TODAY’S S&P 500 SET-UP – June 15, 2012

As we look at today’s set up for the S&P 500, the range is 34 points or -1.44% downside to 1310 and 1.12% upside to 1344.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/14 NYSE 1229

- Up from the prior day’s trading of -1219

- VOLUME: on 6/14 NYSE 779.39

- Increase versus prior day’s trading of 10.22%

- VIX: as of 6/14 was at 21.68

- Decrease versus most recent day’s trading of -10.67%

- Year-to-date decrease of -7.35%

- SPX PUT/CALL RATIO: as of 6/14 closed at 1.23

- Down from the day prior at 2.08

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 37

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.61

- Decrease from prior day’s trading at 1.64

- YIELD CURVE: as of this morning 1.32

- Down from prior day’s trading at 1.35

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Empire Manufacturing, June, est. 13 (prior 17.09)

- 9am: Total Net TIC flows, April, no est. (prior -$49.9b)

- 9am: Net Long-Term TIC Flows, April, est. $45b (prior $36.2b)

- 9:15am: Industrial Production, May, est. 0.1% (prior 1.1%)

- 9:15am: Capacity Utilization, May, est. 79.2% (prior 79.2%)

- 9:15am: Manufacturing Production, May, est. -0.1% (prior 0.6%)

- 9:55am: University of Michigan Confidence, June, est. 77.5 (prior 79.3)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- President Obama travels to Chicago

- Mitt Romney begins bus tour in New Hampshire

- EPA, following court order, expected to announce proposal for new rule on soot pollution

- House meets in pro forma session; Senate in session

- Senate Finance meets on tax reform, energy policy, 10am

- FERC, NRC meet on nuclear power, cybersecurity, station blackout rulemaking and power-grid reliability, 9:30am

WHAT TO WATCH:

- EU Leaders to call for “further urgent measures” to aid growth

- Yammer agrees to be bought by Microsoft for >$1b: WSJ

- Hong Kong Exchanges agrees to buy LME for $2.2b

- Russell Indexes posts updates to list of additions/deletions for reconstitution

- U.S. industrial production probably cooled in May

- Safeway to hold call today on financial strategy

- Greek Election, G-20 Summit, Fed Meeting: Week Ahead June 16-23

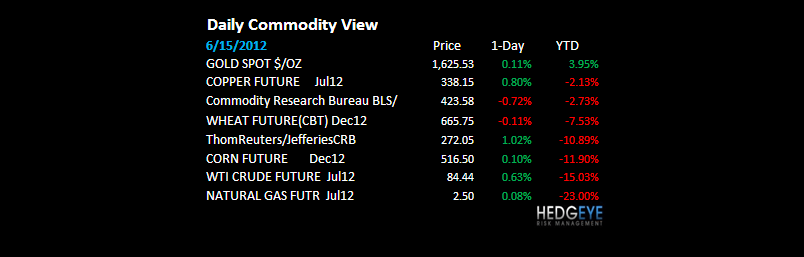

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COMMODITIES – thank God we covered all our shorts there ahead of proactively predictable central planning behavior; rallies in Oil, Gold, Copper look like those in European Equities, right to the walls of immediate-term TRADE resistance as the USD moves to immediate-term TRADE oversold at $81.83; very dangerous spot for Correlation Risk to come back on in a hurry.

- Gold Traders Bullish as Hedge Funds Increase Wagers: Commodities

- HKEx to Buy LME for $2.15 Billion in First Commodity Venture

- Copper Set for First Weekly Gain in Seven on Stimulus Outlook

- Oil Gains a Second Day on Stimulus Speculation, OPEC Output Call

- Gold Set for Best Run Since August on Stimulus Bet, Greece Vote

- Soybeans Rise on Demand Gain From U.S. Processors and Importers

- Cocoa at a Four-Month High as Ivory Coast Supply May Be Limited

- Malaysia Rejects Bid to Cancel Lynas Rare-Earth Refining Permit

- China Said to Buy 1 Million Tons of U.S. Cotton for Reserves

- Bernanke’s Inflation Validated as Commodities Retreat With Hawks

- Petrobras Worst Big Oil Bet on Deepwater Disappointments: Energy

- Iron Ore to Slump as China Slows, Eurofer Says: Chart of the Day

- Oil Rout Has China Hoarding Most Since Olympics: Energy Markets

- Hedge Funds Increase Wagers on Gold Rally

- OPEC Decision Puts Onus on Saudi Arabian Cuts If Prices Fall

CURRENCIES

EUROPEAN MARKETS

EUROPE – now that the central planning “smoothing” mechanism has backstopped markets for another 12 hrs of trading, pretty much every single European squeeze index (Spain, Italy, Greece, etc.) has rallied right back to a wall of immediate-term TRADE resistance, and so has the Euro at 1.26; into the “event” we are at the end of the runway; not good.

ASIAN MARKETS

ASIA – interestingly, but maybe not surprisingly, Japan didn’t go up on that “news” – what will be left over for them after Geithner, the IMF, and Europe blows whatever bullets they have left on Greece/Spain/Italy? Rest of Asia was eerily mixed (China +0.5%, KOSPI -0.7%).

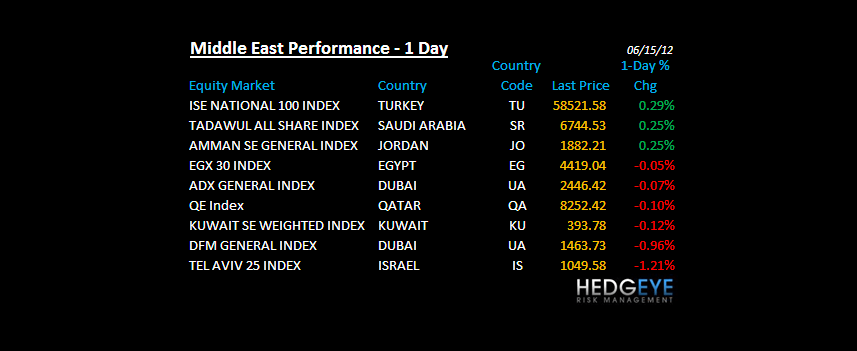

MIDDLE EAST

The Hedgeye Macro Team