“Under capitalism, man exploits man, under communism, it’s just the opposite.” –John Kenneth Galbraith

Q3 Themes:

Inflation trades are over. Bubbles will continue to pop.

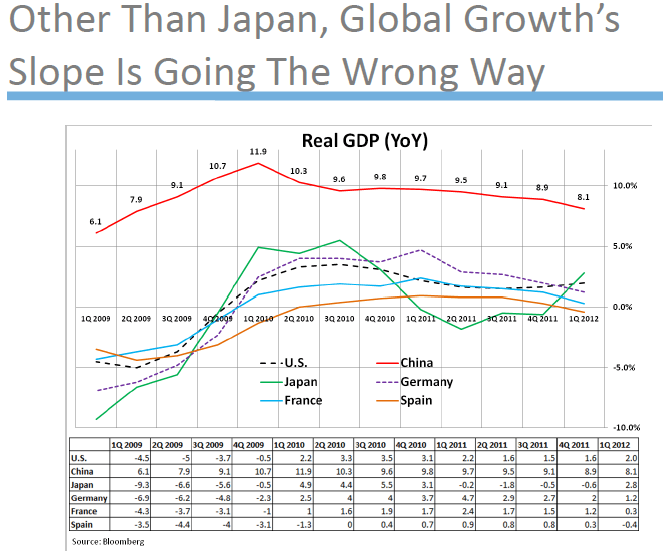

Growth Slowing: It’s about getting the slope of growth right. Get that right, you get a lot of other things right. People need to see growth. Short industrials since March 12.

The question is: are you bearish enough on growth?

Why not $60 oil? Brent bearish against all 3 durations. USD Index to 90s? Highly unlikely. Keith thinks it could happen. At $60 oil, I’ll be really bullish.

SPX hasn’t broken 1286 tail line. If you break 1286, you goto the 1100 line and get really bearish. Trade the range up to 1365.

Gold is on life support. Is the Fed out of bullets? We need to know the answer to this question. Gold is addicted to quantitative easing and expectations. If the USD Index continues higher, watch out for $1100 gold. A lot of hedge funds are caught up in gold and the GLD ETF and it does not bode well for them.

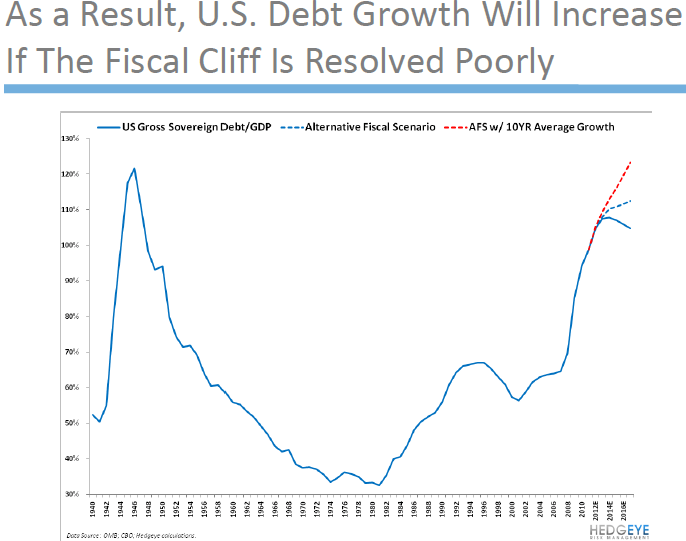

The Fiscal Cliff has two parts. Spending cuts and tax hikes have perpetuated The Cliff. Politicians manage career risk for themselves.

The US debt growth will increase if The Cliff is resolved poorly. If the can is kicked down the road, US will look like France. Congress needs to avoid massive tax increases, negotiate another debt ceiling compromise. Good luck with that.

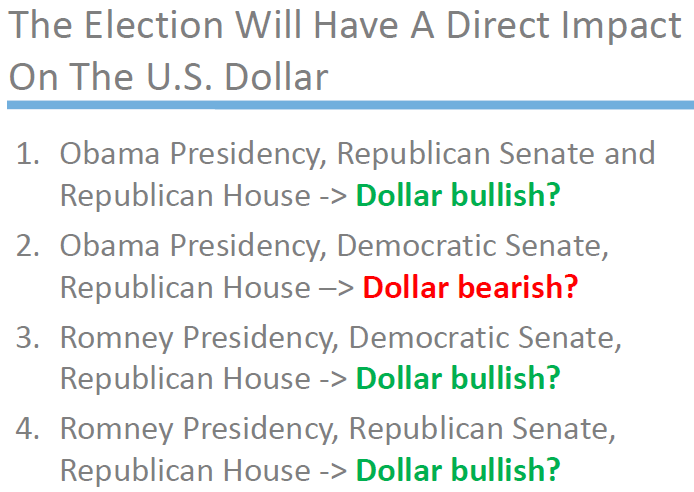

Get rid of Bernanke, you’ll see stocks rip. Definitely not priced in that Romney could win the presidency. Obama separating himself from Bernanke could win him the election. Not likely, though.

More debt will not bring growth. They need to get a handle on things in Europe. We’re very low with the EUR/USD now. It could even go to parity.

LIE-BOR will disrupt the entire industry.

If you’d like access to this morning’s Q3 Big Macro Themes call, please email sales@Hedgeye.com.