Despite the dollar trading down over the last week, many of the commodities we monitor continue to decline in price as economic concerns impact demand expectations. Softer top line trends due to economic weakness are obviously a negative for restaurants but when those softer top line trends are accompanied by all-time high cost of sales growth, the impact on the bottom line can exceed expectations.

General Overview

Clearly, “Softer top line trends and all-time high cost of sales growth” was referring to Buffalo Wild Wings. Estimates are holding firm here, for 2012, even as wing prices are up 133% year-over-year. Beef costs were down over the last week as demand concerns continue to weigh on prices. Supply dynamics remain bullish for prices, but our view is that supply data points highlighting the shrinking herd size in the U.S. have been known for some time. Coffee costs continue to come down which is a positive for SBUX, PEET, GMCR, and other coffee companies. In line with the Hedgeye Macro team’s stance, for a broad overview of where commodity costs are going in our space, we pay particular attention to the US Dollar. As Keith likes to say, “get the US Dollar right, and you’ll get a lot of other things right”, and anchoring off our Macro team’s work on the dollar has helped us to better understand the commodity complex for the restaurant space. Per the second chart, below, the inverse correlation between the dollar the CRB foodstuffs Index is quite strong at -0.81 over the past nine months.

Gasoline Prices

For the week ended June 8th, gasoline demand in the U.S. fell 0.5% to a five week low despite prices at the pump falling lower. Fuel use over the four weeks prior to June 8th fell 1.9% below the same period in 2011, a record 64th consecutive drop in that measure.

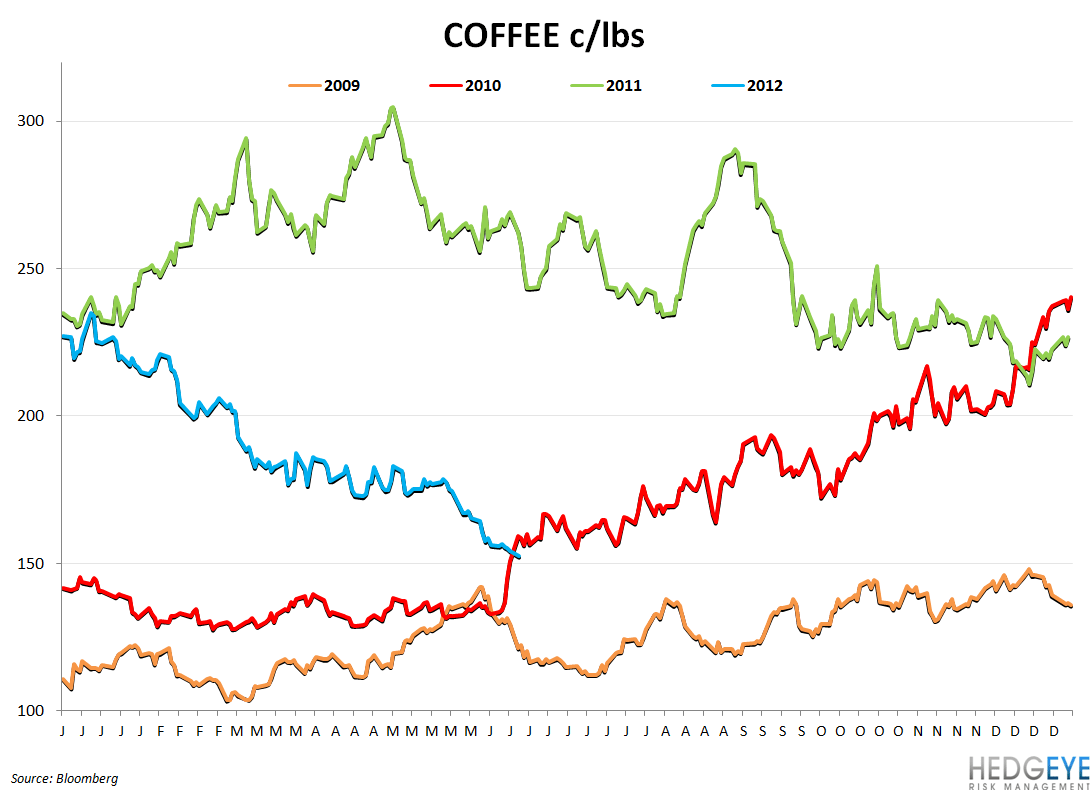

Coffee

Coffee costs lead to the downside over the past week. Here is a refresh on the most recent commentary, by company, on coffee costs.

SBUX: With the commodity markets today and again this is primarily dominated for us by coffee, it is clear that we have a tailwind coming certainly in fiscal 2013 as we've locked most of those prices in for coffee through 11 months of our coffee needs in our fiscal 2013 and directionally we expect tailwinds again in 2014, now we've not locked much of our coffee prices for 2014. We have done some buying for 2014 already, but directionally everything looks like we will face certainly 12 months and I expect 24 months or longer of now – of more favorable commodity cost environment.

HEDGEYE: This coffee tailwind should mitigate some of the dilution to EPS that is expected as a result of recent acquisitions. However, FY12 and FY13 costs being largely locked and given that the company bought all the way down from the peak in coffee costs just over a year ago, the tailwind starting in FY13 should be modest.

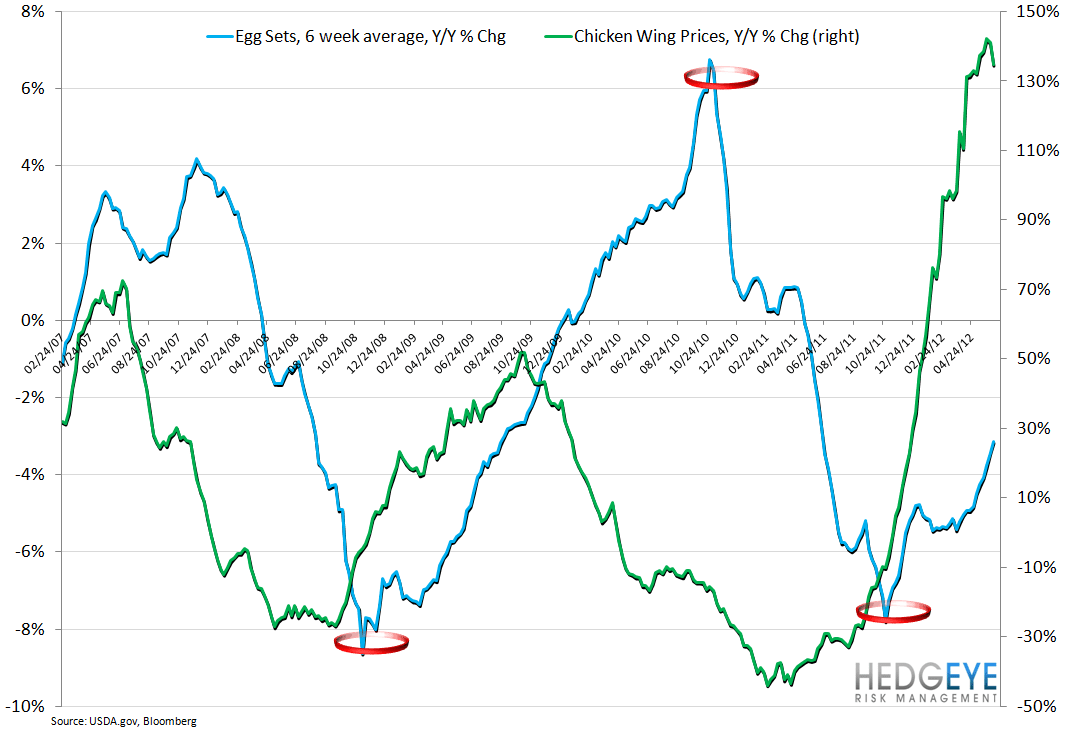

Chicken Wings

BWLD [from the most recent 10-K]: “A 10% increase in the chicken wing costs for 2011 would have increased restaurant cost of sales by approximately $3.8 million.”

HEDGEYE: We estimate that a 10% increase in chicken wing prices would account for $0.14 of EPS pressure. 1Q inflation was 57%. If we assume 120% inflation for 2Q and a possibly-conservative 70% for the year overall, that would imply $0.95 of FY12 EPS pressure. We do not think that the Street's estimates have been adjusted accordingly.

Correlation Table

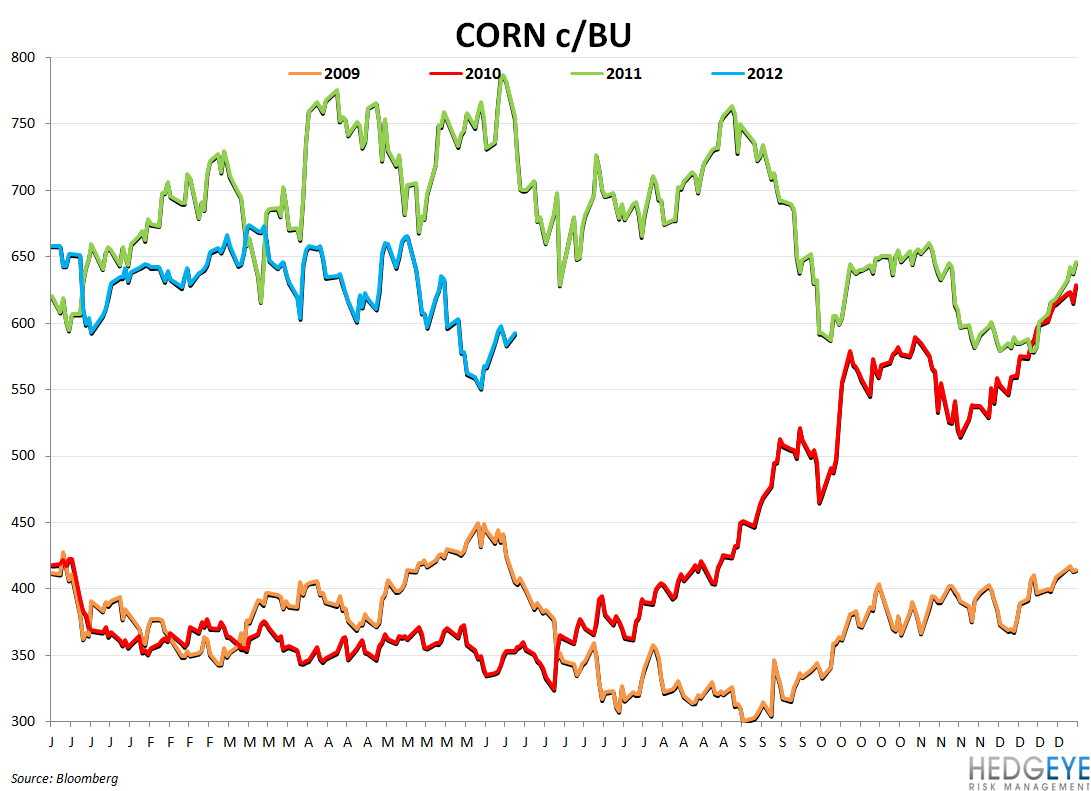

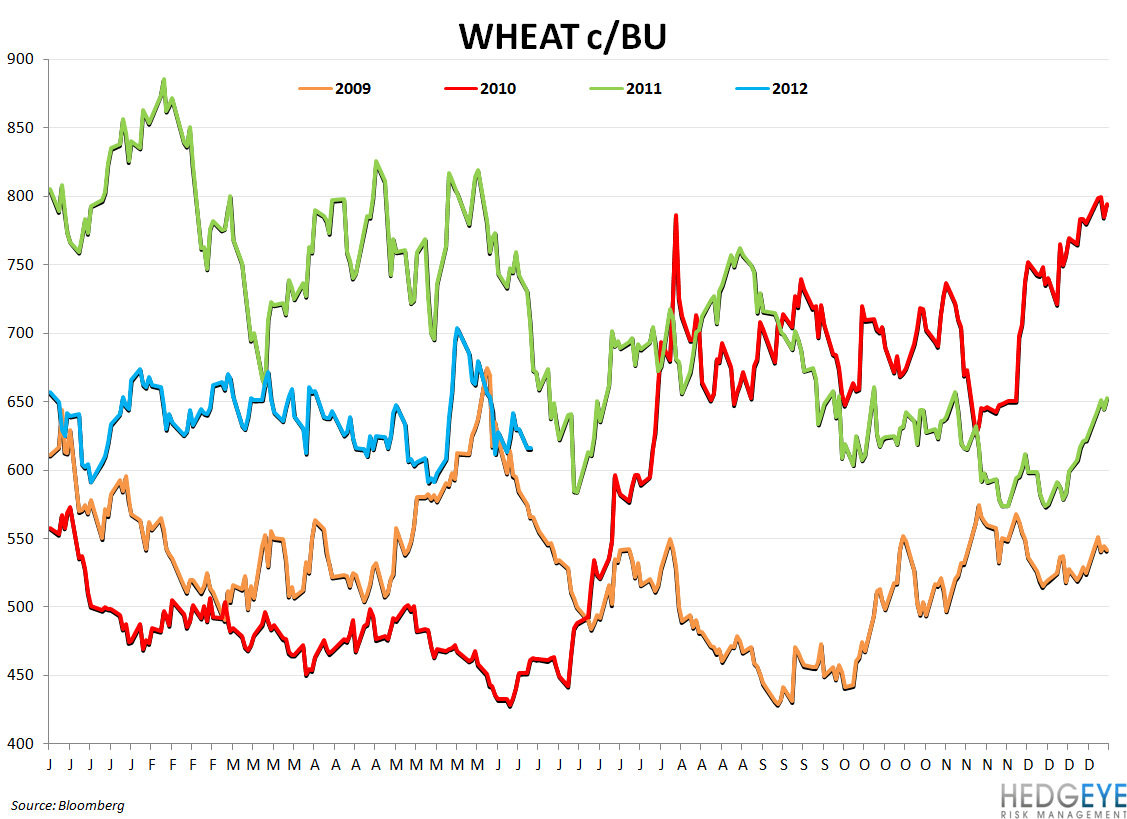

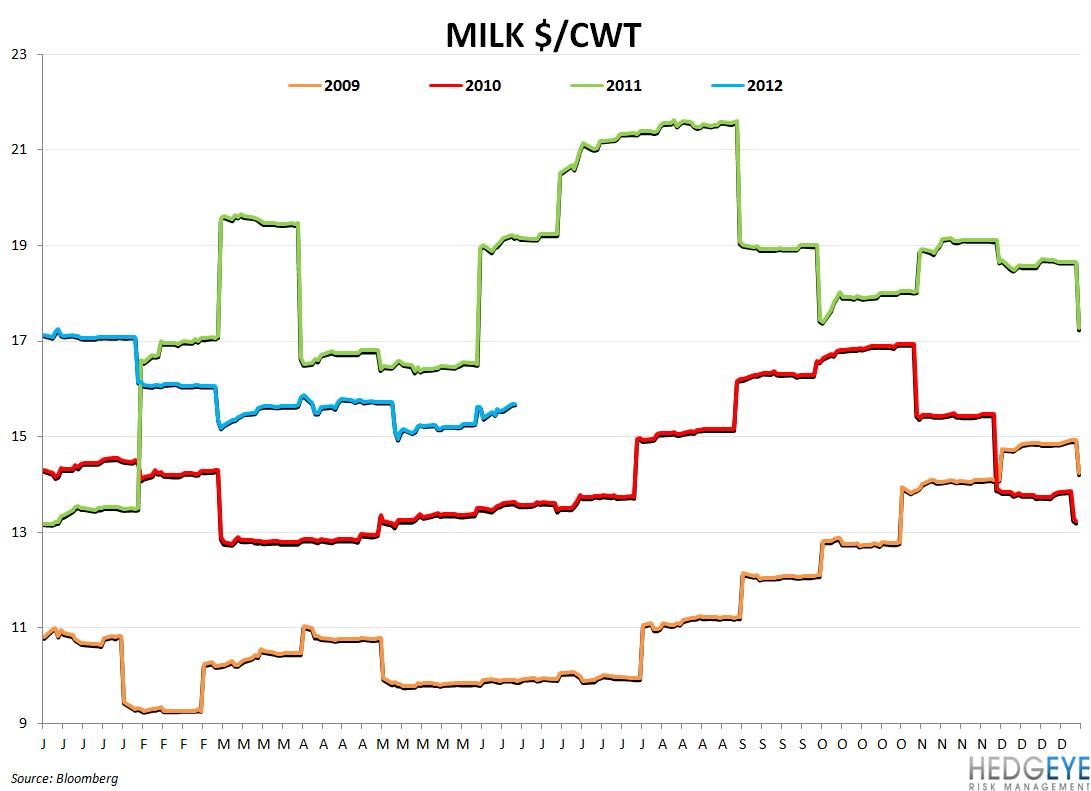

Charts

Howard Penney

Managing Director

Rory Green

Analyst