THE HEDGEYE BREAKFAST MONITOR

HEDGEYE VIRTUAL PORTFOLIO POSITIONS

LONGS: JACK, SBUX

SHORTS: DNKN, MCD

MACRO NOTES

Employment

Initial jobless claims came in at 386k versus 370k expectations and 380k the week prior (revised from 388k).

Commentary from CEO Keith McCullough

Futures are up more in anticipation of the 1st“better than expected” US macro data pt in 2 wks (jobless claims), than on “Spain is fine”:

- JAPAN – both Currency and Equities going down now at the same time (this is when it gets more real on the sov debt concern front – at least it has in every other major sov debt crisis – currency leads). Nikkei down -1.1% last night (down for 10 of last 12 days)

- SPAIN – evidently everyone’s a bearish expert again w/ Spain down -13% YTD; bear markets bounce obviously after -19% drawdowns (that’s where the IBEX was pre this bond auction, which came in at higher yields vs last – but being spun by whoever as “better” than “expected” – thank goodness broken sources routinely expect the wrong thing at the wrong time).

- COPPER – no bid this morning – 10yr yields remain below my key TREND line of 2.04% resistance too. Therefore, if you see the pop on the open, and we don’t see a close > 1394 (my immediate-term TRADE line of SP500 resistance), sell.

SP500 down for 8 of last 11 days, so yesterday I moved back to neutral (10 LONGS, 10 SHORTS), but will look forward to considering going back to net short today. Currently no position in SPY, but that’s the most obvious move to consider.

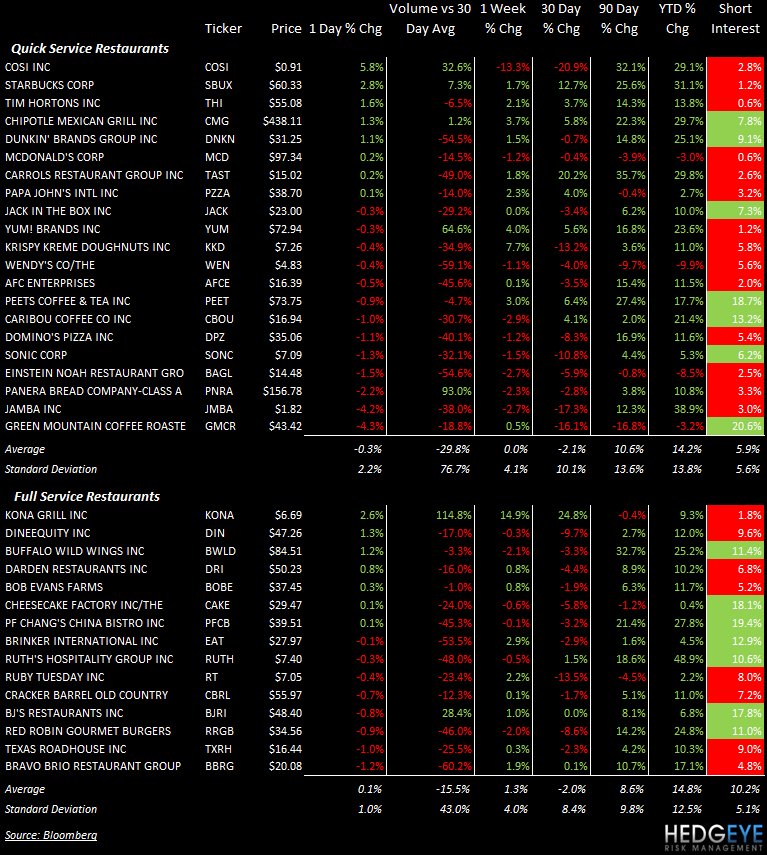

SUBSECTOR PERFORMANCE

QUICK SERVICE

YUM: Yum reported an EPS beat of $0.76 versus consensus $0.73. The negative reaction to the print was largely due to China comps coming in slightly below expectations. U.S. results were above consensus but how sustainable those will be going forward is difficult to say.

YUM: Yum was downgraded to “Outperform” from “Buy” at Credit Agricole. The twelve-month price target is $80. The stock is at $73 right now.

SBUX: Starbucks is continuing to accelerate its plans toward making China its second home market. The company has announced a series of new initiatives aimed at further differentiating Starbucks as the employer of choice in the Chinese market. Included in the initiatives is a new learnings and development concept, Starbucks China University, an institution aimed at elevating the existing learnings and development infrastructure of its employees.

SBUX: Starbucks will introduce the Verismo in China in 2013.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

COSI: Cosi gained on accelerating volume but we are still concerned about the underperformance there.

PNRA: Panera declined on accelerating volume on the news of its COO leaving for Friendly’s.

CASUAL DINING

CBRL: Sardar Biglari issued a letter to shareholders of CBRL calling for the removal of the Chairman and several other members of the board. The letter does not express any confidence on the part of Biglari, who owns 17% of the company, in the company’s performance and ability to improve performance going forward.

Howard Penney

Managing Director

Rory Green

Analyst