TODAY’S S&P 500 SET-UP – July 12, 2012

As we look at today’s set up for the S&P 500, the range is 21 points or -0.63% downside to 1333 and 0.94% upside to 1354.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 07/11 NYSE 75

- Up versus the prior day’s trading of -955

- VOLUME: on 07/11 NYSE 767.99

- Increase versus prior day’s trading of 5.55%

- VIX: as of 07/11 was at 17.95

- Decrease versus most recent day’s trading of -4.11%

- Year-to-date decrease of -23.29%

- SPX PUT/CALL RATIO: as of 07/11 closed at 1.10

- Down from the day prior at 1.69

CREDIT/ECONOMIC MARKET LOOK:

10YR – fresh new #GrowthSlowing lows for the 10yr yield at 1.49% this morning and that’s really bad for the Financials, as the Yield Spread (10s/2s) also hits new lows at +123bps wide; not clear if Dimon’s fireside chat w/ the sell side’s finest tomorrow will change the economic gravity of the matter – the Yield Spread has never not gone back to flat in a big cycle (see 60yr chart from our deck yesterday).

- TED SPREAD: as of this morning 36

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.48%

- Decrease from prior day’s trading at 1.52%

- YIELD CURVE: as of this morning 1.23

- Down from prior day’s trading at 1.26

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Import Price Index M/m, June, est. -1.8% (prior -1%)

- 8:30am: Initial Jobless Claims, July 7, est. 370k (prior 374k)

- 9:45am: Bloomberg Consumer Comfort, July 8 (prior -37.5)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas change

- 11am: Fed to sell $7b-$8b coupon securities in 7/15/2013 to 1/31/2014 range

- 1pm: U.S. to sell $13b 30-yr bonds (reopening)

- 2pm: Monthly Budget Stmt, June, est. $60b (prior $43.1b)

- 2pm: NAHB midyear forecast

- 3:40pm: Fed’s Williams speaks in Portland, Ore.

GOVERNMENT:

- House, Senate in session

- Senate Energy meets to review progress on eliminating environmental hazards at abandoned National Petroleum Reserve oil wells in Alaska, 9:30am

- House Energy panel holds hearing on proposed legislation to limit government programs backing alternative energy, 9:15am

- House Science panel holds hearing on spurring economic growth through NASA-derived technologies, 10am

- Dept. of Labor to announce settlement with BP regarding 2005 explosion at Texas City refinery, 11am

WHAT TO WATCH:

- Yahoo! holds annual meeting today

- Yahoo! expected to name Levinsohn CEO: LA Times

- Blackstone teams up with investors for ING Asia insurance bid

- Supervalu sinks on strategic review, dividend suspension

- Peregrine customers’ claims priced at 25 cents on dollar

- ECB says overnight deposits fall to lowest in 7 mos.

- Maple, TMX Group obtain recognition orders from BCSC, ASC

- Dentsu buys Aegis in $4.9b deal to create global media, marketing network

- Peugeot shuts France plant, cuts extra 8,000 jobs; GM owns 7% of Peugeot

- JPMorgan is No. 1 stock picker in buy-side survey

- CFTC poised to adopt client-fund safeguards after MF Global

- DirecTV, Viacom talks continue as channels stay dark

EARNINGS:

- Cogeco Cable (CCA CN) 6am, C$1.06

- Cogeco (CGO CN) 6am, C$0.99

- Corus Entertainment (CJR/B CN) 7am, C$0.49

- Fastenal (FAST) 7am, $0.37

- Astral Media (ACM/A CN) 7:55am, C$1.01

- Progressive (PGR) 8:30am, $0.27

- Commerce Bancshares (CBSH) 9am, $0.72

- Novagold (NG CN) 9:15am, $(0.06)

- Resources Connection (RECN) 4pm, $0.72

- Bank of the Ozarks (OZRK) 6pm, $0.52

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

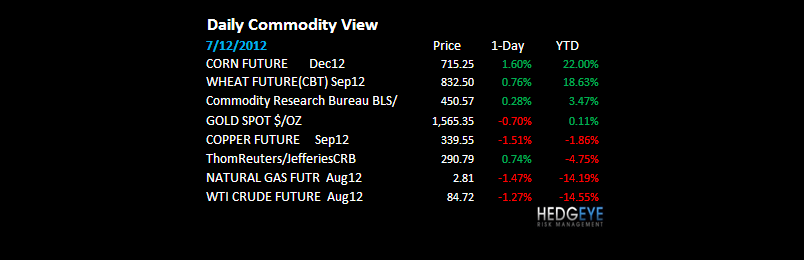

- Gold 22% Rally to Record Seen by Sprott Amid Debt: Commodities

- Refineries Doubling Shutdowns Signals Oil Slide: Energy Markets

- Oil Falls on Signs Faltering Economy Is Eroding Fuel Consumption

- Cocoa Declines After Drop in European Cocoa Grind; Sugar Gains

- Goldman Lifts Grain-Price Forecasts as Drought Withers Fields

- Gold Retreats as Fed’s Minutes Lack Additional Stimulus Signal

- South African Platinum Output Falls for 11th Month on Prices

- Aid Welcomed by Drought-Stricken States as Losses Seen Worsening

- China Crushers Buy More Local Soybeans as Cost of Imports Jumps

- Cooking-Oil Imports by India Fall as Rupee Drop Deter Buyers

- Palm Oil Drops for a Third Day on Concern Slowdown Curbs Demand

- Sandfire Proves Cheapest Copper Target on First Profit: Real M&A

- Russia’s Stavropol Region Is Seen Reaping 40% to 45% Less Grain

- IEA Sees Global Oil Demand Growth Pickup in 2013 on Economy

- Copper Seen Falling Amid Further Signs of Worldwide Slowdown

- Corn Advances After USDA Cuts Outlook on U.S., World Harvests

CURRENCIES

EUROPEAN MARKETS

ITALY – Mario wasn’t kidding; it’s time to get out – the MIB Index -1.1% leads losers this morning and moves right back into crash mode (> 20% peak/trough decline YTD); Italy looks more suspect here than Spain – we went through why its size concerns us on our Q3 Macro Themes Call yesterday – email us if you missed the call and want the replay/slides.

ASIAN MARKETS

KOSPI – continues to be one of our most stealth leading indicators for Global Growth (particularly for Industrials and Tech), and apparently the South Koreans agree w/ us – they cut rates for the 1st time in 3yrs last night – and, contrary to popular #BailoutBull beliefs, that was not good for Asian stocks; KOSPI down hard on that -2.3% (Bearish Formation).

MIDDLE EAST

The Hedgeye Macro Team