Let's face it. No one has ever HAD TO look at either WWW or PSS. Now we're left with the same high-quality leadership at WWW, but at a significantly larger company. This story has legs.

With WWW trading down on the news of the PSS/WWW deal, we see it as a buying opportunity. While WWW paid $1.32Bn the PLG business (10x EBITDA) at the higher end of expectations, the accretion to next year’s EPS after 1x costs are absorbed is attractive and appears conservative.

- For starters, WWW is assuming MSD-HSD sales growth for the PLG group over the next few years, which we think is very conservative.

- Over the last two-years, this business has grown in the high-teens and we think this business could and should grow in the low-to-mid-double-digit range reflecting ~12% growth at wholesale and ~6% growth at retail. Even if we were to assume that the retail business (primarily Stride Rite) remains flat, we’re still looking at +9%-10% revenue growth here. These are not heroic assumptions and reflect a slowdown from current growth rates as reflected in the table below. We can't imagine that WWW management, which we view as the small cap footwear equivalent of VF Corp (i.e. very good) would buy into a permanently lower-growth story with no plans to leverage existing platforms.

- With 90% of PLG’s revenues generated domestically, WWW should be able to leverage existing distribution channels that it’s established to drive PLG growth with 1/3 of sales coming from overseas. This is expertise Sperry lacked under its prior structure, which should drive continued growth at wholesale.

- At Saucony, athletic footwear continues to outpace the industry particularly running. We see little reason this brand should grow less than 10% in 2012. The traction it has gained among elite runners over the past three years can't be given back easily.

- As for Stride Rite and Keds, if WWW can get these brands to grow at a MSD rate, we think the PLG business could grow in the teens.

- In addition, total PLG operating margins were 6.9% in 2010 and while F11 margins came in at 3.6% due primarily to retail store underperformance, we think this business could run at a HSD margin or higher with the drag on retail removed.

- Included in these assumptions is $16mm in incremental amortization offset by the initial impact of $8mm in identified synergies, which will start to be realized in F13 as reflected in the table below the full benefit of which should be realized by F14.

- Further, given the scale of WWW’s supply chain and operating team, we’d expect additional SG&A leverage opportunity.

- Our biggest concern is all the IFs just mentioned. WWW has proven to be extremely astute at integrating new content, turning around existing brands, and growing brands that already have relevance with the consumer. This, however, is a short cruise into uncharted waters, to say the least. WWW is acquiring four brands with over $1Bn in revenue -- equal to 65% of its existing size. The saving grace is that Matt Rubel did them a favor by consolidating back office for PLG under one roof, which makes it a cleaner sweep with lower risk for WWW.

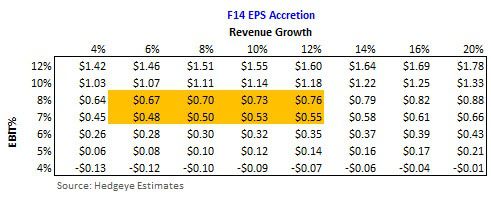

- WWW will be taking on approximately $1.275Bn in debt in the form of $900mm in term loans and a $375mm notes offering at LIBOR + 200-300 suggesting ~$50mm in interest expense and a net debt/EBITDA ratio of 4.2x. The company expects to get that down to 2.2x by the end of F14 suggesting ~$250mm in annual debt reduction and ~$40mm in interest expense as reflected in our table below. Additional considerations include a 25% tax rate and ~49mm shares outstanding.

WWW has historically traded around 14x forward earnings. With earnings of approximately $2.75 this year and ~$3.00 in F13. At 14x this year’s EPS we think there is only $1-3 of the deal currently reflected in the stock. We think EPS accretion could be closer to $0.50 in F13 compared to the range of $0.25-$0.40 suggested and could be up to $1.00 in incremental EPS in F14 vs. a suggested range of $0.50-$0.70, which is worth at least $6-$8 in value today. This implies a $45-$47 stock 10%-15% above current levels with additional upside from PLG 2-3 years out. Given the synergies available and what appears to be conservative growth assumptions for the PLG brand over the next several years, we like $4 in earnings power at this price.

Casey Flavin

Director