TODAY’S S&P 500 SET-UP – August 8, 2012

As we look at today’s set up for the S&P 500, the range is 26 points or -1.45% downside to 1381 and 0.40% upside to 1407.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

SENTIMENT – two beauty signals registering in the last 24hrs w/ the VIX testing long-term TAIL support (14-15) again and the II Bull/Bear Spread spikes back up to +1810bps wide to the bull side (Bears have been eviscerated from the spread, down to 25.5% vs 27.7% last wk). Big drawdowns in the last 5yrs happen after all the weak shorts have been squeezed out.

- ADVANCE/DECLINE LINE: on 08/07 NYSE 888

- Up versus the prior day’s trading of 765

- VOLUME: on 08/07 NYSE 727.94

- Increase versus prior day’s trading of 12.48%

- VIX: as of 08/07 was at 15.99

- Increase versus most recent day’s trading of 0.25%

- Year-to-date decrease of -31.67%

- SPX PUT/CALL RATIO: as of 08/07 closed at 1.33

- Down from the day prior at 1.54

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 34

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.62%

- Decrease from prior day’s trading of 1.63%

- YIELD CURVE: as of this morning 1.36

- Down from prior day’s trading at 1.37

MACRO DATA POINTS (Bloomberg Estimates)

- 7am: MBA Mortgage Applications, week Aug. 3 (prior 0.2%)

- 8:30am: Nonfarm Productivity, 2Q P, est. 1.4% (prior -0.9%)

- 8:30am: Unit Labor Costs, 2Q P, est. 0.5% (prior 1.3%)

- 10:30am: DoE Inventories

- 11am: U.S. Fed to purchase $1.5b-$2b notes in 2/15/2036 to 5/15/2042 range

- 1pm: U.S. to sell $24b 10-year notes

GOVERNMENT/POLITICS:

- House, Senate not in session

- FDA advisory panel meets to discuss uses, limitations of in vitro dissolution testing, receive update on draft guidance for industry on biosimilars, 8am

- IRS holds meeting on proposed regulations, fees imposed by Patient Protection and Affordable Care Act on issuers, 10am

- International Trade Commission to vote on Ferrovanadium, Nitrided Vanadium imports from Russia, 1pm

- Air Line Pilots Association holds annual safety forum, 8:30am

WHAT TO WATCH:

- McDonald’s sales growth may be slowest since 2009

- Greece outlook revised to negative by S&P; ratings affirmed

- Disney profit rises 24% on “Avengers” as rev falls short

- Standard Chartered probe said to require up to $700m

- Knight Losses Spur Tighter Automated-Trading Rules From SEC

- J.C. Penney puts at record vs peers before earnings

- Ford expands into China heavy truck market with acquisition

- German exports fell in June as crisis curbed euro-area demand

- King seen cutting U.K. outlook as BOE stays open to stimulus

- Apple says Samsung document shows application icons copy IPhone

- Rio Tinto 1H net beats est.

- ING Groep 2Q net misses est.

EARNINGS:

- Lamar Advertising (LAMR) 6am, $0.15

- DISH Network (DISH) 6am, $0.66

- Air Canada (AC/A CN) 6am, C$(0.01)

- EchoStar (SATS) 6am, $0.08

- NRG Energy (NRG) 6:45am, $0.18

- PPL (PPL) 6:53am, $0.41

- Alpha Natural Resources (ANR) 7am, $(0.35)

- BCE (BCE CN) 7am, C$0.81

- International Flavors & Fragrances (IFF) 7am, $1.03

- Carlyle Group (CG) 7am, $(0.04)

- HollyFrontier (HFC) 7am, $2.24

- Molex (MOLX) 7:30am, $0.38

- Apollo Investment (AINV) 7:30am, $0.21

- Brookfield Infrastructure Partners (BIP) 7:30am, $0.34

- Ralph Lauren (RL) 8am, $1.78

- Macy’s (M) 8am, $0.64; Preview

- Computer Sciences (CSC) 8:13am, $0.22

- Liberty Interactive (LINTA) 8:30am, $0.24

- Finning International (FTT CN) 8:55am, C$0.46

- Liberty Media - Liberty Capital (LMCA) 10:45am, $0.73

- Allscripts Healthcare Solutions (MDRX) 4pm, $0.18

- Onex (OCX CN) 4pm, NA

- MEMC Electronics (WFR) 4:01pm, ($0.04)

- Jack in the Box (JACK) 4:01pm, $0.35

- MBIA (MBI) 4:01pm, $0.07

- News Corp. (NWSA) 4:02pm, $0.32

- Monster Beverage (MNST) 4:05pm, $0.61

- Keyera (KEY CN) 4:05pm, $0.40

- Canaccord Financial (CF CN) 4:05pm, (C$0.04)

- Universal Display (PANL) 4:05pm, $0.25

- CenturyLink (CTL) 4:12pm, $0.62

- Dun & Bradstreet (DNB) 4:14pm, $1.43

- Kinross Gold (K CN) 4:15pm, $0.17

- Continental Resources (CLR) 4:15pm, $0.74

- Yamana Gold (YRI CN) 4:29pm, $0.21

- Canadian Apartment Properties REIT (CAR-U CN) 5:05pm, C$0.36

- Integrys Energy Group (TEG) 5:07pm, $0.41

- Sun Life Financial (SLF CN) 5:10pm, C$0.08

- Franco-Nevada (FNV CN) 5:15pm, $0.28

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – the Doctor says he’s out; Copper testing its 1st duration of resistance (3.43 TRADE resistance) and failed this morning, moving lower by -0.7% after the 10yr UST yield backed off yesterday’s highs. Another #GrowthSlowing signal born out of $111 Oil.

- Coal to Drop as Steel Output Slows in BHP Setback: Commodities

- Gas May Revisit $2 as Drop in Supply Glut Slows: Energy Markets

- Clive Said to Miss July Commodities Rally as Brevan Gains

- Sugar Reserve in India at Four-Year High Set to Help Exports

- Rubber Tumbles to Lowest in Almost Three Years on Slowdown Risk

- Oil Drops From Two-Month High in New York as U.S. Demand Eases

- Soybeans, Corn Slide as Rain May Revive Drought-Stricken Crops

- Gold Declines in London as Stronger Dollar Curbs Investor Demand

- Copper Falls as Factory Report May Stoke Debt-Crisis Concern

- Sugar Falls to One-Month Low as Supplies Improve; Cocoa Climbs

- Electricity Seen Overstating China Slowdown as Services Rise

- Copper Traders Make $839 Million Bet on China Boosting Demand

- Alpha Posts $2.23 Billion Quarterly Loss After Taking Charges

- Gold in Euros Seen Climbing to All-Time High: Technical Analysis

- Commodities Daybook: Coal Set to Slump as European Demand Wanes

- Taiwan Sugar Buys 23,000 Tons Corn, 12,000 Tons Soybeans

- Zinc, Lead Traders Probably Added to Bets on Falling Prices

CURRENCIES

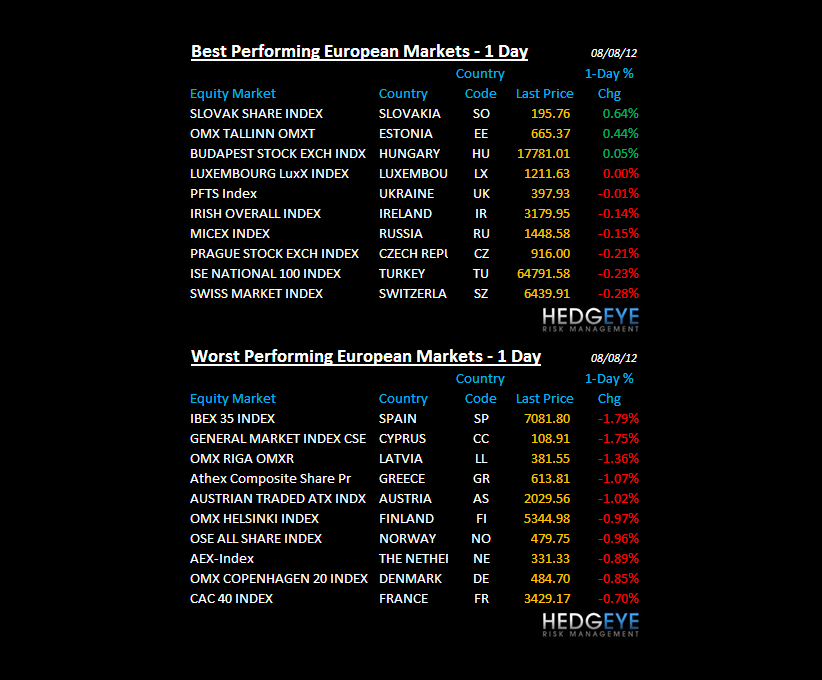

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – Chinese stocks agree; after a paltry “rally” on no volume, the Shanghai Comp closed up, barely, +0.16% last night – but, more importantly, failed at an our immediate-term TRADE line of 2166 resistance; watching that and KOSPI, very closely here. Haven’t been short anything Asia on the meltup, thank god.

MIDDLE EAST

The Hedgeye Macro Team