This note was originally published at 8am on June 12, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Fear is a potent weapon in the hands of the power elite.”

-Chris Hedges

That’s an important quote in Death of The Liberal Class by Chris Hedges. If you believe, like I do, that risk management starts and ends with being empathetic to all politically polarized positions, I highly recommend this book. The first 50 pages will really make you think.

Imagine that, thinking for yourself within the context of how other people think. Instead of doing more of the same – more of what has not worked (print, bail, print), imagine a world where we aren’t centrally planned by Republican/Democrat economic policy dogma. Imagine a world where America wasn’t inching toward becoming Japanese European.

The power elite may have landlocked how Bernanke’s Fed and Geithner’s Treasury think about letting losers win, but they have not yet suffocated the rest of us free market capitalists into silence. Yesterday’s market reaction to the latest bailout scheme was a stiff reminder of that. For them.

Back to the Global Macro Grind…

If you saw my market debate with the ING strategist on The Kudlow Report last night, you can see that I am pretty much #Fedup. I am tired of incompetent forecasting on both US and Global growth. I am done with letting these guys from the Old Wall change their perma-bull thesis to new ones every time they get the prior one wrong.

Done.

I think The People are done with it too. That’s why you see these outflows from stock and commodity funds. That’s why you see this American Zeitgeist of distrust in any idea that comes out of the Fed, Treasury, or IMF. That’s why you saw pretty near every pundit who was spewing about how high the market was going to go on yesterday’s bailout “news” get run right over.

“Fear is a potent weapon.” And our being right on Growth Slowing is not the fear I am talking about. That’s called being accurate. Fear is what both the Bush and Obama administrations run on. So did Nixon and Carter. Fear of Big Government Interventions and all their conflicts of political interest are what puts a confident and optimistic guy like me on hiring hold.

The Fed has a “full employment” mandate, so they think doing more of what has not worked is their job. To a degree, that’s their own problem – the inability to re-learn, re-work, re-think. But, from a bigger picture perspective, this is really a leadership problem. The Fed and Treasury take their policy making lead from the President of The United States.

Here’s what one of their chief group-thinkers (Chicago Fed Head, Charles Evans) had to say after yesterday’s market reaction:

“I’ve been in favor of pretty much any accommodative policy I’ve heard about.”

Great. Just really great, Chuck. You have got to be kidding me. If Obama created a tax shelter whereby I could hire you for free, I’d probably go for it just so that I could fire you. You and your cronies from Chicago who want Policies To Inflate commodity prices need a real life wake-up call.

I’m certainly not alone in feeling this way. And since I built this company with my own risk capital, I’ll write whatever I want. Chapter 1 of Death of The Liberal Class is called “Resistance.” That’s what I am doing. I have American kids, and I resist the institutional pressure to put short-term politics and stock/commodity market performance ahead of the long-term future of this country.

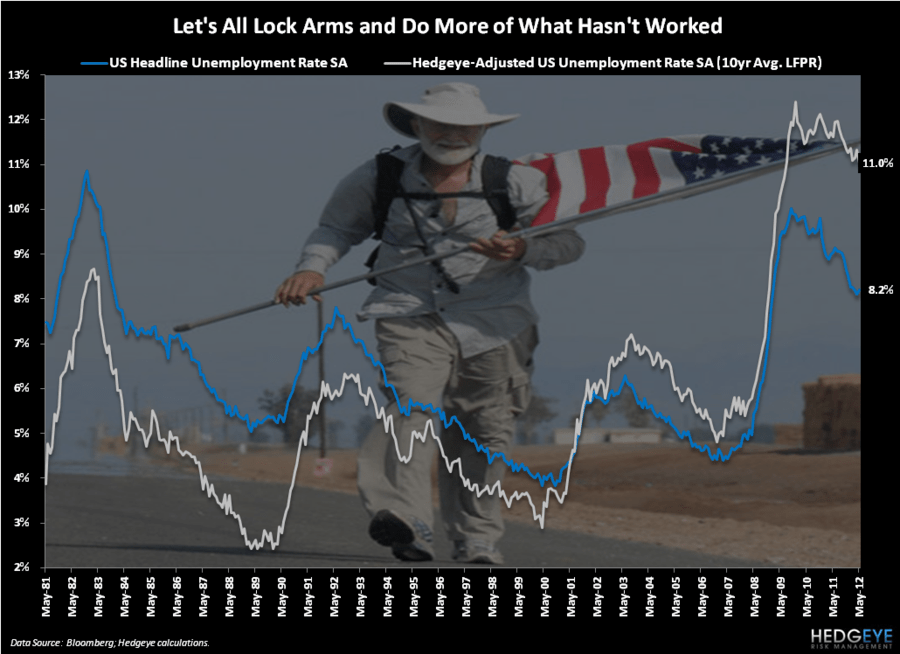

“Earnest Logan Bell, an unemployed twenty-five year old Marine Corps veteran, walks alone Route 12 in Update New York. A large American flag is strapped to the side of his green backpack… he is on a six-day, ninety mile self-styled “Liberty Walk” from Binghamton to Utica. He plans to mount a quixotic campaign…” (Death of The Liberal Class)

“Anger and a sense of betrayal: these are what Ernest Logan Bell and tens of millions of other disenfranchised workers express…” (page 6). If you don’t get that, you are completely out of touch with the real world in which central planners are forcing us to live.

So go ahead, get the US taxpayer to start back-stopping European and Japanese government losses through the IMF. Tim Geithner, I personally dare you to do that and explain it, as you like to say “deeply”, to the American people. Explain to us, with all your fear-mongerings, why we should trust you this time.

Sadly, for Bernanke and Geithner, this time is not different. The market gets that too.

In other Keynesian central planning news this morning:

- The IMF says the Japanese Yen is “overvalued” and that the Japanese should “stimulate”

- Italy’s Monti (who forecasted the European Sovereign Debt Crisis as “ending” in March) to meet with France’s Hollande

- India’s debt to likely lose “investment grade status” (whatever that still means)

Great. Just great. The Washington, DC based (and US tax payer backed) IMF now has market opinions on “valuation”, and Geithner is pushing Lagarde to pull a Krugman on Japan and Europe (1997 he told the Japanese to “PRINT LOTS OF MONEY”).

Great. (link to the CNBC debate https://app.hedgeye.com/media/502)

So was my 0% US Equity asset allocation yesterday. My unlevered and un-invested position Cash can be a Potent Weapon too.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Spain’s IBEX, Italy’s MIB, and the SP500 are now $1588-1598, $96.59-99.98, $82.01-83.17, $1.24-1.26, 5937-6667, 12238-13661, and 1284-1326, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer