Over our TAIL duration, LULU is arguably one of the cheapest stocks in retail. Unfortunately, stocks don’t trade on a 3-year duration. Those looking at near-term metrics see it as the most expensive. That = opportunity. Be Patient.

It’s hard to justify that a company that is comping 25% and growing top line at 53% should trade off when it beats the quarter and guides up (albeit slightly) on the year. But welcome to the world of high-expectations stocks. Even though margins were better than guided, the fact is that they were down, delevering into ONLY 47% EPS growth (you should read that with an element of intended sarcasm).

People who shorted this name at 30x earnings earlier this year got steamrolled because the reality is that it’s rare to find such a powerful brand with such Blue Sky growth (though we think UA gives it a run for its money and is cheaper). If it’s at 30x, why not 40x? 50x? Clearly this is not the right metric. What’s the right metric? From a TAIL perspective (our duration spanning 3-yeasr or less) we like EV/market opportunity.

This is easier said than calculated. If you look at LULU’s share of the Yoga market as it stands today, it is going to look expensive on every metric imaginable, and it will appear by all means a short. You have to believe that the company can grow the category, and take the brand into areas that we do not know exist yet. That’s where the biggest money has been made in retail – when brands consistently do things that you never conceived as being possible.

In looking at LULU’s REAL market, we need to look at total high end sports apparel. The US Athletic Apparel Market is about $40bn at retail. Even Nike has only 10% share of that market. It’s massively fragmented. If we isolate to price points above $50 – which is pretty much where LULU lives, then we’re still looking at a $13bn market. Outside of the US, we think that the size is closer to 1.5x the US. So let’s say $30bn in aggregate.

Is LULU’s EV/Sales of 8.8x seemingly colossal? Yes. It’s a notch above KORS’ (unjustified) 8.5x, Chipotle’s 5.2x, UA’s 3.3x, NKE’s 1.9x and RL’s 1.8x. But relative to addressable market size, it’s trading at 0.33x vs NKE at 0.60x, and RL at 0.45. The only name cheaper than LULU is UA, which is sitting at 0.15x. You probably only care about this if you’re looking to really invest in the company as opposed to renting the stock. And this valuation certainly won’t prevent LULU from selling off as guidance is messy and the chart jockeys out there start eyeing the $61.33 200-day moving average (not our process…by the way). But the bigger picture view as to the premise that valuing LULU differently is definitely context worth considering.

Of course, ‘addressable market size’ is only important if a company has the team, vision, plan, capital, and allocation process to hit its goals. On our durations…

- TAIL (3-Years or Less): There was nothing we heard on today’s call that changes our view that LULU does, in fact, have what it takes to take disproportionate share of the addressable market.

- TREND (3-Quarters or Less): While we really like the company’s focus on innovation to lead demand instead of meeting it, the simple fact that they are not doing this already deserves a minor in the penalty box. Capped top line growth this year as LULU shifts its model won’t help its growth multiple near-term, nor will reinvesting better yy product cost deltas into innovation and material. These moves are for all the right reasons, but the market likely won’t care. The saving grace is that LULU’s SIGMA move this quarter was definitely positive, which offers up some Gross Margin support next quarter.

- TRADE (3-Weeks or Less): The quarter is already out of the bag, so near-term factors are minimal. With growth acceleration and margin improvement on hiatus, our sense is that – as great a growth story as it is -- chasing it here is premature.

LULU: Sales Inventory Gross Margin Analysis (SIGMA)

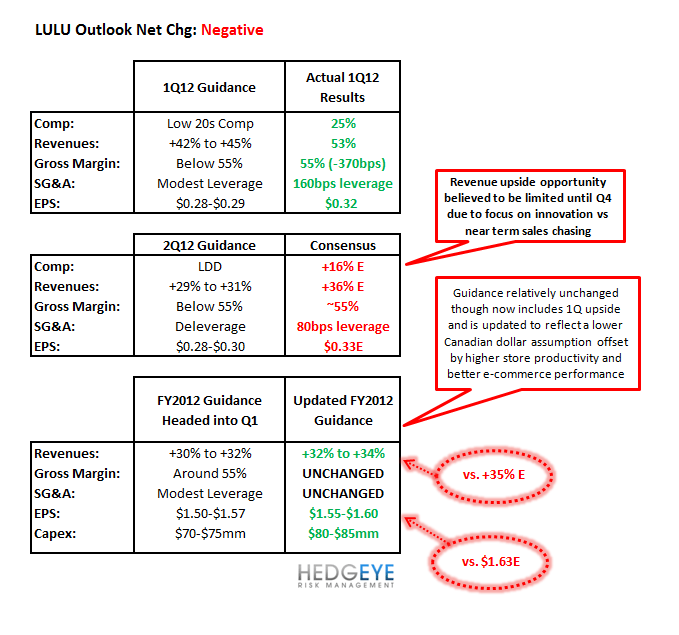

Accountability and Outlook: Here’s a look at LULU’s variance between guidance and actual, as well as deltas in guidance for the balance of the year:

Highlights from the Call:

Product Innovations vs. Chasing Near Term Sales:

- Shift in Thinking relative to last year- focused on avoiding buying in bulk to simply meet demand

- There is a brand cost associated with over ordering what people want today vs. focusing on what they will NEED down the road – near term focus results in markdowns

- Revenue upside will be limited as a result until Q4 with more modest comps mid-year (guided Q2 +LDD vs. +16E)

- Product innovation includes capsules (completed swim and commuter and planning new warm-wear, gym, cross-fit) as well as fabric infusions and technical investments

E-Commerce:

- +178% in 1Q12 reaching ~13% of sales vs. 7% in 1Q11

- Growth largely due to boost from transition to ATG platform last year

- Increases expect to be somewhat muted for the rest of the year with slightly lower penetration vs. Q1 in Q2/3 but will pop in Q4

- Seeing similar life span for products online and in store- not in the business of doing exclusives online

- Men’s penetration much lower online vs in store (overall 12% of sales in Q1)

- Expected to be accretive to long term GM target of 55% as penetration grows

Cost/Pricing:

- 85%-90% of the 25% Q1 comp due to increase in units with only a minor boost from pricing

- Cost improvements (primarily due to raw materials vs. labor) expected to be offset by investments in innovation

- Pricing product introductions to market but seeing improved margins on product as they are improved/innovated

- Seeing a better balance of full priced selling with more normalized markdowns driven by better inventory balance

International:

- Just launched E-commerce site in Australia (May); planning country specific launch in UK and Hong Kong later this year

- Canadian comps running MDD while US stores comping mid 30s (aggregate +25% comp)

- Brand recognition in New Zealand/Australia ~3 years behind the US but stores on track & comping well

- Yoga market continues to grow in Asia

- See both Europe and Asia attractive though Asia is more compelling

Full Year Guidance:

- Guidance updated to reflect Q1 outperformance through relatively unchanged- weaker Canadian dollar expected to be offset by strong store productivity & e-commerce

- Revenue upside limited until Q4 due to restrained sales chasing near term and focus on innovation

- Gross Margin expectations maintained around goal of 55% (-188 bps) due to higher product costs partially offset by more normalized markdowns from balanced inventory levels as well as occupancy leverage