This note was originally published at 8am on June 05, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The fact that this policy had failed spectacularly in 1973 did not deter the weak dollar crowd.”

-Jim Rickards

Between today’s G-7 meeting, tomorrow’s ECB decision, and Thursday’s Bernanke testimony, there will be plenty of opportunity for politicians and their pandering economists to beg and fear-monger for more of what simply has not worked.

That’s the short-run. The conflicted and compromised will do whatever it takes for their short-term political survival. In the long-run, apparently Keynes had the duration of the policy trade wrong – the rest of us aren’t all yet dead.

Taking a step back, the last 60 years of history are obviously littered with examples from Charles de Gaulle to Richard Nixon where sovereign currency devaluation and debt monetization did not work. If you’d like to get back up to speed on that, Jim Rickards does a great job walking through part of this history in Chapter 5 of Currency Wars (1967-1987).

Back to the Global Macro Grind…

Real-time market prices don’t lie; politicians do. Within hours of last week’s US Growth Slowing double-header (US GDP slowed to 1.9% in Q1 versus 3% in Q4, then the May Employment Report bomb detonated), the US Dollar stopped going up.

Why? Because the rest of the world fully expects an un-elected central planner in Washington (Ben Bernanke) to launch an iQe4 Upgrade. He did it on January 25th (pushing 0% rates out to 2014) and there’s no reason to expect he doesn’t do something again between Thursday’s Joint Economic Committee meeting and the FOMC meeting on June 20th. He’s fighting for his political life.

All that said, we have no idea what he is going to do. So don’t look for us to give you the super-secret whisper on that. Our strategy remains playing the game that’s in front of us, Embracing Uncertainty. We think the US Election puts him in a box.

Right, the man walked on water during 2008 and we should perpetually give him thanks and praise. But seriously, what Bernanke should have done and what he did have been 2 very different things since 2010.

By the summer of 2010 Bernanke had bi-partisan support (the Republicans wanted to win the mid-term elections) to move to Quantitative Easing (Policy To Inflate). Both parties wanted the stock market up. Now only one of them do.

What Bernanke does next must also be contextualized on a relative basis. This is not 2008 or 2010 in that regard either. Today you have a currency war between the 3 major currencies of the world (Dollar, Euro, and Yen). They trade relative to the expedience of the latest Fiat Fool (failed) Policy that is designed to debauch them. The Fed, ECB, and BOJ don’t get paid to act unilaterally.

So what are currency markets signaling happens next?

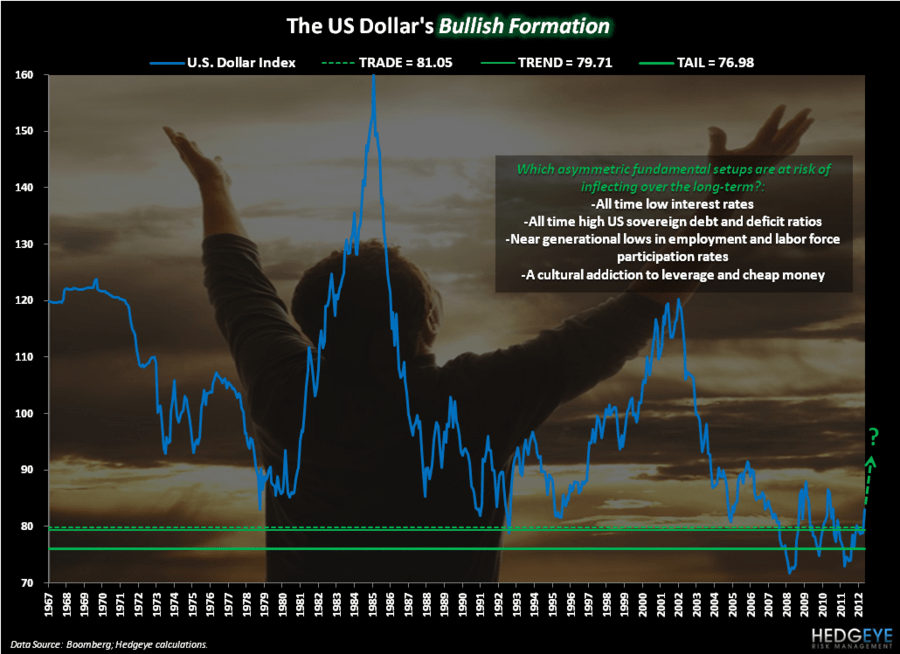

1. The US Dollar – remains in what we call a Bullish Formation (bullish across all 3 of our risk management durations, TRADE/TREND/TAIL) with immediate-term TRADE support at $81.55 and next resistance = $83.31.

2. The Euro (vs USD) – remains in what we call a Bearish Formation (bearish across all 3 of our durations) with an immediate-term TRADE support/resistance range of $1.22-1.25.

3. The Yen (vs USD) – is in a neutral position with long-term TAIL resistance at $77.68 and immediate-term TRADE support at $79.05.

In other words, if we had to pick one and #TimeStamp our highest probability scenario right now (we do), we’d be long the US Dollar and short the Euro (which we re-shorted on yesterday’s bounce).

It’s another way of saying that both Hedgeye and Global Macro markets think that the Europeans are in a much more dire situation (for now) than the United States of America is.

That could change at literally any minute of any day now – and that, of course, is why most sane people don’t trust these markets or the politicians attempting to centrally plan them.

Back to the ‘for now’…

We still aren’t all brain dead, and we have to deal with whatever tomorrow’s European move to debauch the Euro back down to $1.22 brings. Then we have to react to Bernanke’s reaction to the reaction. Then we all have to pray.

Prayer, in markets, is obviously not a risk management process. Neither is hope. That said, my only long-term hope for this country and the free-market economy that we used to have is to get Ben Bernanke out of the way of expectations, let prices at the pump clear, and let US Consumption Growth recover again.

With Bernanke having not been able to really do anything for the last 5-6 weeks, the US Dollar has risen steadily and Oil, Gold, Copper, etc. prices have fallen precipitously. That’s good for American consumers.

That’s bad if you are long Energy stocks (the Energy ETF (XLE) is down -10.3% for the YTD). That’s good if you are short them and long Consumer Discretionary stocks (the Consumer ETF (XLY) is +7.4% for the YTD).

Strong Dollar = Strong America (via Stronger Consumption). That’s not more of a 1973 like Failed Policy. That’s a new idea.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1599-1625, $97.21-102.78, $1.22-1.25, and 1258-1283, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer