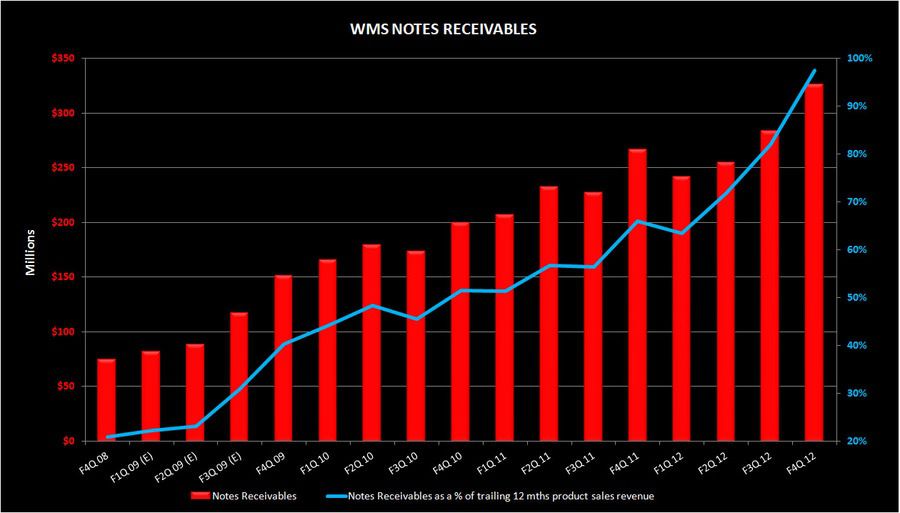

The trend could not be any more clear

- In F4Q, WMS’s new unit sale revenues declined 11% YoY while total receivables increased 22%. On a FY basis, new unit sale revenues fell 17% and total notes receivable increased 22%.

- Over the last 3 years, new unit sale revenues have declined from $375MM to $334MM, or 11%. At the same time, total notes receivable have climbed from $151MM to $325MM, or 116%.

- Within the total notes receivable bucket, long-term receivables have been growing at an alarming rate from just $8MM at June '08 to $122MM in June '12. Over the last 3 years, long-term receivables have increased more than three-fold.