-- For specific questions on anything Europe, please contact me at to set up a call.

No Current Positions in Europe

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +1.9% week-over-week vs +1.0% last week. Top performers: Russia (RTSI) +7.0%; Norway +4.9%; Belgium +4.8%; Italy +4.5%; Ireland +3.5%; France +3.4%; Austria +3.4%; Spain +3.3%. Bottom performers: Cyprus -10.8%; Slovakia -0.8%; Ukraine -0.3%; Finland -0.0%; Portugal +0.1%; Greece +0.5%.

- FX: The EUR/USD is UP +0.69% week-over-week vs -0.59% last week. W/W Divergences: RUB/EUR +1.52%, PLN/EUR +1.27%, CZK/EUR +0.99%, HUF/EUR +0.62%; SEK/EUR +0.62%; CHF/EUR -0.03%; GBP/EUR -0.06%; TRY/EUR -0.31%, NOK/EUR -0.65%, RUB/EUR -1.84%.

- Fixed Income: 10YR Yields came in day-over-day pretty dramatically and showed a mixed picture on the week. On the day Greece and Spain fell -66bps to 25.83% and 6.33%, respectively. Italy fell -40bps on the day to 5.82%. On the week, Greece saw the biggest move to the downside, falling -123bps. Spain fell -20bps on the week, while Portugal gained +62bps to 10.16% and the other countries we track were largely flat. On the month German yields are up +23bps to 1.58%.

“Not in my Lifetime”

Zee EU Summit concludes today. Interestingly, we saw quite a sustained relief rally today on the back of the statement’s release this morning [Italy +6.6%; IBEX +5.7%; Greece +5.7%; CAC +4.8%; DAX +4.3%; and EUR/USD +1.7% day-over-day]. While today’s rally doesn’t look dissimilar to rallies around releases of major bailout packages for Europe’s periphery since May 2010, we believe this rally will not have legs. Why?

Unfortunately, it’s both what today’s release didn’t address and intentionally dodged that confirms Europe is far from out of the dark crisis; the results are far from anything near a “bazooka” that could set markets on a sustained up trend. Keep in mind that today’s entire statement is three paragraphs long! It’s not that we’re looking for a 2-ton volume like the Dodd-Frank bill, but the release’s brevity leaves many river cards unturned. What’s missing?

The biggest concerns this time around include:

- Uncertainty around the extent of ECB involvement to leverage its balance sheet to bailout out/print money for any and all sovereign and banking “needs” across the region. Here Draghi has not shown his cards and Germany (Merkel and Co.) continues to fear-monger hyperinflation.

- How can, short of ECB involvement, the existing bailout facilities—the EFSF and the ESM that is “expected” to come online on 9 July (after German ratification today) with €600B upfront cash—cope with the default threats of Italy (sovereign and banking) and remaining Spanish sovereign imbalances? We view both facilities as being far too underfunded to cope.

- There was no concrete talk or agreement on a fiscal compact and fiscal union for the Eurozone-17 and/or EU-27. As a reminder, we believe a fiscal union must go hand in hand with a monetary union, if the Eurozone has any hope of maintaining its existing fabric.

- Because Europe needs a fiscal union before it can legitimately consider such programs as Eurobonds and a Pan-European deposit guarantee, we also didn’t get any further clarity on these two programs. Both could be very impactful for mitigating risk, however we remain firm that given the inability of states to willingly give up their full fiscal sovereignty to Brussels, such compromise, if it ever materializes, is many months if not years out.

So what were the key components of the proposal?

- Creating a single banking supervisor under the ECB

- Allowing the ESM to recapitalize banks directly

- Renouncing the preferred creditor status of loans to Spanish banks after they are transferred from the EFSF to ESM, and

- Flexible use of EFSF/ESM under a “Memorandum of Understanding” without Troika oversight

And what are the key undefined points and question marks?

- It’s not clear the scope of a “single supervisory”, which will not be in place, if it ever is, until a target of the end of 2012.

- The ESM “could” have the “possibility” (“following a regular decision”) to recapitalize banks directly with “appropriate conditionality”. Which means specifically?

- Question: What is the “appropriate conditionality” tied to banks who receive funds from the ESM?

- Question: Will the EFSF/ESM have the ability to buy bonds in the open market?

- Question: Will ESM loans no longer carry preferred creditor status, or only for certain countries?

- Merkel was out this morning saying each ESM bank recap will need unanimous approval (and another German official says the ESM seniority change is limited to Spain).

- Issue: For now the EFSF has to fund itself at the market, while there has been no indication from Germany that it is willing to soften its opposition to granting the ESM a banking license.

Returning to the title of this note, “Not in my Lifetime” (Nicht zu meinen Lebzeiten), which is the phrase Frau Merkel utter this week dismissing “euro bonds, euro bills and European deposit insurance with joint liability and much more” as “economically wrong and counterproductive,” saying that they ran against the German constitution.

Her positioning portends that Eurocrats will remain at loggerheads over Europe’s path forward. Europe is running out of bullets in our opinion to save the Eurozone project short of the ECB stepping in to play a larger role. However, we must return to our most basic outlook which is that excessive debt loads are one main problem across peripheral Europe. Growing debt only further impairs and slows growth, a point proven by history according to the seminal work of Reinhart and Rogoff.

Switching gears, it was a second straight week that saw peripheral yields and risk metrics (CDS) come in, while new peripheral sovereign paper was issues at significant premiums (vs pervious auctions as recent as last month), and data—including confidence figures and retail sales—slid to the downside! [See below in Data Dump].

EUR-USD:

Below is an updated EUR/USD price level chart. Our immediate term TRADE support is $1.24 and resistance is $1.26. Today’s Summit release sent the price through our $1.26 line. We’ll be monitoring this level closely to confirm or deny aninflection. Our intermediate term TREND support level remains at $1.23. Our call is that if $1.23 breaks, look out below! We’re not EUR parity folks because we see Eurocrats stepping in to prevent it.

Call Outs:

ECB - A Reuters poll found 48 out of 71 analysts expect the central bank to cut rates next week, most of them forecasting a 25 basis point cut to 0.75%. Benoit Coeure said last week cutting rates was an option and one that would be discussed at the ECB's 5 July meeting.

Italy - Italy’s business lobby sees GDP at -2.4% and -0.3% in 2012/2013 (down from -1.6% and +0.6%).

Spain - Rajoy “we can’t finance at current prices for too long” and “many institutions have no market access”.

UK - Barclays Plc was fined 290 million pounds, the largest penalties ever imposed by regulators in the US and UK, after admitting it submitted false London and euro interbank offered rates.

Germany - Egan Jones Downgraded Germany From AA- To A+.

France - France's government will increase the minimum wage by more than inflation this year for the first time since 2006, in the hope that stronger consumption will revive the country's ailing economy.

Spain - Moody’s downgraded 28 Spanish banks (12 cut to junk) citing the sovereign downgrade earlier this month as well as the possibility that commercial real estate losses will worsen.

EU - is losing around €1 trillion a year in tax evasion. The EU Commission is calling on the 27-nation bloc to improve tax collection nationally, boost cooperation between EU countries in fighting tax fraud and increase pressure on tax havens outside the EU to limit tax evasion. Draft proposals include making taxes simpler with the ability to deal with them online and that EU countries should have the same minimum penalties for tax evasion, so that fraudsters cannot choose less risky locations.

Slovenia - may ask for a bailout in July says PM Janez Jansa.

Greece - Greek Finance Minister Vassilis Rapanos resigned for health reasons.

Cyprus - becomes the 5th Eurozone nation to request EU aid, with initial figures projected at up to €10B.

Cyprus - Fitch Ratings cut Cyprus’s credit rating to junk status at BB+ from BBB- and maintained a negative outlook on the nation’s rating, citing expectations that Cypriot banks will need further, substantial capital injections. Fitch said that in addition to the €1.8B required to recapitalize Cyprus Popular Bank, the country’s banks could require as much as an additional €4B in additional capital — an amount equal to 23% of the tiny country’s GDP.

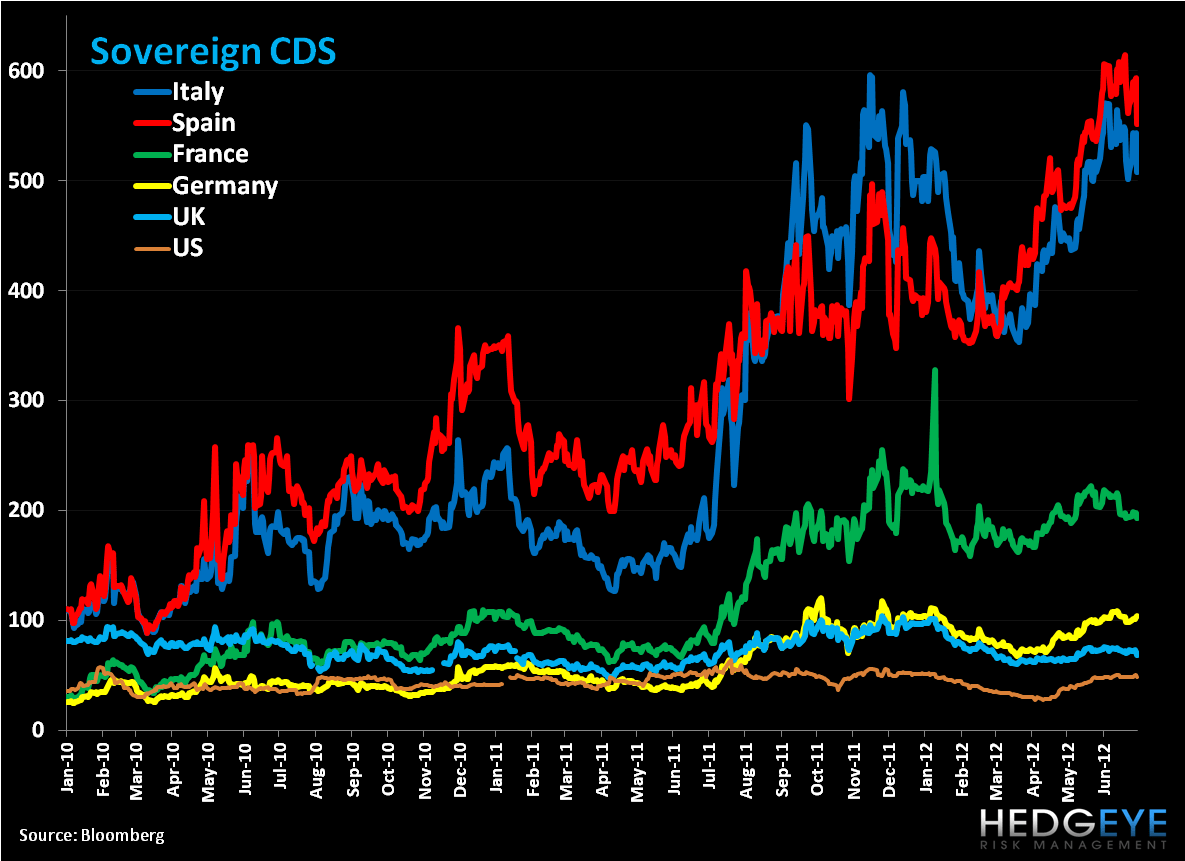

CDS Risk Monitor:

Sovereign CDS were down on the week. Ireland saw the largest decline in CDS w/w at -43bps to 582bps, followed by Portugal -39bps to 808bps, Spain -17bps to 552bps, and Italy -1bps to 508bps. Germany rose +5bps to 104bps.

Data Dump:

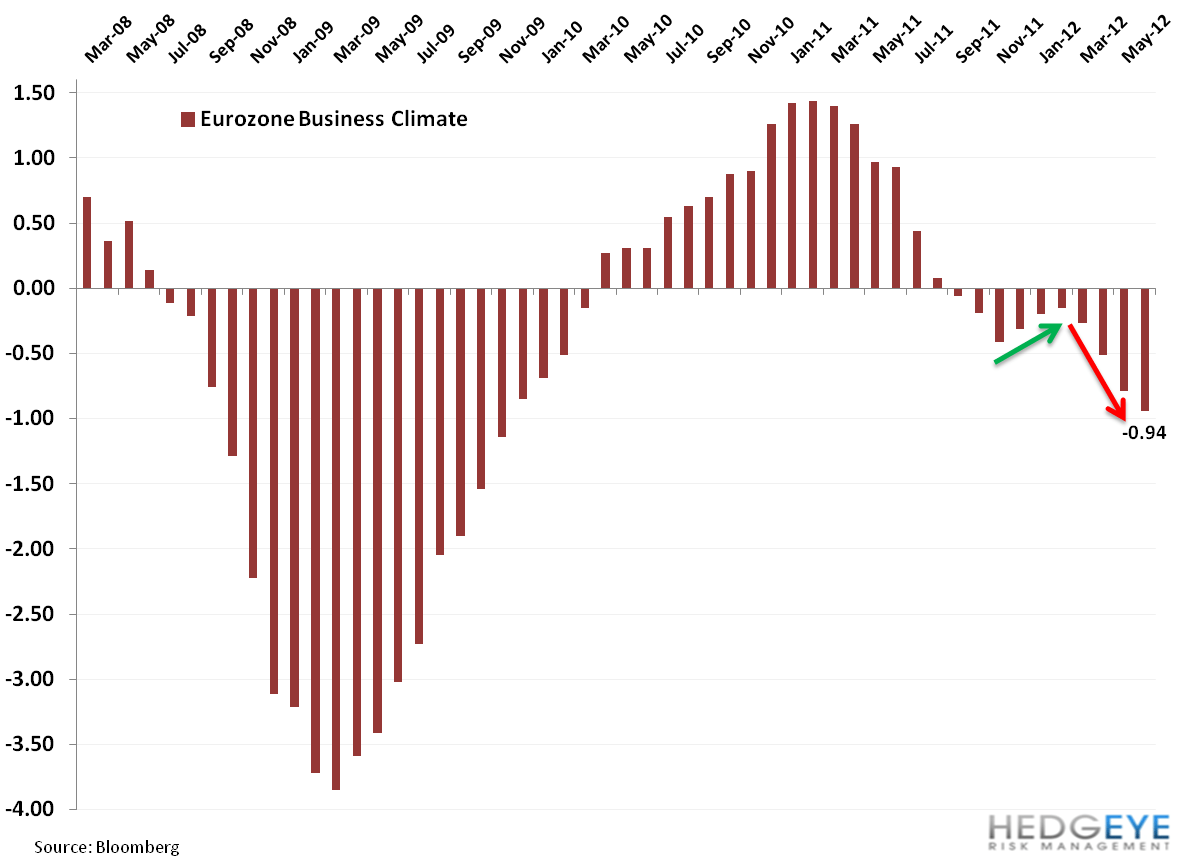

Eurozone Business Climate indicator -0.94 JUN vs -0.79 MAY

Eurozone Consumer Confidence -19.8 JUN Final vs -19.3 MAY

Eurozone Economic Confidence 89.9 JUN vs 90.5 MAY (lowest level since 2009)

Eurozone Industrial Confidence -12.7 JUN vs -11.4 MAY

Eurozone Services Confidence -7.4 JUN vs -5.2 MAY

Germany CPI 2.0% JUN Preliminary Y/Y (exp. 2.1%) vs 2.2% MAY [-0.2% JUN M/M (exp. -0.1%) vs -0.2% MAY]

Germany Unemployment Rate 6.8% JUN (exp. 6.7%) vs 6.8% MAY (revised up from 6.7%)

Germany Unemployment Change 7K JUN vs 1K MAY

Germany GfK Consumer Confidence 5.8 JUL vs 5.7 JUN

UK Q1 GDP Final UNCH -0.3% Q/Q

UK Q1 GDP Final revised to -0.2% Y/Y vs -0.1% previous estimate

UK Nationwide House Prices -1.5% JUN Y/Y (exp. -0.6%) vs -0.7% MAY [-0.6% JUN M/M (exp. 0.1%) vs 0.2% MAY]

France Consumer Confidence 90 JUN vs 90 MAY

Spain Total Housing Permits -32.4% APR vs -27.8% MAR

Spain CPI 1.8% JUN Prelim Y/Y vs 1.9% MAY

Spain Producer Prices 3.2% MAY Y/Y vs 3.0% APR

Spain Retail Sales -4.3% MAY Y/Y vs -11.5% APR

Italy Retail Sales -6.8% APR Y/Y vs 1.5% MAR

Italy Business Confidence 88.9 JUN vs 86.6 MAY

Italy CPI 3.6% JUN Prelim Y/Y vs 3.5% MAY

Italy PPI 2.3% MAY Y/Y vs 2.5% APR

Sweden PPI 0.3% MAY Y/Y vs 0.0% APR

Sweden Retail Sales 4.6% MAY Y/Y (exp. 3.8%) vs 0.5% APR

Norway Unemployment Rate 3% APR vs 3% MAR

Finland Consumer Confidence 5.8 JUN vs 12.0 MAY

Finland Business Confidence -6 JUN vs -9 MAY

Finland Unemployment Rate 9.5% MAY vs 8.4% APR

Switzerland UBS Consumption Indicator 1.05 MAY vs 1.37 APR

Ireland Retail Sales -2.1% MAY Y/Y vs -1.8% APR

Ireland Property Prices -15.3% MAY Y/Y vs -16.4% APR

Ireland PPI 2.0% MAY Y/Y vs 2.8% APR

Portugal Consumer Confidence -51.5 JUN vs -52.6 MAY

Portugal Economic Climate Indicator -4.4 JUN vs -4.6 MAY

Hungary Unemployment Rate 11.2% MAY vs 11.5%

Slovakia PPI 4.2% MAY Y/Y vs 3.8% APR

Slovakia Consumer Confidence -22.6 JUN vs -22.5 MAY

Slovakia Industrial Confidence 2 JUN vs 2.7 MAY

Netherland Q1 GDP Final -0.8% Y/Y vs -0.8% in Q4 [+0.3% Q/Q vs -0.6% in Q4]

Netherlands Producer Confidence -4.8 JUN vs -5.0 MAY

Czech Republic Business Confidence 4.6 JUN vs 6.0 MAY

Czech Republic Consumer and Business Confidence -2.2 JUN vs -1.4 MAY

Czech Republic Consumer Confidence -29.3 JUN vs -31.0 MAY

Turkey Foreign Tourist Arrivals -1.5% MAY Y/Y vs -5.3% APR

Interest Rate Decisions:

(6/26) Hungary Base Rate UNCH at 7.00%

(6/27) Romania Interest Rate UNCH at 5.25%

(6/28) Czech Repo Rate Announcement CUT to 0.50% vs 0.75%

The Week Ahead:

Sunday: The ESM is set to come into force

Monday: Eurozone Troika will likely start on its mission to Cyprus; Jun. Eurozone, Germany, and France PMI Manufacturing - Final; May Eurozone Unemployment Rate; Jun. UK Lloyds Business Barometer, PMI Manufacturing; Jun. Italy PMI Manufacturing; May Italy Unemployment Rate – Preliminary, New Car Registration, Budget Balance; Spain and Italy Manufacturing PMI

Tuesday: May Eurozone PPI; Jun. UK PMI Construction, BRC Shop Price Index; May UK Net Consumer Credit, Net Lending Sec. on Dwellings, Mortgage Approvals, Money Supply: Jun. Spain Unemployment

Wednesday: Jun. Eurozone PMI Composite and Services - Final; May Eurozone Retail Sales; Jun. Germany PMI Services – Final; Jun. UK PMI Services, Official Reserves; 1Q UK BoE Housing Equity Withdrawal; France Prime Minister Ayrault is poised to submit new adjusted budget to his cabinet; Jun. France PMI Services – Final; Spain Services PMI; Jun. Italy PMI Services; 1Q Italy Deficit to GDP; Sweden Riksbank Interest Rate

Thursday: Eurozone ECB Announces Interest Rates; May Germany Factory Orders; UK BoE Announces Rates; Jul. UK BoE Asset Purchase Target; Jun. UK New Car Registration

Friday: May Germany Industrial Production; Jun. UK PPI Input and Output; May France Central Government Balance, Trade Balance; May Spain Industrial Output

Extended Calendar Call-Outs:

JULY: France – extraordinary session of parliament in July is due to re-draft the 2013 budget

9 July: ESM to come into force

5 July: ECB governing council meeting

19 July: ECB governing council meeting

18-19 October: Summit of EU Leaders

Matthew Hedrick

Senior Analyst