TODAY’S S&P 500 SET-UP – April 30, 2012

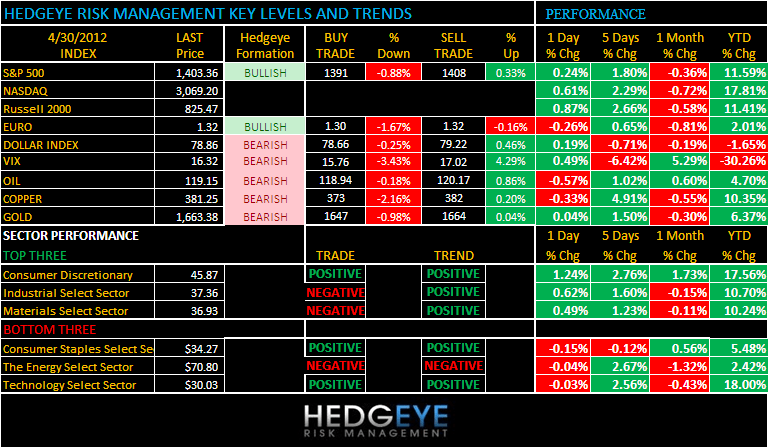

As we look at today’s set up for the S&P 500, the range is 17 points or -0.88% downside to 1391 and 0.33% upside to 1408.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 4/27 NYSE 1005

- Down from the prior day’s trading of 1071

- VOLUME: on 4/27 NYSE 787.79

- Increase versus prior day’s trading of 0.97%

- VIX: as of 4/27 was at 16.32

- Increase versus most recent day’s trading of 0.49%

- Year-to-date decrease of -30.26%

- SPX PUT/CALL RATIO: as of 04/27 closed at 2.21

- Up from the day prior at 1.31

CREDIT/ECONOMIC MARKET LOOK:

GROWTH – slowing, sequentially, is now a reported fact – but Treasury Yields (10yr 1.93%) and Equity Markets (making lower-highs, globally, since Feb-March) have been very stealth in discounting that before the Sell-Side has. This morning’s South Korean Export number was awful at flat y/y (ie no growth).

STAGFLATION – politically, it’s harder to say we have that in the USA right now (b/c of how we calculate GDP and inflation) than it is to say they have it in Europe. In Italy, the CPI was reported at +3.8% y/y for April, which is nauseatingly high relative to the no growth in Italian GDP (or France, Spain, etc). Brent oil $119 is a consumption killer.

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.92

- Down from prior day’s trading of 1.93

- YIELD CURVE: as of this morning 1.67

- Decrease from prior day’s trading of 1.68

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Personal Income, Mar., est. 0.3% (prior 0.2%)

- 8:30am: Personal Spending, Mar., est. 0.4% (prior 0.8%)

- 9:45am: Chicago PMI, Apr., est. 60.5 (prior 62.2)

- 10:00am: NAPM-Milwaukee, Apr., est. 53 (prior 51.8)

- 10:30am: Dallas Fed Manu. Act., Apr., est. 8 (prior 10.8)

- 11:30am: U.S. to sell $30b 3-mo., $28b 6-mo. bills

- 5:30pm: Fed’s Fisher speaks on jobs in Beverly Hills, CA

GOVERNMENT:

- Japanese Prime Minister Yoshihiko Noda visits White House to discuss U.S.-Japan Security Alliance, economy and trade

- President Obama to speak at Building and Construction Trades legislative conference

- House, Senate not in session

- Supreme Court issues orders only

WHAT TO WATCH:

- Collective Brands said to select group made up of Wolverine World Wide, Golden Gate Capital as leading contender to buy co.

- Warner Chilcott said to be weighing options including possible sale after receiving interest from strategic, private-equity buyers

- Spain’s economy enters second recession since 2009

- LightSquared said to receive weeklong extension from creditors

- Consumer spending in the U.S. probably climbed 0.4% in March as incomes grew, economists est.

- Occupy Wall Street demonstrators plan marches across the world tomorrow calling attention to what they say are abuses of power, wealth

- Chrysler’s Dodge Dart overcoming snags before start of production, will have high-mileage version ready in 3Q

- Apple uses offices in states other than California, countries outside the U.S. to help minimize its overall tax burden: NYT

- Yahoo urged shareholders not to back board nominees put forward by holder Third Point

- Boeing will ship all four 787 composite-plastic Dreamliners to Air India, the carrier that demanded $1b in compensation after production delays

- Apple, Google deserve to be part of Dow Jones industrial average: Barron’s

- Goldman Sachs Asset Management Chairman Jim O’Neill reported by Sunday Times to be a candidate for Bank of England governor

- Accretive Health said yesterday it’s working with advisers to address concerns raised by Minnesota AG that it puts bedside pressure on patients to pay bills

- Haemonetics agreed yesterday to buy blood-collection business of Pall Corp. for $551m in cash

- Apple said to have held talks to let subscribers of Epix movie chanel watch films on its set-top box

- Starwood Hotels plans to re-enter Iraqi market almost 20 years after exiting as a result of Gulf War

- BOX Options Exchange won approval April 27 to become a U.S. securities exchange

- Dewey Leboeuf said to end Greenberg Traurig merger talks

- Analysts predict U.S. shares will rise this year to boost the S&P 500 to record, even as Wall Street strategists say the best is already over for American equities

- No U.S. IPOs expected to price: Bloomberg data

- Week Ahead : U.S. Jobs, French Debate, Buffett: April 30-May 5

EARNINGS:

- CNA Financial (CNA) 6am, $0.68

- Humana (HUM) 6am, $1.55

- Loews (L) 6am, $0.90

- LyondellBasel (LYB) 6am, $1.04

- Watson Pharmaceuticals (WPI) 7am, $1.59

- Harman International Industries (HAR) 8am, $0.67

- UDR (UDR) 8am, $0.34

- DiamondRock Hospitality Co (DRH) 8am, $0.07

- Mercury General (MCY) 8:30am, $0.68

- Canadian Oil Sands Ltd (COS CN) 4pm, C$0.54

- SBA Communications (SBAC) 4pm, $(0.18)

- Veeco Instruments (VECO) 4pm, $0.22

- Anadarko Petroleum (APC) 4:01pm, $0.83

- Hologic (HOLX) 4:01pm, $0.33

- CNO Financial Group (CNO) 4:02pm, $0.13

- Plum Creek Timber Co (PCL) 4:02pm, $0.24

- Shutterfly (SFLY) 4:02pm, $(0.21)

- PMC-Sierra (PMCS) 4:04pm, $0.05

- PartnerRe (PRE) 4:04pm, $2.01

- Forest Oil (FST) 4:05pm, $0.20

- Enbridge Energy Partners (EEP) 4:08pm, $0.37

- Flowserve (FLS) 4:09pm, $1.61

- Herbalife (HLF) 4:10pm, $0.81

- McKesson (MCK) 4:10pm, $2.06

- FMC (FMC) 4:30pm, $1.85

- Masco (MAS) 5pm, $(0.01)

- Suncor Energy (SU CN) 10pm, C$0.81

- Jacobs Engineering Group (JEC) Post-Mkt, $0.74

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Speculators Miss Biggest U.S. Corn Sale Since 1994: Commodities

- Wheat Drops as U.S. Crop Development Accelerates; Soybeans Fall

- Brent Oil Heads for First Monthly Drop Since December on Demand

- Copper Falls 0.5% to $8,376 a Ton; Nickel Declines, Tin Gains

- Gold May Gain as Lower Borrowing Costs, Debt Crisis Spurs Demand

- White Sugar Rises as Lower Prices May Spur Demand; Coffee Falls

- Mercuria Said to Hire Perkins as Agriculture Head in Singapore

- Palm Oil Drops to Pare Monthly Advance on Higher Output Concern

- U.S. to End Fuel Exports as Oil Discount Disappears, Facts Says

- Hedge Funds Cut Bullish Gasoline Bets on Prices: Energy Markets

- Roomier Pig Pens May Bolster Pork Prices as European Output Ebbs

- Merkel’s Green Jobs Drive Faltering With Cuts for Solar: Energy

- Record-High Gasoline Burdens Consumers as Europe Fights Slowdown

- Funds Miss Biggest Corn Sale Since 1994

- Fortescue Seen Luring Anglo-to-Glencore on China Iron: Real M&A

- China Forestry Logging Assets Hold Value, Investor Carlyle Says

- Crude April Trading Range Tightest Since 1995: Chart of the Day

CURRENCIES

US DOLLAR – whether people want to admit it or not, the US economic data was bad last week (jobless claims and GDP) – if the only thing left keeping asset prices afloat is the hope for iQe4, that’s dicey. We’ve seen this movie before – holding the USD down like a ball under water (down 6 of the last 7 wks) ends in deflationary tears when it pops back up.

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team