“Capital flight is a traditional response to currency collapse.”

-Jim Rickards

During most “bull” markets you see a decisively bullish pattern of rising volumes and fund flows to those markets. Not this one.

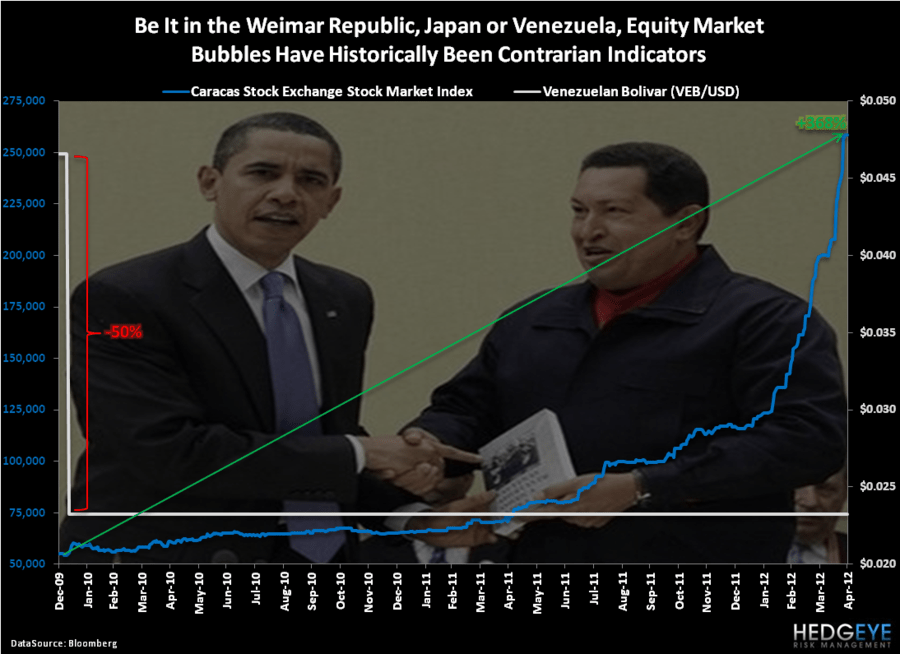

Not in Venezuela either. While Chavez has been less subtle about devaluing Venezuela’s currency than Ben Bernanke has ours, at up +121% for 2012 YTD, the fund flows to the Venezuelan stock market are as dead as Keynes too.

The failed political strategy of inflating asset prices via Currency Debauchery is not new. Neither is the hyperinflation sometimes born out of those strategies. As Jim Rickards reminds us in Currency Wars, “In 1922, the inflation turned to hyperinflation as the Reichsbank gave up trying to control the situation and printed money frantically…” (page 59)

Back to the Global Macro Grind…

Don’t worry, we don’t have hyperinflation in the USA yet. Nor are we likely to if the Global Macro Ball that is being held underwater (the US Dollar) suddenly pops up. That, last I checked, has Deflated The Inflation in a hurry, multiple times in the last 5 years. So manage your risk accordingly.

People aren’t stupid. If you burn their bucks with broken promises of iQe upgrades over, and over, and over again – they’ll stop giving you their hard earned Dollars to burn. Selling Commodities and Equities into their Q1 tops of 2008, 2010, 2011 proved to be very smart 3-6 month timing decisions. When it comes to the pending flight of your capital, you don’t want to miss that flight.

Last week’s rally in asset price inflation was trivial. As the US Economic data worsened, expectations for iQe4 rose. Whenever that happens – and it has happened multiple times in the last 5yrs – the US Dollar goes down, and asset prices catch another lower volume bid. In context, here’s how that looked last week:

- US Dollar = down another -0.6% to $78.71 (down for 6 of the last 7 weeks)

- SP500 = up +1.8% (getting back to flat for April, right on time, into month-end)

- CRB Commodities Index = +1.4% (led by Natural Gas, up +14% on the week)

Now political people really like to argue with me on this, primarily because I’m holding them accountable for not only Policies To Inflate, but also A) the shortened economic cycles and B) amplified market volatilities born out of their policies.

Fortunately, the data doesn’t lie; politicians do. Growth Slowing again is as obvious as the sun rising in the East. If an un-elected Central Planner in Chief didn’t arbitrarily decide to move the goal posts on January 25th, 2012 (pushing easy money to 2014), I don’t think the US Dollar would have had this decline – and I don’t think US Growth would have slowed like it just did.

Here’s what US GDP Growth looked like in Q1 of 2012:

- Q1 2012 GDP slowed to 2.2% from 3.0% in Q4 of 2011

- Q1 US Fixed Investment Growth slowed to 0.18% from 0.78% in Q4 of 2011

- Q1 US Export/Import Growth accelerated to -0.01% from -0.26% in Q4 of 2011

Ah, the elixir of a Keynesian life – Exports. Yes, in their textbook it says that if you devalue the currency of a country, you will “boost” exports. Ok, sounds good – but it has not and will not work in the United States of America if the broken promise is to keep doing this with the US Dollar testing 40 year lows.

Consumption and Investment drive the US Economy, not Government and Currency Devaluation. If you perpetuate spikes in price inflation, Consumption will fall. If you perpetuate economic volatility, Fixed Investment will slow.

US Consumption = 71% of US GDP. That’s why gas prices matter so much to real (inflation adjusted) US GDP Growth. Sure, Final Retail Sales Growth rose to +1.6% in Q1, but a lot of that simply has to do with prices at the pump going up. Mistaking inflation for growth has been, and will continue to be, the legacy of Keynesian economic forecasters in the Bush/Obama era.

In order to account for inflation adjustments, the US Government estimates what they call the “Deflator” and subtract that price from what you are paying at the gas station, grocery store, etc.

Look at what the US GDP Deflator has done in the last 2 quarters:

- Q4 2011 Deflator = 0.84%

- Q1 2012 Deflator = +1.5%

You don’t need a Ph.D in applied math to realize that (even if you believe these ridiculously low government “estimates” of inflation in your life) their estimates just almost doubled, on the margin.

On the margin is how real human beings live. It’s also how Globally Interconnected Risk is priced. Paycheck to paycheck, tick by tick – it’s real life for all of us who have to balance a family budget and firm payroll. It’s what most of these conflicted and compromised central planners have never been held accountable to in their working life.

The Fed’s “mandate” = Price Stability and Full Employment. US Jobless Claims just spiked +15% month-over-month (April versus March), and price volatility is plainly evident to anyone with live quotes. It’s time to get real about the credibility of the currency in this country, or we are going to see some serious Capital Flight.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, France’s CAC40, and the SP500 are now $1, $118.94-120.17, $78.66-79.22, 3099-3321, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer