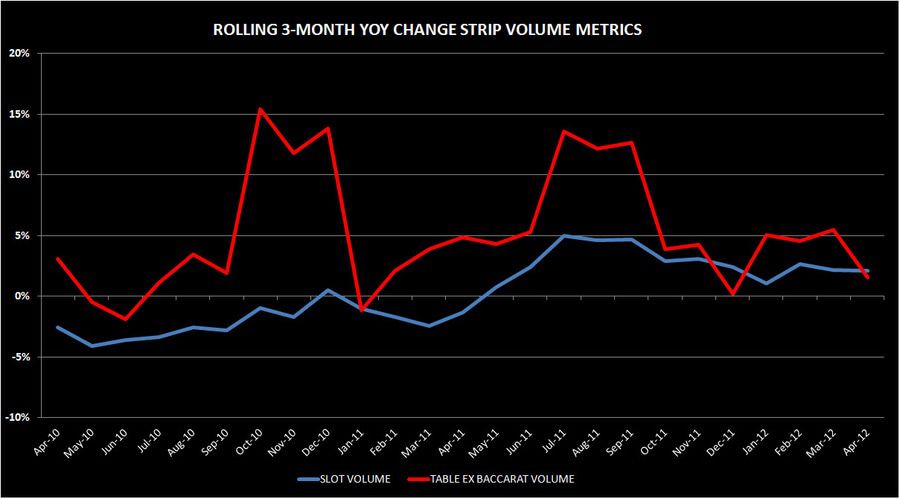

- Given the free fall of 2008-2009, these core metrics should be recovering faster

- Table volume is making lower highs and slots have been consistently in the “slow growth” camp

- “Return to peak EBITDA” analysis is a pipe dream. Structurally, LV and most of domestic gaming appear permanently impaired.