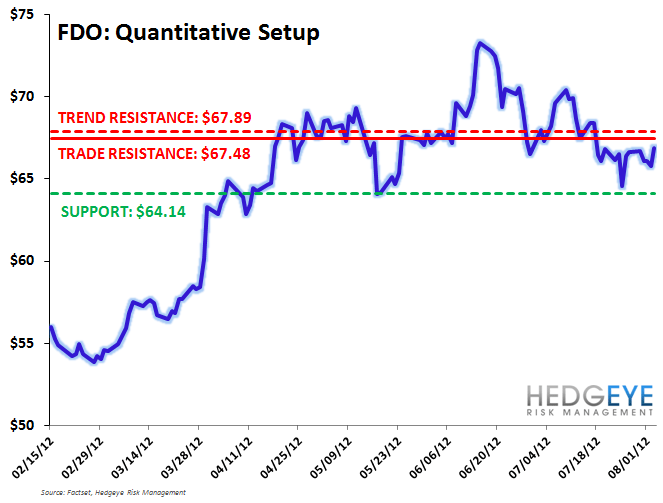

Keith shorted FDO on today’s up-move – central planning isn’t quite the elixir of life should we see $5 at the pump. We remain bearish on the dollar store space; we don’t need Operating Margins to contract in order to build a short case but simply for the prior drivers of expansion to fade.

Last month, we had the pleasure of attending FDO’s analyst day where management left investors with something to be desired offering no change to its long term guidance which was initially provided back at the October 2010 analyst day calling for MSD comps, Operating Margin expansion and double digit EPS growth. Importantly however, with operating margins sitting around ~7.5% over the past 2 years and running flat to potentially down this year, it was notable that there was no clarification on the “operating margin expansion” guidance. When asked in the Q&A to elaborate on what that meant in terms of the magnitude of growth and timeline for expansion, CFO Mary Winston declined to provide additional detail and simply reiterated the qualitative drivers of improved profitability.

Over the past three years, the spread between FDO margins and DG margins, despite both reaching their respective peak levels, has expanded sequentially with FDO now running nearly 300bps below DG. With no additional insight into what levels of operating margins can truly be achieved over the next few years, what does “margin expansion” really mean for FDO as we sit 1 quarter away from a potential year of compression? We definitely think that FDO is a safer place to be on the short side than DG.

Here are some additional thoughts on our thesis:

- Operating Margins have expanded from ~5.7% in 2007 to 7.5% in 2011. At the same time, while a drag on margins, an increase in consumables penetration (from 59% to 67% in 2011 and 68% YTD) has been a traffic tailwind. As an offset, FDO has drastically increased its private label offering from 4% to 25% today and while management expects to enhance its private label offering further, the rate of growth has slowed drastically. FDO does expect to double its private label offering by 2015 via an expanded assortment (which implies penetration just below 40% relative to 25% today), though we’re not so sure private label can continue to increase as a percent of sales as quickly as management expects especially considering the primary category to grow in is consumables.

- Sadly, during the 5 years where margin expansion drove earnings, the percent of Americans on food stamps increased from 9% peaking at 15% last year. Should consumables penetration increase further without a correlated growth in consumers using food stamps as well as private label penetration, gross profitability will continue to deteriorate and strain earnings growth.

- Capital expenditures are expected to run around 7% of sales this year following 3.7%, 2.5% and 2% over the last 3 years respectively due to reaccelerated store growth, an entire chain refresh set to be completed in 2015 and expanded DC capacity. These investments may not be timely given the deceleration in private label penetration and top line growth coming in below both internal and external expectations.

- Finally, management highlighted at its investor day that digital would not become a meaningful part of the business in the foreseeable future. While the consumables business doesn’t necessarily cater to an online model as seamlessly as most other brick and mortar models, the missed opportunity for increased digital penetration to drive margin expansion through a lower cost structure is important nonetheless.

We continue to feel that with operating margins at peak, tailwinds fading, the inability to grow online and management teams offering no new insight into the drivers of future earnings growth, the dollar store space is not a safe place to be.