TODAY’S S&P 500 SET-UP – July 25, 2012

As we look at today’s set up for the S&P 500, the range is 20 points or -0.70% downside to 1329 and 0.80% upside to 1349.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 07/24 NYSE -1477

- Up versus the prior day’s trading of -1601

- VOLUME: on 07/24 NYSE 808.38

- Increase versus prior day’s trading of 8.81%

- VIX: as of 07/24 was at 20.47

- Increase versus most recent day’s trading of 9.94%

- Year-to-date decrease of -12.52%

- SPX PUT/CALL RATIO: as of 07/24 closed at 2.08

- Up from the day prior at 1.23

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 35

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.43%

- Increase from prior day’s trading at 1.39%

- YIELD CURVE: as of this morning 1.22

- Up from prior day’s trading at 1.17

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, July 20 (prior 16.9%)

- 10am: New Home Sales, June, est. 372k (prior 369k)

- 10am: New Home Sales M/m, June, est. 0.8% (prior 7.6%)

- 10:30am: DOE inventories

- 11am: Fed to purchase $4.5b-$5.5b notes due 8/15/20-5/15/22

- 11am: U.S. to sell $35b 5-yr notes

GOVERNMENT:

- House, Senate in session

- Senate Finance holds hearing on education tax Incentives, 10am

- Senate Commerce holds hearing on short-supply prescription drugs, 2:30pm

- House Education and Workforce Committee holds hearing on proposals to strengthen National Labor Relations Act, 10am

- Senate Appropriations hears from Education Secretary Arne Duncan on effects of budget cuts on education, 10am

- Senate Foreign Relations holds hearing on increasing trade with Africa, 3pm

- House Armed Services panel holds hearing on military capabilities for cyber operations, 3:30pm

- Treasury Secretary Tim Geithner presents annual report of FSOB at House Financial Services hearing, 9:30am

- Peregrine Financial’s collapse amid shortfall in customer funds will be examined at House Agriculture hearing on oversight of swaps,, with CFTC Chairman Gary Gensler, 10am

- Sen. Richard Shelby, R-Ala., speaks at U.S. Chamber of Commerce event on financial regulatory reform, 1pm

WHAT TO WATCH:

- Apple shrs tumble as earnings, forecasts miss analyst ests.

- Netflix plunges on guarded outlook for new 2012 subscribers

- Ancestry.com said to discuss buyout with Providence

- New U.S. home purchases may have risen to 371k annual rate in June, most since April 2010

- C.R. Bard told by jury to pay $5.5m over vaginal-mesh implant

- Food inflation may rise 4.5% in 2013 on worst drought since ’50s

- Wells Fargo ranks No. 1 in hardest-to-value securities: S&P

- Perella said to be hired in Morgan Stanley, Citigroup price rift

- U.K. GDP falls most in 3+ yrs; 2Q GDP falls 0.7%, median forecast 0.2% decline

- German business confidence fell 3rd straight month in July to lowest since March 2010

- Spanish, Italian notes rise on bets ECB may boost rescue fund

- IMF says China downside risks significant as growth slows

- Japan June exports fall 2.3% Y/y vs. est. 3% drop

- Nintendo 1Q net loss 17.23b yen, analyst est. 16.4b yen loss

- ECB’s Nowotny sees arguments for giving ESM banking license

EARNINGS:

- TE Connectivity (TEL) 6am, $0.78

- WellPoint (WLP) 6am, $2.08; Preview

- Encana (ECA CN) 6am, $0.19; Preview

- Thermo Fisher Scientific (TMO) 6am, $1.16

- Cenovus Energy (CVE CN) 6am, C$0.53

- Praxair (PX) 6:02am, $1.42

- Regeneron Pharmaceuticals (REGN) 6:30am, $0.50

- Wyndham Worldwide (WYN) 6:30am, $0.84

- Eli Lilly & Co (LLY) 6:30am, $0.77

- Alexion Pharmaceuticals (ALXN) 6:30am, $0.36

- Tupperware Brands (TUP) 7am, $1.27

- General Dynamics (GD) 7am, $1.74

- Motorola Solutions (MSI) 7am, $0.69

- US Airways Group (LCC) 7am, $1.55; Preview

- AOL (AOL) 7am, $0.23

- PepsiCo (PEP) 7am, $1.10

- Northrop Grumman (NOC) 7am, $1.61

- Rockwell Automation (ROK) 7am, $1.31

- Lorillard (LO) 7am, $2.32

- Nasdaq OMX Group (NDAQ) 7am, $0.60

- Ford Motor Co (F) 7am, $0.29; Preview

- Corning (GLW) 7am, $0.31

- Nielsen Holdings NV (NLSN) 7am, $0.41

- RadioShack (RSH) 7am, $0.04

- MeadWestvaco (MWV) 7:05am, $0.39

- Canadian Pacific Railway Ltd (CP CN) 7:30am, C$0.85

- Caterpillar (CAT) 7:30am, $2.29

- Hess (HES) 7:30am, $1.38

- IAC/InterActiveCorp (IACI) 7:30am, $0.71

- Bristol-Myers Squibb Co (BMY) 7:30am, $0.48; Preview

- Southern Co (SO) 7:30am, $0.68

- JetBlue Airways (JBLU) 7:30am, $0.16

- Airgas (ARG) 7:30am, $1.15

- T Rowe Price Group (TROW) 7:30am, $0.81

- Delta Air Lines (DAL) 7:30am, $0.68

- Boeing Co (BA) 7:30am, $1.13; Preview

- Omnicare (OCR) N , 7:31am, $0.79

- ConocoPhillips (COP) 8am, $1.19; Preview

- Level 3 Communications (LVLT) 8am, $(0.23)

- Cooper Industries PLC (CBE) 8am, $1.12

- Loblaw Ltd (L CN) 8am, $0.60

- Canadian National Railway Co (CNR CN) 8am, C$1.47

- Akamai Technologies (AKAM) 4pm, $0.37

- Las Vegas Sands (LVS) 4pm, $0.60

- Torchmark (TMK) 4pm, $1.30

- LSI (LSI) 4:01pm, $0.17

- Varian Medical Systems (VAR) 4:01pm, $0.93

- AvalonBay Communities (AVB) 4:01pm, $1.34

- Owens-Illinois (OI) 4:02pm, $0.76

- Stericycle (SRCL) 4:02pm, $0.80

- Whole Foods Market (WFM) 4:03pm, $0.61

- Symantec (SYMC) 4:04pm, $0.38

- Everest Re Group Ltd (RE) 4:05pm, $3.83

- Zynga (ZNGA) 4:05pm, $0.06

- Citrix Systems (CTXS) 4:05pm, $0.60

- Angie’s List (ANGI) 4:05pm, $(0.39)

- Lam Research (LRCX) 4:05pm, $0.65

- Visa (V) 4:05pm, $1.45

- Ameriprise Financial (AMP) 4:05pm, $1.34

- Tesla Motors (TSLA), 4:06pm, $(0.94)

- Western Digital (WDC) 4:15pm, $2.45

- Cheesecake Factory (CAKE) 4:15pm, $0.49

- Assurant (AIZ) 4:15pm, $1.41

- Equity Residential (EQR) 4:25pm, $0.68

- Community Health Systems (CYH), 4:30pm, $0.89

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- China to Flood Steel Market Hurting ArcelorMittal: Commodities

- Exxon Seen Leading Drop in Oil Earnings on Lower Prices: Energy

- Oil Near Lowest in a Week on U.S. Stockpile Gain, China Concern

- LME Shareholders Approve HKEx’s $2.2 Billion Takeover Offer

- Midwest Drought Impact Reaches Indonesia as Soybean Levy Ends

- Corn Rises, Erasing Drop, as Rains May Fail to Reverse Losses

- Gold Advances for Second Day on European Debt Crisis Concerns

- Germany Lowers Gold Holdings for First Time in Eight Months

- Copper Seen Falling as IMF Warns of Risks to China’s Economy

- East Iowa Corn, Soy Yields Plunge From 2011, Doane Tour Shows

- South Korea Considering Stockpiling Corn, Wheat, Soybeans

- Oil Import Peak in China Set to Curb Brent Rally: Energy Markets

- Fertilizer Maker Seeks Canadian Potash Mines: Corporate India

- Chinese Steel Exports Rise to Two-Year High

- Sugar Rises on Speculation of a Surplus Cut; Coffee Declines

- Food Inflation Seen Rising 4.5% in 2013 as Drought Sears Crops

- North Dakota Spring Wheat Yields Seen Climbing on Early Planting

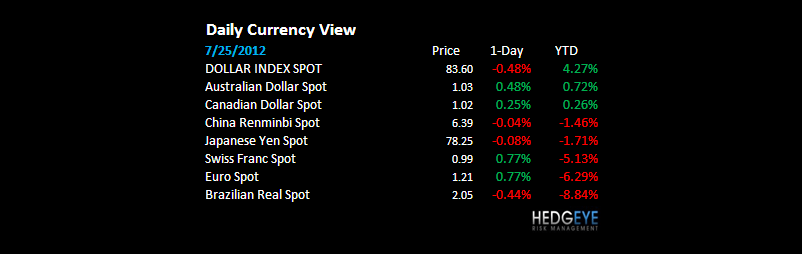

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team