We see an asymmetric setup for Jack in the Box over the next three years. For any clients looking for ideas on the long side, here is our favorite one on the three year duration.

The price of oil declining has moved some investors to look more closely at the consumer discretionary sector for long ideas. Jack in the Box is one name that we like here and now. The next catalyst for this stock is when 2QFY12 earnings are reported on May 15th. We expect same-restaurant sales to beat expectations at Jack in the Box. In addition, we believe that management will provide incrementally positive commentary on Qdoba, its growth prospects, and its operating margins.

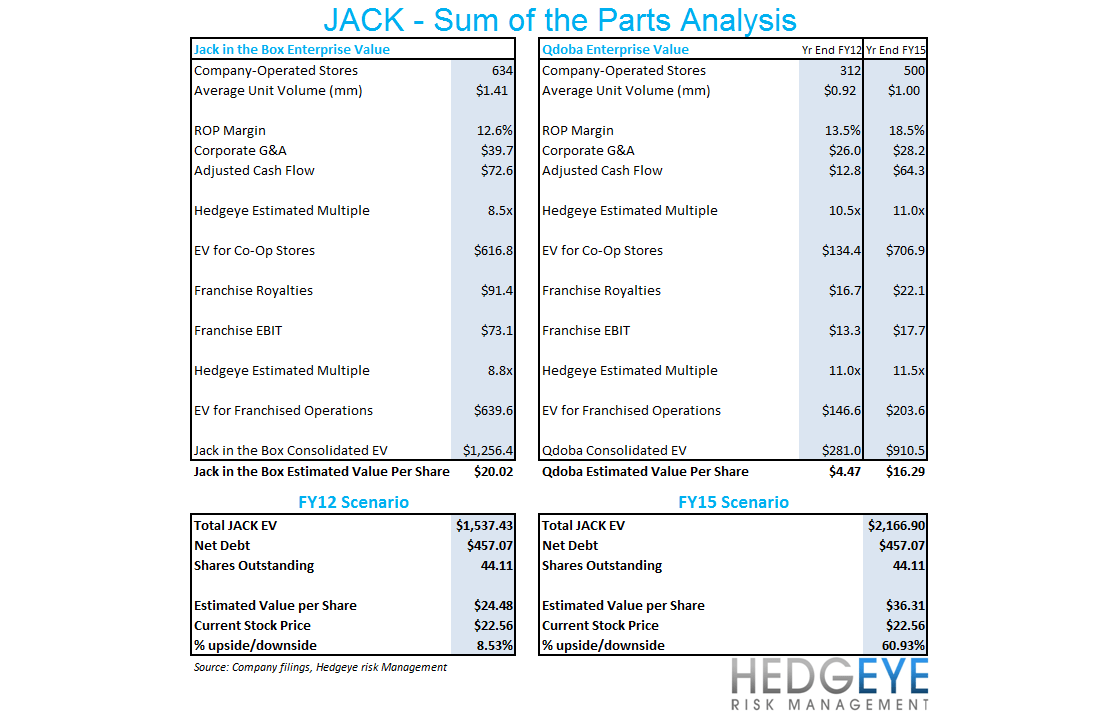

Following the investor day, much of the skepticism was based on Qdoba’s restaurant operating margin trending at 13.5%. As the asset base matures we expect margins to rise. In its Investor Day materials management highlighted that, for Qdoba restaurants open more than three years, restaurant operating margins are at 18.5%. We see an asymmetric risk setup for JACK at this point given the margin expansion that should follow as the Qdoba unit base matures. The leverage in this stock, as we see it, lies almost entirely with Qdoba. The company unit base is projected to double by 2015. If growth targets can be reached and unit economics improve, we see as much as 60% of upside in this name over the next three years.

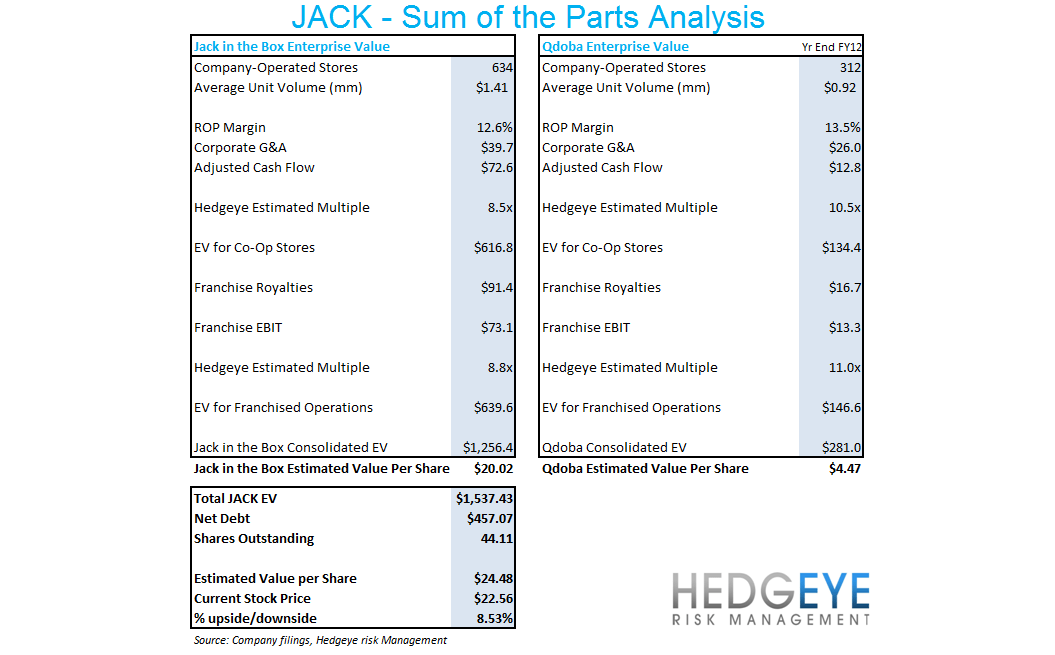

Sum of the Parts – FY2012

How high margins can go is largely a function of how successful the company will be in increasing same-store sales. Our sum of the part analysis, below, outlines our fundamental view on the stock over the next 6-9 months. We believe that there is 8.5% of upside at current levels. That view is predicated primarily on growth from Qdoba and the investment community awarding the stock a higher multiple, something that we think is overdue. Wendy’s and Sonic include some of the names that are trading at higher multiples than JACK. Given that Jack in the Box has completed a reimaging program of its main concept and is set to generate free cash flow of ~$75mm this year while driving the Qdoba growth story forward, it seems incongruous that Wendy’s, which is facing some serious issues over the next several years, would trade at a premium to Jack in the Box.

Sum of the Parts – FY2015

It is always difficult to forecast what the future holds but, in the case of Jack in the Box, we see much more upside than downside. Management is planning on growing the company-owned base of Qdoba stores to grow by 15-20% per year through 2015. Franchisees are expected to add 30-40 units per year over the same time period. Qdoba’s growth and expanding margins are the primary components of the long-term TAIL story. The margin expansion that we show in the sum-of-the-parts analysis, below, can be attributed to what we expect to be a maturing store base, stronger sales trends, and opportunistic acquisitions of franchise restaurants.

Even assuming an enterprise value of Jack in the Box level with what it is today, we believe that Qdoba’s growing and maturing store base can deliver outsized returns to shareholders. Given that, according to Bloomberg, the sell side is currently divided on the stock – 3 Buys, 7 Holds, 3 Sells – there are plenty of skeptics to be won over if management can hit targets over the next few quarters.

Quantitative Setup

Keith bought JACK today in the Hedgeye Virtual Portfolio as his model was indicating that the stock was immediate-term TRADE oversold. Given Keith’s quantitative view of the stock along with our fundamental view on the stock, we believe that Jack in the Box is the most attractive stock in QSR over the longer term TAIL duration.

Howard Penney

Managing Director

Rory Green

Analyst