This note was originally published at 8am on July 27, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“His own men wanted more of the same, the enemy less.”

-Victor Davis Hanson

I am grinding through two books about leadership and war right now – and that probably puts me in a mood to fight. When it comes to going to battle with Fed and ECB ideologies that are perpetuating global #GrowthSlowing, someone has to do it.

In his epic classic “The Soul of Battle”, Victor Davis Hanson tells the story of the great Greek General of Thebes, Epaminondas, and his fight for democracy versus the Spartans. “Thebes now battled for neither money nor power, but for the idea of allowing all Greek states to be autonomous.” (page 87)

Theban farmers taking up arms for their economic freedom was ultimately instigated by the central planning Spartans themselves. “The Spartan takeover of the sacred Theban Cadmen (382BC) – the city’s spiritual and political center – was the most foolhardy foreign enterprise in the entire history of Spartan foreign policy.” (page 28)

It’s different now, but it’s the same.

Our Keynesian overlords are taking over the most pure temple of free market capitalism that remains – our public markets. And while I may get my short-term market calls right and wrong, I will not confuse that risk management duration with my principles. After listening to Draghi’s drivel yesterday, I will not provide him the cowardice of standing idle.

I am here on the front lines of this ideological debate. And I too will do whatever it takes.

Back to the Global Macro Grind…

Undoubtedly, the toughest balance beam to traverse in my head is my absolute disgust for what I hear these people say every day and what it is I need to do in order to not violate Rule #1 (don’t lose money).

We need to keep getting our economic forecasts and risk managed positions right in order to crack these Keynesians right up the middle of their phalanx. Ideologies die on the vine of mediocrity and broken promises.

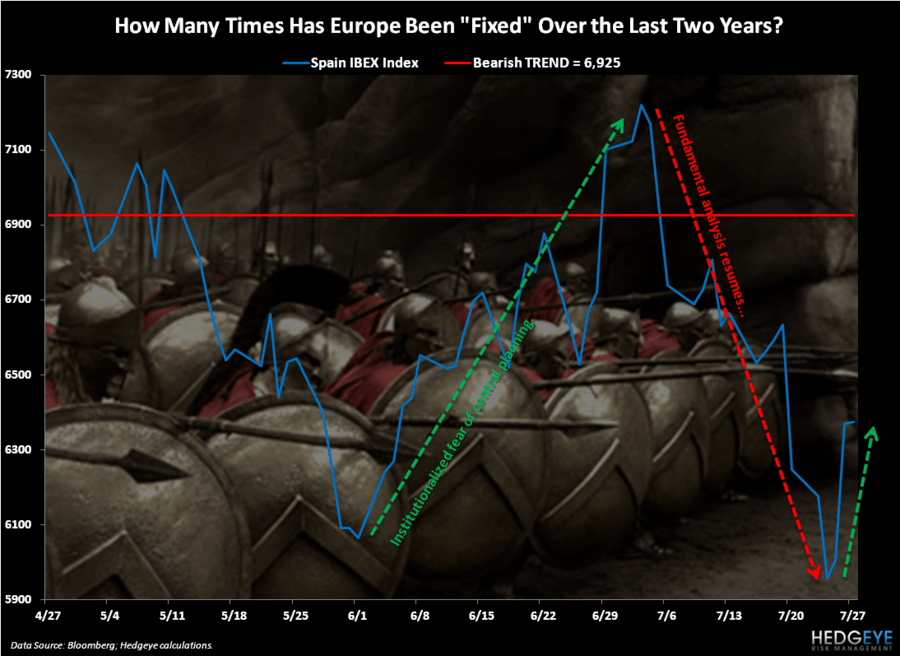

Whether they are coming at us from the ECB or Fed flanks, their ultimate impact can be measured. As you can see in Darius Dale’s Chart of the Day, this is their 2nd major centrally planned attack since June:

- Dollar Down

- Gold Up

- Stocks Up

If you’re going to step on the field with me and my boys, you better realize that winning a few battles doesn’t win you the war. Yesterday, the S&P Futures rallied 27 handles (2 full percentage points) at the stroke of Draghi’s “whatever” shot hitting the tape. Spanish and Italian stocks moved 6-7 full percentage points in less than 3 hours of trading.

That’s normal, right? Bull market.

If I have reminded you of this 100x in the last 5 years, it’s been 1000x. Get the US Dollar right, and you’ll get a lot of other things right. With the US Dollar Index down a full percentage point on the day yesterday, the #BailoutBulls of the 112th Correlation ran wild.

Here’s how our most immediate-term TRADE correlation scored on yesterday’s close (correlation to the USD):

- EuroStoxx 600 Index = -0.82

- SP500 Index = -0.75

- SPX Volatility Index (VIX) = +0.77

In other words, more central planning fire in your Purchasing Power hole continues to do the 2 very things we stand against for The People (24.6% unemployment in Spain this morning) who don’t get paid by food/energy/stock market inflations:

- Shortening Economic Cycles

- Amplifying Market Volatility

They know it. You know it. The People watching this market know it. No matter which side of this battle of ideologies you stand on, the short-term correlation (price action) is being drive by causality (short-term policy reactions).

Their world is built on broken promises. Their bailout policies are designed to inflate asset prices by debauching your hard earned dollars. And now these said leaders of Western Academia’s tallest ivory towers have shot arrows towards the heart of “whatever” they think will have us stand down. Ironically, this is precisely what will make us rise up.

Our men and women want more of the same, the enemy less – and that’s the free-market’s trust.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Spain’s IBEX, and the SP500 are now $1586-1623, $101.91-107.86, $82.52-83.39, $1.20-1.23, 5846-6349, and 1349-1366, respectively.

Enjoy your weekend and best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer