Smith said in late July, “This year highest wing prices we've ever seen at a sustained level. Now, there's nothing to indicate that wing prices are going to change.”

Dairy prices (milk and cheese) seem to be moving steadily higher as concerns mount over shrinking herd sizes in the United States. This could be a potential headwind for CAKE which, during the first half of 2012, experienced better-than-anticipated favorability due in part to the price of non-contracted dairy ingredients.

Corn and wheat prices have declined over the past week as speculation mounted that Isaac will bring rains this week to the southern United States, helping to ease drought conditions.

Beef prices have been moving lower recently as the drought has accelerated herd sell-off. Longer-term, inventory numbers suggest continued elevated prices for beef. TXRH, WEN, and JACK all have exposure to spot market beef prices.

Macro Callout

The drought is having an impact on commodity costs in many different ways. This article from Bloomberg describes the difficulty shippers are having moving petroleum, commodities, and goods around inland waterways in the U.S.

“More than 566 million tons of freight valued at $180 billion moved through inland waterways in 2010, including 60 percent of U.S. grain exports, 22 percent of domestic petroleum and 20 percent of the coal used to generate electricity, according to the Waterways Foundation in Arlington, Virginia.”

Correlation

Charts

Howard Penney

Managing Director

Rory Green

Analyst