June could pull GGR growth into negative territory on the year

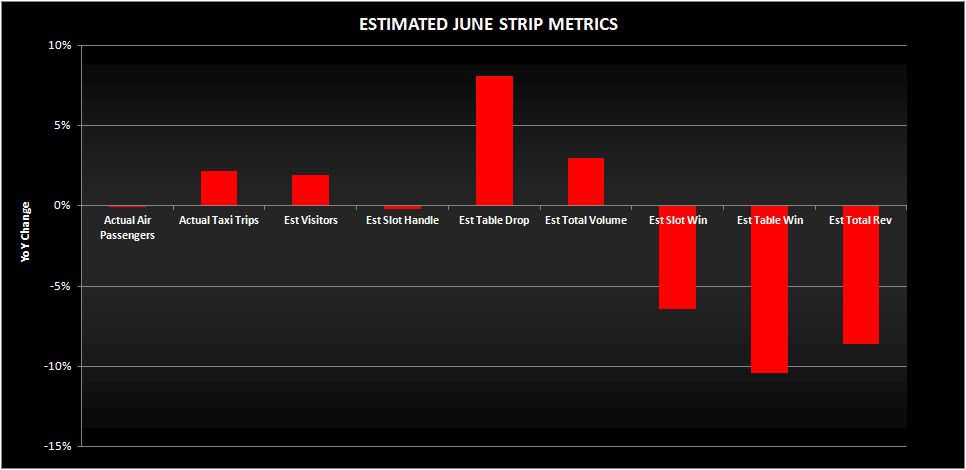

Based on taxi data and McCarran Airport figures, we project that June Strip gross gaming revenues (GGR) fell 6-10% YoY, assuming normal slot and table hold percentages. Baccarat is always the wild card - both hold and volume - but if the Strip falls in our predicted range, June will drive YTD gaming revenue down versus the first half of 2011. Remember that May was disastrous with GGR falling 18%. It has become clear that Vegas is not only in the middle of a modest recovery, the recovery cannot even be called modest and may not even be a recovery.

WYNN and LVS already reported a 33% and 8% drop in GGR, respectively, on the Strip in Q2 2012. Despite their awful revenue performance, we believe WYNN and LVS actually gained volume market share YoY, which means the two gaming operators yet to report earnings - MGM and CZR - probably performed poorly as well.

The number of enplaned/deplaned airport passengers at McCarran fell by 0.1% YoY, the 1st decrease since December 2010. McCarran's expansion into Terminal 3 is ongoing and may help with the ease of transportation and additional capacity. Taxi trips increased 2.2% YoY in June.

June results will also be hurt by lower than normal slot hold due to an accounting rule which defers slot win on the last day to July, since June ends on a Saturday. Moreover, June 2012 faces slightly higher than normal table and slot hold percentages generated in June of 2011.

Here are our projections: