TODAY’S S&P 500 SET-UP – July 17, 2012

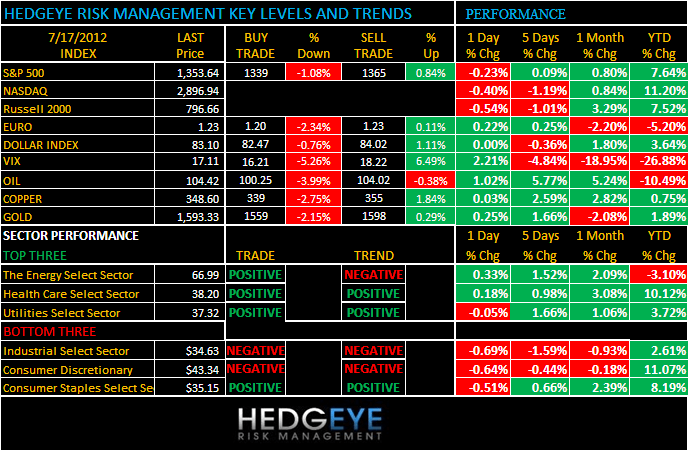

As we look at today’s set up for the S&P 500, the range is 26 points or -1.08% downside to 1339 and 0.84% upside to 1365.

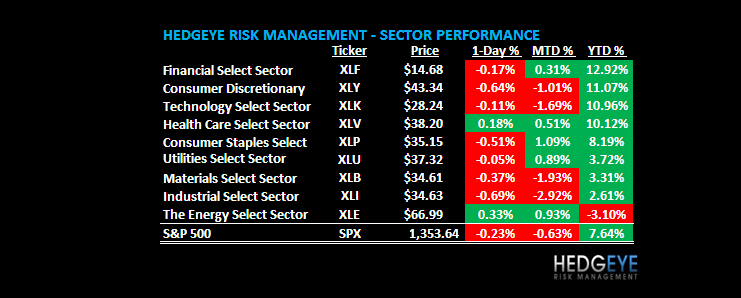

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 07/16 NYSE -306

- Down versus the prior day’s trading of 2044

- VOLUME: on 07/16 NYSE 602.07

- Decrease versus prior day’s trading of -11.85%

- VIX: as of 07/16 was at 17.11

- Increase versus most recent day’s trading of 2.21%

- Year-to-date decrease of -26.88%

- SPX PUT/CALL RATIO: as of 07/16 closed at 1.47

- Down from the day prior at 1.62

CREDIT/ECONOMIC MARKET LOOK:

BERNANKE – what started slowing growth, globally, in late Feb early March was Bernanke’s pushing of the goal posts on 0% money to 2014; oil ripped and consumption growth slowed – so, now the Qe people want more of that? Brent Oil busting back towards $104 this morning is only going to compound the #GrowthSlowing problem in July.

- TED SPREAD: as of this morning 36

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.48%

- Increase from prior day’s trading at 1.47%

- YIELD CURVE: as of this morning 1.25

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook retail sales

- 8:30am: Consumer Price Index M/m, June, est. 0.0% (prior -0.3%)

- 8:30am: CPI Ex Food & Energy M/m, June, est. 0.2% (prior 0.2%)

- 9am: Total Net TIC Flows, May (prior -$20.5b)

- 9am: Net Long-term TIC Flows, May, est. $41.3b (prior $25.6b)

- 9:15am: Industrial Production, June, 0.3% (prior -0.1%)

- 9:15am: Capacity Utilization, June, 79.2% (prior 79.0%)

- 10am: NAHB Housing Market Index, July, est. 30 (prior 29)

- 10am: Bernanke delivers monetary policy report to Senate

- 11am: Fed to sell $7b to $8b notes maturing Feb. 15, 2014- Aug. 31, 2014

- 11:30am: U.S. to sell $ 4-week bills

- 1:15pm: Pianalto speaks on economy in Erie, Pennsylvania

- 4:30pm: API inventories

GOVERNMENT:

- House, Senate in session

- HSBC officials appear before Senate Homeland Security subcommittee to testify on lapses in London-based bank’s money-laundering controls

- Bernanke will discuss the outlook for economy, U.S. central bank monetary policy in semi-annual report to Congress

- CFTC Chairman Gary Gensler testifies before Senate Agriculture on Dodd-Frank, consumer protections; Robert Cook, SEC’s director of trading, also gives testimony

- Committee for a Responsible Federal Budget holds event on debt reduction at National Press Club, with Dave Cote, CEO of Honeywell International; Larry Fink, CEO of BlackRock; Paul Stebbins, CEO of World Fuel Services, 2pm

- Bloomberg Government hosts breakfast with Southern Co. CEO Thomas Fanning; NextEra Energy Chairman Lew Hay; NV Energy CEO Michael Yackira, 8am

- FERC, Energy Dept. hold technical conference on small generator interconnection agreements, 9am

- Senate Energy holds hearing on protecting the electric grid from cyber attacks, 10am

- House Energy panel holds hearing on alternative fuels, vehicles, 3pm

- U.S. International Trade Commission meets on third review of stainless steel bar from Brazil, India, Japan, Spain, 11am

- Former Fed Chairman Paul Volcker speaks at State Budget Crisis Task Force discussion, 11am

WHAT TO WATCH:

- Yahoo names Google’s Marissa Mayer as CEO

- Joblessness issue prompts Fed to shift its focus as Bernanke set to testify to Senate committee today

- Fed’s George says U.S. growth may not exceed 2% in 2012

- Spain borrowing costs fall at 12-month bill auction

- U.K. inflation falls to 2.4%, lowest rate in 2 1/2 yrs

- HSBC probe shows bank allowed laundering, dodged Iran sanctions

- Libor manipulation losses probed by 5 state AGs

- Consumer price index in June probably was little changed

- US Airways, American Eagle pilot leaders to meet: union

EARNINGS:

- Host Hotels & Resorts (HST) 6am, $0.33

- Mattel (MAT) 6am, $0.21

- Comerica (CMA) 6:40am, $0.62

- Mosaic (MOS) 7am, $1.15

- Omnicom Group (OMC) 7am, $1.01

- Goldman Sachs (GS) 7:30am, $1.18

- State Street Corp (STT) 7:17am, $0.97

- Coca-Cola (KO) 7:30am, $1.19; Preview

- TD Ameritrade Holding (AMTD) 7:30am $0.26

- Johnson & Johnson (JNJ) 7:45am $1.29; Preview

- Forest Laboratories (FRX) 8am, $0.32; Preview

- Kansas City Southern (KSU) 8am, $0.84

- M&T Bank Corp (MTB) 8am, $1.69

- McMoRan Exploration Co (MMR) 8am, $(0.13)

- Charles Schwab (SCHW) 8:45am, $0.18

- Intel Corp (INTC) 4:01pm, $0.52

- CSX Corp (CSX) 4:01pm, $0.47

- Wynn Resorts (WYNN) 4:02pm, $1.49

- Yahoo (YHOO) 4:05pm, $0.23

- Albemarle (ALB) 4:05pm, $1.22

- Fidelity National Info Svcs (FIS) 4:05pm, $0.59

- United Rentals (URI) 4:15pm, $0.50

- AAR (AIR) 4:24pm, $0.46

- Fulton Financial (FULT) 4:30pm, $0.20

- Cathay General Bancorp (CATY) 4:30pm, $0.32

- MB Financial (MBFI) Late, $0.38

- Equity Lifestyle Properties (ELS) Late, $1.02

- Ironwood Pharmaceuticals (IRWD) Unknown time, $(0.31)

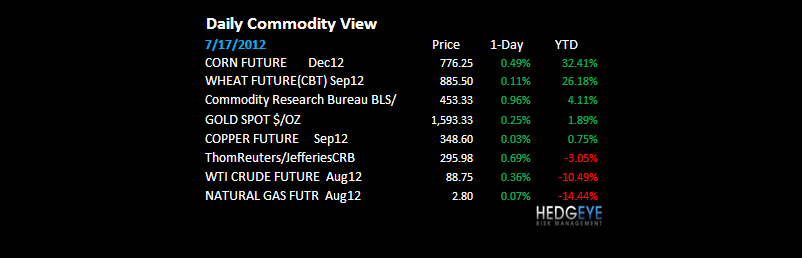

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – Oil looks different than Gold coming out of the weekend’s Israel/Iran chatter; there is nothing that will slow the world’s marginal real-consumption growth than higher oil prices; rising food/oil prices also puts further Chinese rate cuts on hold don’t forget.

- Good Dirt Gone Dry Wilting Corn as Food Costs Gain: Commodities

- Oil Supplies Decline for Fourth Week in Survey: Energy Markets

- Oil’s Center of Gravity Shifts Toward Asia: Chart of the Day

- Rio Tinto CEO Closely Watching Economic Turmoil as China Slows

- Oil Near Seven-Week High on Iran Tensions, Stimulus Speculation

- Corn Slides From 13-Month High as Demand Slows for Fuel and Feed

- Gold Set to Gain in London on Speculation Over Further Stimulus

- Copper Seen Rising Ahead of U.S. Data and Bernanke Testimony

- Sugar Falls on Surplus Outlook; Cocoa Gains on El Nino Concerns

- Iron Ore Drops to Lowest Price Since May as Chinese Demand Wanes

- Rubber Gains as China May Add Stimulus, Thailand Boosts Support

- Palm-Oil Refining Capacity Seen Climbing 24% in Indonesia

- Zinc Poised for 9% Rally on TD Buy Signal: Technical Analysis

- Mosaic Doubles Dividend as Profit Beat Estimates on Planting

- Soybean Acres in India to Climb as Record Prices Boost Planting

- Palm-Oil Options Seen Boosting Futures Volume on Malaysia Bourse

CURRENCIES

US DOLLAR – get the Dollar right and you’ll get today/tomorrow right; watching that closely into and around Bernanke at 10AM EST; if we had to bet (we don’t, so we won’t take a position until we see the river card), USD and Gold are saying Bernanke doesn’t deliver the drugs. USD remains in a Bullish Formation and Gold a Bearish one.

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team