TODAY’S S&P 500 SET-UP – May 23, 2012

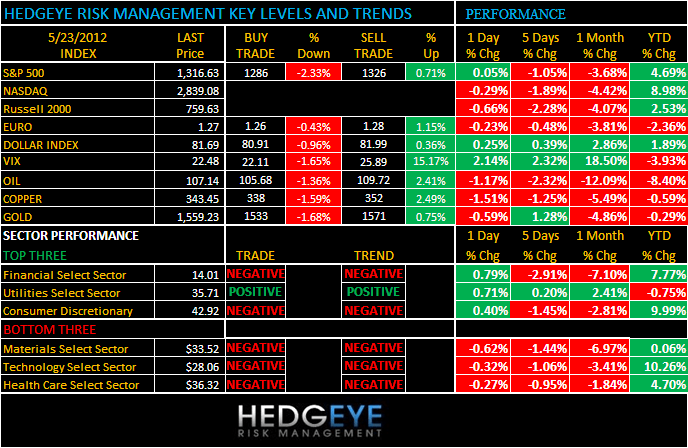

As we look at today’s set up for the S&P 500, the range is 40 points or -2.33% downside to 1286 and 0.71% upside to 1326.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 5/22 NYSE 104

- Down from the prior day’s trading of 2143

- VOLUME: on 5/22 NYSE 846.67

- Increase versus prior day’s trading of 6.09%

- VIX: as of 5/22 was at 22.48

- Increase versus most recent day’s trading of 2.14%

- Year-to-date decrease of -3.93%

- SPX PUT/CALL RATIO: as of 05/22 closed at 1.83

- Up from the day prior at 1.58

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 39

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.74

- Decrease from prior day’s trading at 1.77

- YIELD CURVE: as of this morning 1.45

- Down from prior day’s trading at 1.48

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, week of May 18

- 10am: House Price Index (M/m), Mar., est. 0.3% (prior 0.3%

- 10am: New Home Sales, Apr., est. 335k (prior 328k)

- 10am: New Home Sales (M/m), est. Apr., est. 2.1% (prior -7.1%)

- 10:30am: DoE inventories

- 11am: Fed to purchase $1.5b-$2b notes in 8/15/2022 to 2/15/2031 range

- 1pm: U.S. to sell $35b 5-yr notes

- 2pm: Fed to purchase $4.25b-$5b notes in 5/31/2018 to 5/15/2020 range

- 2pm: Fed’s Kocherlakota speaks in South Dakota

GOVERNMENT:

- President Obama attends campaign events in Colo., Calif.

- Mitt Romney won Republican primaries in Arkansas, Kentucky yesterday

- Nuclear Regulatory Commission Chairman Gregory Jaczko, who is resigning, holds news conference in Charlotte, N.C., 9:30am

- Senate in session, House not in session

- Senate Finance holds hearing on health-care delivery, with testimony from UnitedHealth, Advocate Health Care, Kindred Healthcare, Renaissance Medical Management officials, 10am

- NRC staff meets on agency’s yearly assessment of safety for Entergy Corp.’s Vermont Yankee nuclear plant, 5:30pm

- Financial Industry Regulatory Authority holds final day of annual conference

WHAT TO WATCH:

- Merkel faces Hollande pleas to shed “taboos” at summit

- Morgan Stanley defended its role in Facebook’s IPO after a Massachusetts regulator subpoenaed the bank

- Facebook investor sues Nasdaq over “mishandled” stock offering

- PetroChina looking at American, Caribbean assets, Jiang says

- U.S. April new home purchases forecast to rise 2.1% from March to 335k annual rate

- Barclays to raise $5.5b from sale of BlackRock stake

- U.K. retail sales fall most in two years as rain hits demand

- Japan’s April exports rise less-than-forecast 7.9% Y/y

- ECB’s Lipstok says no need for additional ECB stimulus at the moment, “no guarantee” Greece will keep euro

- BofA to buy back $330m of mortgages from Freddie Mac

- RailAmerica reviewing alternatives including possible sale

- SEC Chairman Schapiro says SEC’s JPMorgan review focused on VAR models

- U.S. consumer bureau seeks comments on prepaid debit card rules

- More CFOs willing to pay bribes, global survey finds

EARNINGS:

- Suntech Power (STP) 6am, $(0.49)

- Big Lots (BIG) 6am, $0.69

- Canaccord Financial (CF CN) 6:30am, C$0.09

- Hormel Foods (HRL) 7am, $0.41

- Trina Solar (TSL) 7am, $(0.27)

- Bank of Montreal (BMO CN) 7:30am, C$1.35

- Zale (ZLC) 7:30am, $(0.20)

- Apollo Investment (AINV) 7:30am, $0.21

- Genesco (GCO) 7:35am, $0.74

- American Eagle Outfitters (AEO) 8am, $0.20

- CAE (CAE CN) 8am, C$0.20

- Eaton Vance (EV) 8:30am, $0.48

- NetApp (NTAP) 4pm, $0.63

- Pandora Media (P) 4:02pm, $(0.18)

- PVH (PVH) 4:03pm, $1.26

- Hewlett-Packard (HPQ) 4:05pm, $0.91

- Synopsys (SNPS) 4:05pm, $0.55

- Semtech (SMTC) 4:30pm, $0.31

- Bristow Group (BRS) 5pm, $1.03

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

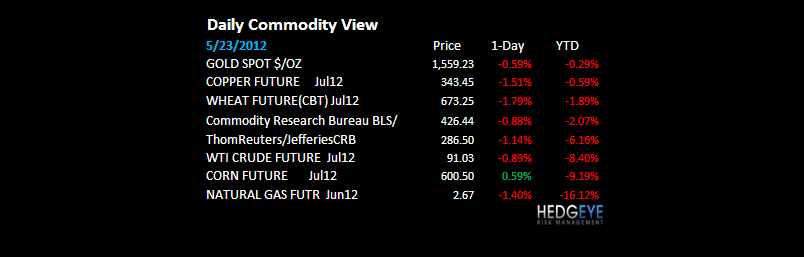

GOLD – plain ugly since the February top (down -12.7%) and this remains one of our top Global Macro short ideas that we’ll be discussing on our Best Ideas call at 11AM. Get the US Dollar right, and you’ll get a lot of big beta in macro right.

- Mining Slump Feeds M&A as Projects Overrun Budgets: Commodities

- Wheat Drops for Second Day as Price Surge Prompts Farmer Selling

- Rubber Set for Glut on Weaker China Growth Hurting Prices

- Copper Slumps as Euro-Area Crisis May Threaten Chinese Growth

- FreePort Founder Sells Diamonds as Investment Bet on China

- Oil Drops a Second Day on Iran Agreement, Rising U.S. Stockpiles

- Gold Declines in London as European Crisis Concern Boosts Dollar

- Cocoa Falls to Three-Week Low in New York After African Rains

- New Robusta Harvest in Indonesia’s Sumatra Seen Boosting Exports

- Iron Ore Heads for Worst Run Since October as China Demand Slows

- EU Farm Income May Drop for First Time Since 2009 as Prices Fall

- Rubber Retreats to Lowest Level in a Week on Greek Exit Concern

- Commodities to Gain on China’s Stimulus Pledge: Chart of the Day

- Oil Falls for Second Day on Iran Agreement

- Cotton Extends Slump to Lowest in More Than Two Years on Demand

- Palm Oil Drops to Lowest This Year on European Crisis Concerns

- Commodities Drop to Five-Month Low as Greece Concern Cuts Demand

CURRENCIES

EUROPEAN MARKETS

ITALY – getting powdered again this morning (down -2.5%, crashing since March = -23.4%) after reporting the worst consumer confidence reading in Italy since 1996 (pre-Euro). Germany/France draw-downs chasing the Spanish and Italian ones; DAX and CAC down -11.5% and -15.5% from March. Nothing is going to happen at their 3hr dinner tonight.

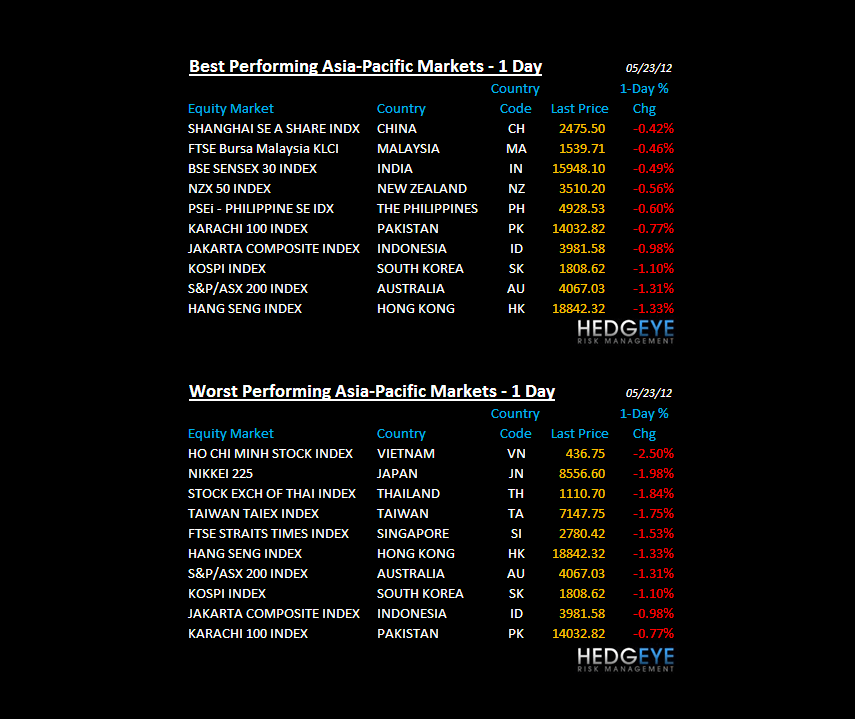

ASIAN MARKETS

JAPAN – finally seeing consensus walk our way on the massive interconnected global macro risk associated with Japan’s fiscal and debt problems. This is an Export economy that just missed another export number – that’s bad. Japanese stocks down for 23 of the last 33 days (draw-down = -16.6%). Japan matters to Global Demand.

MIDDLE EAST

The Hedgeye Macro Team