Conclusion: This story is playing out like it should fundamentally. That’s no surprise to us. What did come as a shocker was how management approached the quality of its results, and seemed to add every bit of opacity within its grasp. Is Ullman still there? There’s a long time to wait for any signs of momentum (on the upside) here. In the meantime you’re paying 15.2x a made-up non-GAAP EPS number that might or might not materialize before 2014.

As big as this event seems to be for JCP, it was really written in the cosmos. We didn’t exactly have a soft stance on this one.

June 11, 2011: HedgeyeRetail on The Closing Bell with Maria Bartiromo “The Street is at $2.77 [in 2013]. I think they’ll be lucky to earn a buck.”

June 11, 2011 Interview on "The Closing Bell"

What are we looking at today? After assuring the investment community that JCP would earn adjusted EPS of $2.16 (estimates had been coming down from $2.77), and GAAP EPS of $1.59, today he pulled the GAAP number. Earnings are going to come in closer to a buck.

The message he left us with is “We’ll still get to adjusted earnings of $2.16 – which is excluding all restructuring charges – but we’re not going to tell you what our GAAP target is. We’ll include restructuring benefits in our results, but not the costs associated with those benefits. As our results change each quarter, we’ll call the delta between what we report and the $2.16 a ‘restructuring charge’."

Seriously Ron…we’d expect this from your predecessor’s administration. But you? With your high-class pedigree? Someone is giving you bad advice.

Let us hit on a couple of items we liked in the quarter.

1) The dividend cut: The reality is that JCP has no business paying a dividend. 1Q Cash from Operations was –($577mm). Last year it was +$52mm. That's a $629mm hole. Its cash balance was down $928mm yy. JCP HAD to cut the dividend. In fact, we’d be concerned had they not.

2) It would be disingenuous for us not to state – flat out – that the store concept sounds very exciting. With dedicated shops from brands like Nike, Liz Claiborne, Tourneau, Levi’s, DC Shoes and about 95 other ‘higher-end-than-KSS and even Macy’s brands, this concept has teeth. We still don’t think that the goal of ‘a store for everybody’ is achievable in any way, shape or form. But the store as it is described today certainly has mid-upper mass appeal.

3) We still like the bargaining power JCP will have with vendors as it goes about its strategy. Johnson at one point made a comment like “even Gold Toe (Gildan) wants a shop in shop.” They also noted that there will be a very large Levi’s presence, indicating that VFC’s Lee and Wrangler did not make the cut, or play the price cut game required to secure the business. In the end, this is good for JCP. (We still think that the supply chain implications for the rest of the industry are extremely negative).

What we did not like…

1) From the very start of the presentation, management’s attitude was surprisingly cagey. They took the few statistics they they were willing to share , such as average spend and conversion, and attempted to twist them around to suggest that comping down 18.9% had some kind of positive read through. Let’s face some facts, comping down 20% and putting up a 28% decline in internet sales when Macy’s reported 33% growth in e-tail is just flat-out embarrassing.

2) It would have been so much better for them if he stood up and said “Hey everybody. Let’s get right to the heart of the matter. I realized this quarter that the forecastability of near-term customer behavior and competitive response in this business is much harder than what I am accustomed to. I’m pulling guidance accordingly because I don’t want our team focused on the wrong metrics. I’m going to quantify for you what deviated from my expectations, what I learned, and how I’m changing it.” For a guy with Johnson’s level of integrity, this could have taken an otherwise awful quarter and flipped it 180.

3) Though we like the concept in theory as noted above, we have major concerns about execution, capital investment needed to achieve the goals, and the duration mismatch between Johnson and investors (he gets paid in 6 ½ years when his warrants vest – few investors have that luxury).

4) The company identified additional cost saves – we’re guessing about another $50mm above the previously stated $900mm run rate JCP should achieve by year end (they indicated north of just $10-$20mm). Mind you, this means that it could get to this run rate on Jan 31, and would be a FY14 earnings event. Nonetheless, when a company puts up one of the most miserable top lines in recent memory, we rarely want to see Retail Austerity to sustain earnings. Management probably reads a statement like this and says ‘c’mon Wall Street…you want earnings and now you tell me not to cut costs?’ Our answer is “Yes. Some people want earnings via cost-cuts today, and they could care less about tomorrow. We’d rather you invest today and crush Kohl’s and Macy’s tomorrow.”

5) We have to point out the irony of management’s statement about employee morale, and how “it has never been better” since they switched from a commission to a salaried workforce. So let me get this straight, the employees are happy with sales down 21%? Wow… Johnson’s point is a good one. A salaried workforce leads to happier workers, which leads to better service, more customers, and perhaps better conversion (though we could argue against that one). In the end he thinks it is a big positive. He’s probably right. But again, we’d note that it is a positive within his 7-year duration – not the 2-3 year horizon by the average long-term investor.

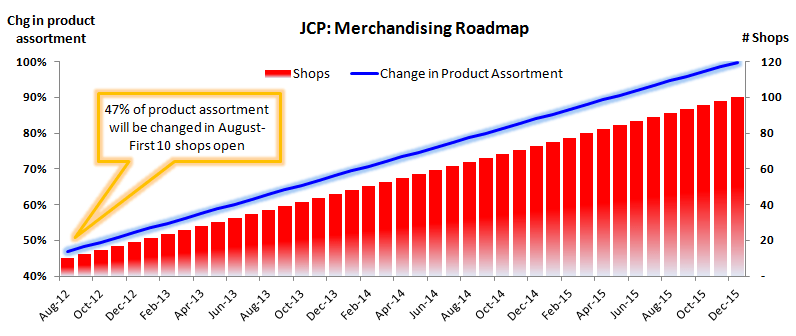

6) The shop in shop rollout will take time. Johnson is planning on rolling out 2-3 shops per month through December 2015 until JCP has reached 100 overall. Right now, we know ~30 of these shops (see matrix below). Additionally, there seems to be no shortage of applicants as JCP received 110 applications from brands interested in partaking in the new concept. Though the actual rollout may consist of 2-3 brands per month, our sense is we will be introduced to those participating in the "shops" in larger groups well ahead of their actual rollout not unlike we were yesterday. Assuming JCP maintains the 2-3 shop schedule, the rollout and ensuing change to the merchandise assortment could looking something like the roadmap below with 100% of the assortment refreshed come 2015 (47% will be changed by this August).

We’re at $1.00 for the year, and $1.75 in 2014. Timing is a very important consideration. If the company gets closer to $2.16 in 2014, then people will look towards a number above $3 another year out as the excitement around a big comp rebound and associated leverage ensues. That would, in fact, be an exciting story. But the absolute earliest there will be any form of visibility into any such rebound happens well into 2013. In the meantime you’re paying 15.2x a made-up non-GAAP EPS number that might or might not materialize before 2014. We can think of dozens of other places we’d rather be.

Brian P. McGough

Managing Director

Below are the highlights from managements presentation last evening:

"If I were to write the headlines for today, here is what I’d say. Our first 90 days are a little tougher than we expected. We expected the sales to be down, double-digit. They at the low end to that range, of our expectation, but the good news is, the transformation from my perspective is way ahead of schedule." - Ron Johnson, CEO

Progress to Date

- 2012 is the year of transformation; 2013 to be the year when takeoff starts, currently on day 105

- Expect to earn "good money" this year

First Quarter Results

"This has been a very tough quarter for us, but not necessarily unanticipated." - Michael Kramer, COO

- Revenues down 20%, comps down 18.9%

- GAAP EPS loss of $0.75

- Adjusted EPS of -$0.25

- Feb sales down 21%, saw 300 bps improvement in back half of the Q

- Continue to expect the back half of the year to be better

- Traffic down 10%

- Traffic down 6% Monday-Thursday

- Traffic down 12% on the weekends

- Conversion: 21% this year vs. 22% last year

- Average spend per visit $46 this year vs. $48 LY

- Primary issue is traffic due to like of couponing- 40% of last years transactions not only included a product on sales but had an additional coupon

Gross Margin -290 bps (270 bps due to selling margin reduction)

Expense Savings:

- Incurred $76mm in restructuring charges in Q1

- For the quarter, saved $121mm of SG&A YoY

- Now Committed to more than $900mm run rate of savings in 2013

3 opportunities to reduce costs

Inventory management: moving more to chase mode allowing merchants to really go after hits and misses

- Uncovered 17 weeks of inventory

- Department stores typically operate 15-18 weeks of inventory

- Some hard goods operate closer to 10-13 weeks (WSM)

- Feel JCP can get this to 13 weeks of inventory

- Had way to many skus with excessive weeks of supply

- By the end of 2012, this will free up $500mm of working capital

Legacy Systems: Streamlining internal systems

- 492 unique applications

- JCP should be operating around roughly 100 systems

- 88% of the applications were customized

- Translates to 90% of IT spend goes to maintenance

- 10% goes to strategic initiatives

Simplify Processes: Eliminating false sense of precision

- Extra processes create false precision

- Of the $900mm, have already identified and are executing on $650mm of it

Progress Update:

- Starting to act like a startup- need to be nimble and fast

- Marketing is gaining a lot of mindshare but is not communicating the pricing message and driving traffic

- Marketing is entertaining but not doing the hard work

- Now running the "Do the Math" advertising

- Need to convey JCP still has promotions, just not 500

- Started doing ROPs in major publications last week highlighting month long values

- Will be running ads like this every Thursday or Friday going forward

- Changed marketing to the "Big Deal" starts today

- Working harder from moving marketing from building a brand to convey pricing

- Did not have enough impact in the store for pricing

Strengthened the team:

- Added 41 people at the VP, SVP, EVP team level

- 20 internal promotions

- 6 new EVPs

- Team is dramatically different

Simplified the structure

- Had 92 buying teams to start the year, now 60

- Have eliminated commissions

Customer:

- Customers love what they see when they come to the store

- Customer Survey Improvements:

- Changes in brand perception:

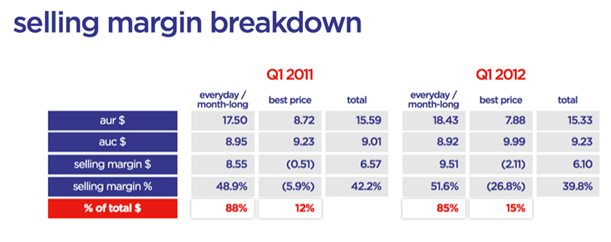

- Love the everyday price (67% product bought at highest point price)

- Best price purchases representing 15% of sales

- Have established a Predictable sales pattern

- Doing this with pricing strategy as the customer shops on their terms

- Only had 1 week with sales more than 10% outside of the range

Fashion Apparel Performing:

- Problems selling basics

- Home/basics men women kids remain weak

- On fashion, customers want better merchandise- Best performing retailers have fashion with credibility for great product

New Store design ahead of schedule:

- Have a 60,000 square foot warehouse, working on new store design which will be discussed in August

Shop strategy:

- March 15th, posted application for shops, got 110 shop applications excluding those already in discussion

- Now in a position for more choices in content than space

Product Update:

- Beginning in august, will have transformed 47% of content through new brand launches and improving current brands

New Brands launching the Fall

- JCP brand rolled out in August to both men's and women's

- Dream Pop for ages 7-14

- Betsyville by Betsy Johnson- handbags and accessories in 4Q

- LULU Guinness

- Vivienne Tam debuting in the Fall

- Royal Velvet- heritage brand for bed and bath, expanding exclusive license into furniture window and tabletop

- DC will be a foundational element of young mens

- Monet- categories like handbags and footwear

Powering up existing brands:

- Liz Claiborne, goal is to return LIZ to its heritage of well designed collection for working women

- Puma- athletic footwear and active wear, growing assortment dramatically in the back half of the year

- Xersion- Americas favorite active wear brand for the family

- Nike- have had partnership in footwear- introducing broader assortment of men's and women's

- St John's Bay- restoring the brand to it's roots, outdoor brand

- Worthington- one of the top 10 women's brands in America focusing on the modern career women

- Stafford- improving design, styling and fabrication

10 new shops announced in January

- Arizona Jeans- creating assortment of fashion denim for men's and women's in all new shop

- IZOD

- Liz Claiborne- honoring the customers ability to pull together a look with ease

- JCP brand- in addition to having fashion basics, will have a men's/women's shop rolling out in September of this year in all stores

- Levis- opening shops for both men and women for BTS season but will represent the most innovative Levi experience in the US

Spring Update:

- Corner stone of home will be Martha Stewart by March 1st, 2013

- Partnerhsip with Jonathan Adler called "Happy Chic"

- Michal Graves Design

- Bodum

- Design by Conran

- Lamour by nanette lepore (13-19 year old crowd)

- Georgina Chapmen expected to be in stores by Feb 2013

- Licensing agreement with William Rast- premium denim and sportswear apparel beginning in the Spring

- Nike- Building out men's/women's Nike Shops, most inspiring collection outside of Nike Freestanding stores

- Watchgear by Torneau for JC Penney

Guidance:

- Adjusted EPS of $2.16

- Taking off $1.59 GAAP guidance due to additional restructuring expenses

- Increased Marketing and 47% change in merchandise expected to drive traffic

- Shops will have a big impact on the business going forward

- Discontinuing dividend

- Will generate over a $1bn in cash before capex- plan to invest cash in the business which will be a better return than a dividend

August Meeting Agenda:

2Q results

Merchandise strategy

New technology platform

New store design

Q&A:

Inventory:

- Have done best valuation on aged inventory

- Have removed aged inventory

- Goal is to get inventory turning faster which will generate a profound amount of cash

- Reduced inventories will help push margins over 40%

Cost Savings

- $900m net run rate by year end

- Do anticipate increased investing

Merchandise priorities

- Those introductions shared today reflect gaps that JCP has had in the past

- Expect to see a thoughtful review of legacy and heritage brands that will be restored in shop environment as well as newness in all categories within the store

- Have had the goal to reach younger customers without sacrificing heritage customers

Shops in Stores

- Goal is to get shops in as many stores

- At launch, shops will go into A, B, C stores (about 700) with sizing varying

- Largest stores are called stores (2000 square feet) done selectively

- Shops minimum 500 square feet

- 3rd is boutique, 300 square feet which may not have all the walls

Store performance:

- Best performance was in the smallest small town stores

- Took the time to really understand the pricing strategy

- Performance across all other markets was virtually identical within 1%

- Continue to expect to operate all stores vs. any closures

- A new priority is to work and reevaluate the store portfolio but this hasn’t been focused on early on

Customer Demographic

- Are seeing that JCP has been engaging a younger customer

- Hard to say with precision how the mix is changing this early

- Will provide greater detail in August through enhance analytics

Merchandise Selection

- With all of the shops, engineering all of the shops to be in line with expectations of the consumer

- Torneau will help open the doors to all of the brands like Sephora did for makeup

- Can do large brands like Nike, Levis, etc.

- Have yet to enter certain categories, food, beverage, hardlines, etc.

$1bn in cash flow

- This is before capex

- During the transformation will still generate cash

Guidance

- No Comp guidance

- Expect sales to improve throughout the year

- Half of the assortment will be new

- Changes in content will update the fashion with fewer key items

- Inserting freestanding shops will help drive volume

Employee Morale

- Difficult to know customer morale from the top

- Store employees have embraced the change, easier to take care of customers, stores are cleaner, less recovery

- Most employees were thrilled with commission changes

- Non commission force will create a better customer service experience overall

Market Share

- Keeping the customer is job number 1

- Currently losing customers

- Customer has not gone to primary long term competitors, i.e KSS comping essentially flat

- M said in some markets against JCP have gained share but comps have slowed

- Believe a great deal of the slowdown is lack of refilling basics

- Customer is clearly buying less- want to earn him/her back

Basics

- Plan on winning in basics

- Configured basics for a promotion strategy (bulk)

- Dinnerwear- JCP selling 72 piece innerwear sets- need to reconfigure the basics

- Working to get merchandise aligned with new strategy

- Gold Toe wanted to put in a Gold Toe shop

Competition:

- No major competitive response to changes at JCP

- TGT had better performing spring apparel

- TJX had strong results

- Old Navy improving

- Those succeeding are using an EDLP strategy vs. the promotional strategy

Category issues

- Overall, opportunity to better communicate value proposition

- 3 categories: fine jewelry, home, basics (towels, underwear, socks)

- Fine jewelry: lowered in March all of fine jewelry prices

- In April, made jewelry pricing better everyday

Traffic

- Will learn more in August about new store design that is about creating traffic outside of the product

- The old way of driving traffic was a coupon or a sale

Impact of SG&A savings on sales

- Have to take a look at the base

- Historically over the past 5 years of sales decline JCP has not been reducing labor force in stores

- Have had an over managed over processed labor force in stores- working to simplify that base

- Want to develop a high service model

- Conversion was hardly effected thus far