The Knapp Track numbers for April suggest a slight sequential improvement in casual dining sales trends from March.

Malcolm Knapp released his Knapp Track casual dining sales numbers for April this weekend. This release was a departure from Knapp’s usual release, which comes in the form of a longer text report offering different insights into consumer trends during the month concerned; this weekend Knapp released the numbers alone with the text report, presumably, to follow in the coming days.

Estimated Knapp Track casual dining comparable restaurant sales grew 0.8% in April versus an estimated -0.7% in March. The sequential change from March to April, in terms of the two-year average trend, was 30 bps. While this is an improvement, the two year average trend is still well below the strength we saw in December through February.

Estimated Knapp Track casual dining guest counts declined -1.9% in April versus an estimated -3.4% in March. The sequential change from March to April, in terms of the two-year average trend, was +50 bps. This is an improvement but the decline in March was so substantial that a more sustained move higher will be necessary to convince investors that traffic can get back to positive territory.

Takeaways

Besides the broader casual dining group, for Darden and Brinker this result is especially meaningful since those companies’ systems represent a large portion of the unit base from which the numbers are calculated.

Traffic trends remain disappointing; it seems likely that weather was supporting traffic trends for much of 1Q. Now that the weather impact has dissipated, we are seeing numbers more representative of the true traffic trends in casual dining.

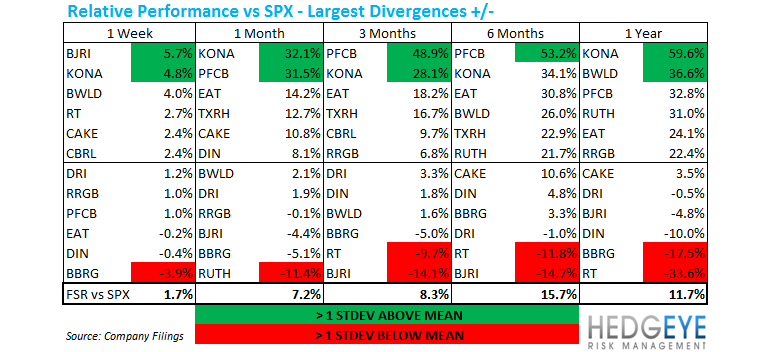

The price action is confirming our CASUAL DINING CAUTION stance we took ahead of 1Q earnings season. The group’s performance versus the broader market is slowing markedly. BWLD, however, remains a volatile name and outperformed the market last week by 4%. We still like BWLD on the short side but there are no catalysts until the company reports earnings on July 26th. The stock has not been performing very strongly relative to its peers over the last three months; we think consensus is too bullish on FY12 EPS.

Howard Penney

Managing Director

Rory Green

Analyst