Conclusion: Macy’s 2H guidance supports our concern about the stepped-up competitive pressure in the mid-tier later this year. Yeah, we know, Bloomies is high end, and much of Macy’s is not exactly KSS-competitive. But they definitely compete on the fringe. Mgmt went as far as to say that they are seeing definite strength in areas where they compete w JCP. One other interesting dynamic we see is analysts are asking Macy’s management about input costs. We think that’s actually a very relevant question, but probably for a different reason. The reality is that input costs don’t really matter much anymore. They are known. They are built into the plan – for the vendors, at least. And those prices are tentatively set with retailers. But ultimately, we’re going up against significantly higher AUR’s vs 2H11, and we absolutely NEED to maintain pricing integrity in 2H for margin integrity to hold. People forget that there are two elements to the gross margin equation – and only one of them is cost.

While playing the guidance game is not our forte, the reality is that this is the first quarter in 5 where Macy’s did not increase its outlook. With the stock up 23% YTD and short interest as a percent of float testing historical lows of 2.1%, we absolutely need to see positive earnings revisions to move this stock higher. Our thesis regarding stepped up competition in the mid-tier in 2H will need to be dead-wrong in order for that to happen (or JC Penney will need to fall flat on its face and cede share increasingly to M).

What Drove the Beat?

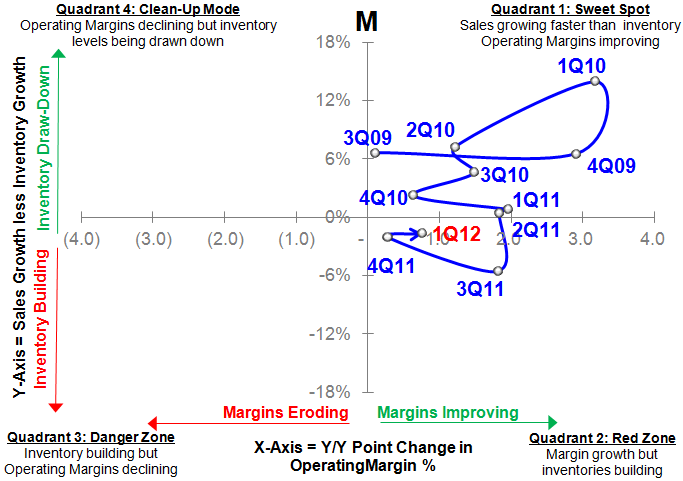

The $0.03 beat in 1Q12 was a result of operating expense leverage in light of 2 new store openings in Salt Lake City, UT, and Greendale, WI. The operating expense leverage of 110bps was primarily due to improved profitability in the credit portfolio which is expected to increase $15-$20mm this year. Additionally, M benefitted from reduced D&A though partially offset by increased investment spend in OMNI Channel (My Macy’s, MAGIC selling, etc.) as well as higher pension expense. Inventory growth improved 2 points sequentially in Q1 +6% though the sales to inventory spread remained unchanged -2%.

Deltas in Forward Looking Commentary?

In order to properly measure performance relative to original expectations, we look at management’s 2012 guidance headed into the quarter as well as the key deltas in Q1 results vs. expectations :

Store And Sales Growth

- For planning purposes, we are assuming a comp store increase of approximately 3.5% on a 52-week basis UNCHANGED- continue to expect 3.5% for the remainder of the year and now expect 3.7% for the full year

- Our total sales, including this extra week, are expected to be up approximately one point over our comp store sales increase UNCHANGED

- Now, obviously, in Q4, given that extra week, we’re expecting a much bigger gap – in fact, 3.5 points higher total store growth than comp UNCHANGED

- However, in the first three quarters of the year, total sales growth is expected to be slightly below our comp store growth due to the locations that we closed at the end of 2011 UNCHANGED- revenues +4.3% on +4.4% comp

New Store Openings

- We are planning to open two new stores in 2012 – both, in fact, next month – one in Milwaukee and one in Salt Lake City COMPLETE

- We are also opening five new Bloomingdale’s outlets during 2012, bringing the total number to 12 UNCHANGED

Gross Margins, Income And Credit

- We are assuming a flattish gross margin rate for the year, although we could have continued pressure from free shipping, given the sales growth expected in the omnichannel business UNCHANGED- GM was down 30bps in Q1

- On the SG&A front, we expect to be able to continue to improve our expense rate as a percent of sales UNCHANGED- SG&A leveraged 100bps in Q1

- We expect our income from the credit portfolio to increase approximately $15mm to $20mm during 2012 UNCHANGED- credit contributed to expense leverage in Q1

- But we are expecting big variances when we look at the comparison to last year in each quarter UNCHANGED- 3Q expecting unfavorable impact

Expenses, Depreciation, Tax Rate And CapEx

- For the year, we’re expecting retirement expense – pension plus SERP – to increase by approximately $65mm UNCHANGED

- While depreciation is expected to decline approximately $25mm for the year UNCHANGED

- For interest expense, we’re assuming approximately $435mm to $440mm for the year UNCHANGED

- And we’re assuming an effective tax rate of 36.95% for 2012, although it will vary by quarter UNCHANGED

- And our CapEx budget for 2012 is $850mm INCREASED: now $950mm but will return to $900 level in 2013

EPS And Costs

- So, net-net, we are assuming EPS on a diluted basis of $3.25 to $3.30 for 2012 UNCHANGED0 $0.09 below consensus at the high end of range

Highlights from the Call:

Revenues: +4.3%

- Sales continued to be strong at Macy's and Bloomingdales both in-store and online (online +34%)

- Sales performance broad based

- Men's, center core (watches jewelry handbags cosmetics shoes etc.) and home strong

- Feminine apparel stronger in Feb and March than in April but feeling better particularly in classic

- Saw strength in impulse apparel (women's age 22-30)

- Junior business continued to be weak

- Private brands continued to perform well (charter club, bar 3 strongest, new ideology brand launched recently doing well)

- Geographic: southern markets continue to outperform (FL, TX, Hawaii)

- Strength in other markets demonstrate the power of My Macys and more localized assortments

- AUR +8% with units down 4%

Gross Margin: 38.8%, down (-30bps)

- Merchandise margin flat in the first quarter

- Rounded the impact of free shipping but growth of Omni channel continue to put pressure on GM

Inventory Improvements:

- Inventory +6% (increase in in-transit merchandise, inventory +3% net payables)

- More opportunity to satisfy demand with inventory from other stores and DTC as well as online demand from in store

- Now have over 80 stores equipped to drop ship and expect over 290 store fulfillment locations by Holiday

- Drop shipping Should enable more productive inventory and store square footage

Operating expenses: +1%; 110bps of leverage

- Credit was the biggest factor favorably impacting expenses

- Expect credit profitability to increase by $15-$20mm for the full year (1Q consistent with higher end of annual guidance)

- Benefitted from lower D&A

- Offsetting: higher expense related to Omni channel investments, higher pension expense

EBIT +80bps YoY

Cash Flow $265mm vs. $67mm LY

5 primary drivers:

- Higher net income

- Last year, pension contribution of 225mm in quarter

- Tax payments and reductions in deferred taxes last year (246mm unfavorable last year)

- Inventory net of payables was $118mm favorable vs. last year

- Reduction in prepaid expenses due to Lord and Taylor proceeds that had been put in escrow were used to purchase 2 key parcels of flagship in Union Square Can Francisco.

Outlook:

Second Quarter:

- Sales growth to be consistent with +3.5% with May higher and June/July lower

- GM expected to be flattish

- SG&A expected to increase more in 2Q relative to last year than it did in the first Q primarily because credit profitability is only expected to be up slightly

- In 3Q, credit profitability is expected to be lower than last year by 40-50mm but still expect 15-20mm increase in full year credit profitability

Full Year:

- Guidance is unchanged at +3.5% comp for the remainder of the year or 3.7% for the full year

- EPS also remains at $3.25-$3.30

- Capex now expected to be $950mm although next year it will return to $900 level as previously discussed

- Plan to continue to focus on OMNI Channel and better tailor assortment to localized needs.

- Enhanced MAGIC Selling expected to continue to differentiate Macy's from competitors

Q&A

JCP:

- Have seen an uptick in business in markets where they compete against JCP

- Marketing strategy has been unchanged since the announcement of JCP's new strategy

- There are strategies in place to maintain the customers coming over from JCP

Renovation at Herald Square:

- Will have an impact on the comp

- Will have some effect on the total but not material

Product costs:

- Are expecting to see some relief in 2H

- Don’t expect an impact until later in 3Q

Buybacks

- 1.1bn remaining in the authorization

- Have not quantified exact amount but idea is to use excess cash to buy back stock

Inventory:

- Net of payables up 3% so below 2Q sales expectations

- Will take longer to figure out optimal place by cetegory for inventory levels

- Expect to see this in 2013 and beyond

- With more categories online that can be fulfilled from store better able to satisfy demand

- Big chunks of inventory available in store but not yet online

- Will be testing putting inventory up online that will be 100% fulfilled from in-store

- Site to store to door rolling out by category- accelerating rollout because it has been so successful

3Q Guidance:

- Not giving guidance but quarter but 40-50mm credit profit compare will put a lot of pressure on earnings

SG&A

- Committing to reaching 14-15% EBITDA rate

- Current game plan in place to reach 14%; getting to 15% will require new thinking

- While investing in growth, doing so while keeping in mind bottom line improvement

Merchandise Margin:

- Think there is huge opportunity to improve inventory productivity that will help gross margin

- Plan to pull inventory from locations where they would be sold for less to preserve margins

- Expect gross margin to be flattish for the year

- Did not increase promotions in the quarter

- Clearing the cold weather goods when the weather was hot

Women's Apparel:

- Feel very good about regular priced selling of the new goods

Millennial Customer Initiatives:

- Spending a lot of time rethinking how product is selected for stores

- Launched Bar 3 last year as a way to use private label market to help (bar 3 geared toward older customer)

- Reviewing marketing to be sure reach out is working; digital, social media, etc.

- Juniors doing less well due in part to market overall, M needed to reload the strategy and restart overall- feel it will be much better a year from now

Omni Channel

- Will continue to improve and add new components to MAGIC selling

Brazil Brazil Brazil Campaign

- Very early to tell but product from Brazil doing very well in store

- Doing some tailoring by market mostly in terms of size of the Brazil campaign

- Sticking to overall marketing program

Bloomingdales:

- Continues to be very strong, no major callout there

Home Business:

- Big ticket has been unbelievably strong- think the trend will continue

Amazon

- As much a competitor as JCP, KSS, etc.

- In most of the businesses, the in store experience is still very important to the consumer

- Expect it to be very challenging for an internet pure play to compete

- In fashion business, having stores is still a competitive advantage

Potential for short term borrowing:

- Not something that would be done this year given cash position but have started to test the opportunity