We changed our fundamental stance on Starbucks on June 12th. The reason for this change was a combination of the Hedgeye Macro Team’s call on Global Growth Slowing, the La Boulange acquisition, and our conviction that managing five concepts at once was likely to lead to inefficiency.

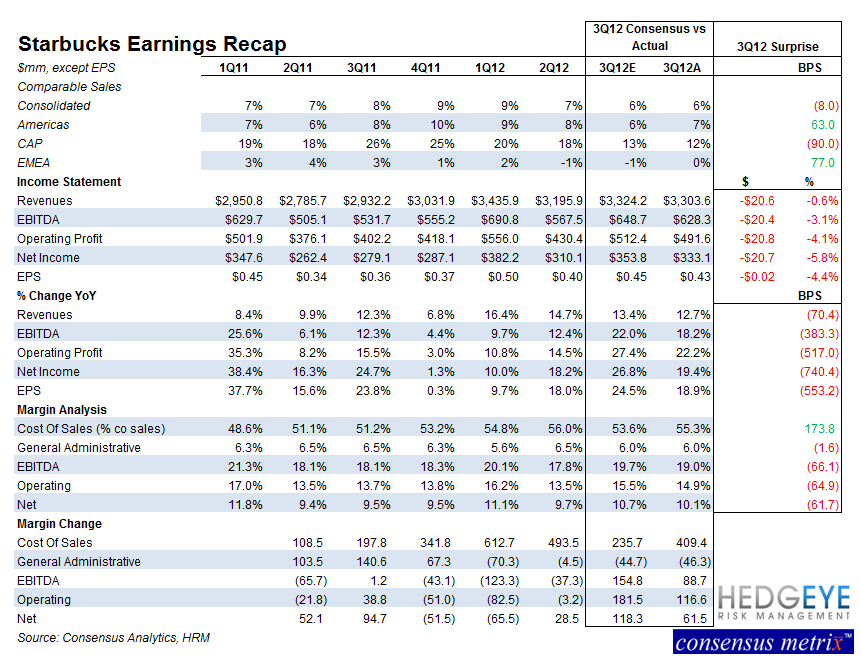

Starbucks reported worse-than-expected 3QFY12 earnings after the close. There were not many positives to salvage from the call other than comps do not look too bad. Given the unmistakable slowing in trends, however, this is scant consolation. The macroeconomic environment is playing a role, certainly, but company specific issues are also a factor.

We will advise our clients to remain on the sidelines until consensus expectations come closer in line with reality. The Starbucks business model is sensitive to economic volatility. Additionally, to become bullish on Starbucks again, we would need to see management focus on fewer concepts. Within its core business, CPG, and its Verissimo home brewer, the company can easily satisfy investor appetite for growth. Increasing the number of “four-wall” concepts under its umbrella is, in our view, not the correct move at this stage. Below is a summary of the quarter with some of our takeaways.

Guidance:

- 4QFY12 revenue growth of 10-12%

- 4QFY12 EPS of $0.44-0.45, growth of 19-22% versus consensus of $0.48

- FY13 targeted revenue growth of 10-13%

- 1,200 net new stores – acceleration in U.S., China, possible acceleration of closures in Europe

- FY13 EPS of $2.04-$2.14 versus consensus of $2.29, according to Consensus Metrix

- FY12 impact of commodity costs remains $230mm

- FY13 is locked for coffee costs through 11 months at favorable prices. ~100m tailwind to operating income

- FY13 new unit growth of 1,000 stores

- Americas +500

- CAP +400

- EMEA +100

3QFY12 Consolidated

- 3QFY12 EPS of $0.43 versus $0.45 consensus represented 19% y/y growth

- Sales increased 13% to $3.3 billion on 6% Global Consolidated comps

HEDGEYE: Consensus was disappointed by 3QFY12 and still needs to lower expectations for FY12 and FY13 to avoid further disappointment. SBUX is one of the most loved names in the industry; sell-side sentiment has a long way to go. Margins should pick up going forward as commodity cost pressure on the P&L eases.

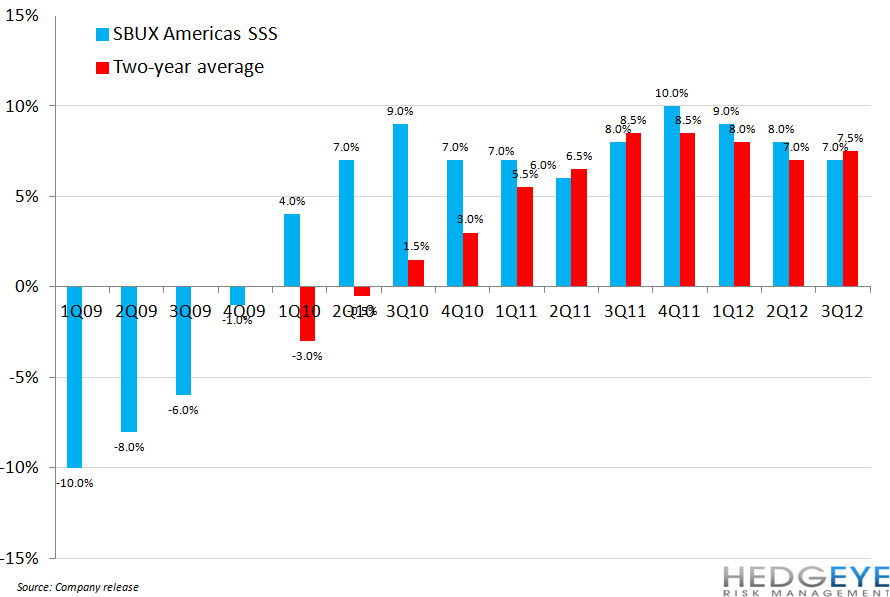

Americas:

- Comps gained 7% during 3QFY12

- Slowing trends in June was primary driver behind EPS miss

- Evolution Fresh drinks in 800+ stores in Seattle, LA, San Diego. Plans to 2x in coming months

- SBUX operates one of the largest mobile payment programs globally. ~1m U.S. payments/week

EMEA

- Mgmt “seeing tangible benefits” of ongoing initiatives in the region but “long road” back

- Seeking to “optimize” portfolio, possibility of increased closures and possible charges

HEDGEYE: The comps and margins in Europe, obviously, imply a dire situation in that geography for Starbucks. Despite management’s apparent determination to turn things around there, we feel it is largely out of the company’s hands. Obviously continuing to operate competitively is crucial, but we believe it could possibly be a sustained period of time before Europe is a meaningful profit-driver again.

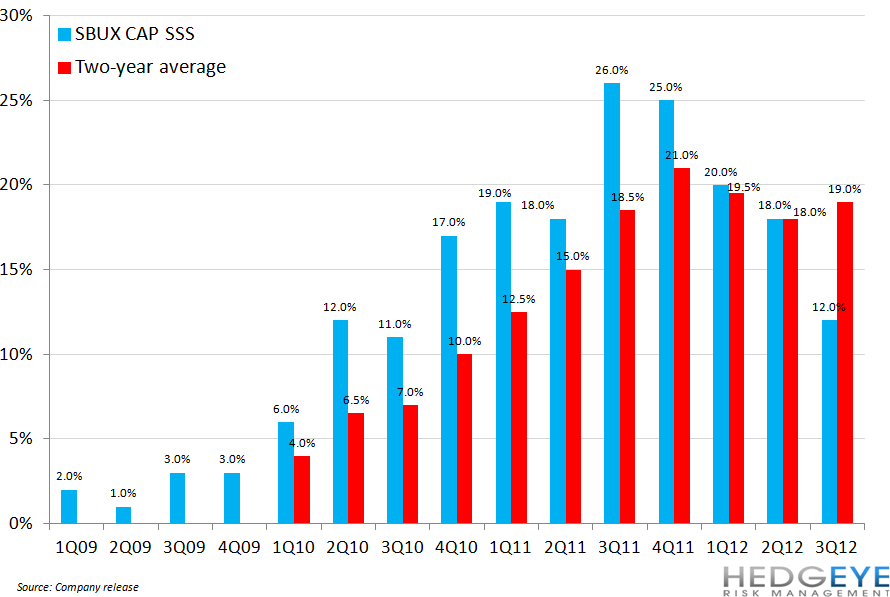

CAP

- On track for 1500 stores on mainland China by 2015

- China representing 1/2 of 400 (up from 300) projected FY12 CAP openings

- Management believe the brand has “turned the corner” in terms of growth in China

- Contribution to company profitability 13% YTD versus 9% two years ago

HEDGEYE: This remains a high-margin, high-growth region for Starbucks that seems to be generating a lot of excitement. Two-year average trends sequentially accelerated in 3QFY12.

CPG & Other

- CPG segment reached $1 billion for first time

- Premium coffee now 50% of total U.S. grocery aisle coffee sales

- Starbucks brands leading with 28.2% share

- Advance commitments for Verissimo from retailers bode well for holiday season

- 15% share of premium single-cup market with more than 230 million cups shipped in 5 months

Howard Penney

Managing Director

Rory Green

Analyst