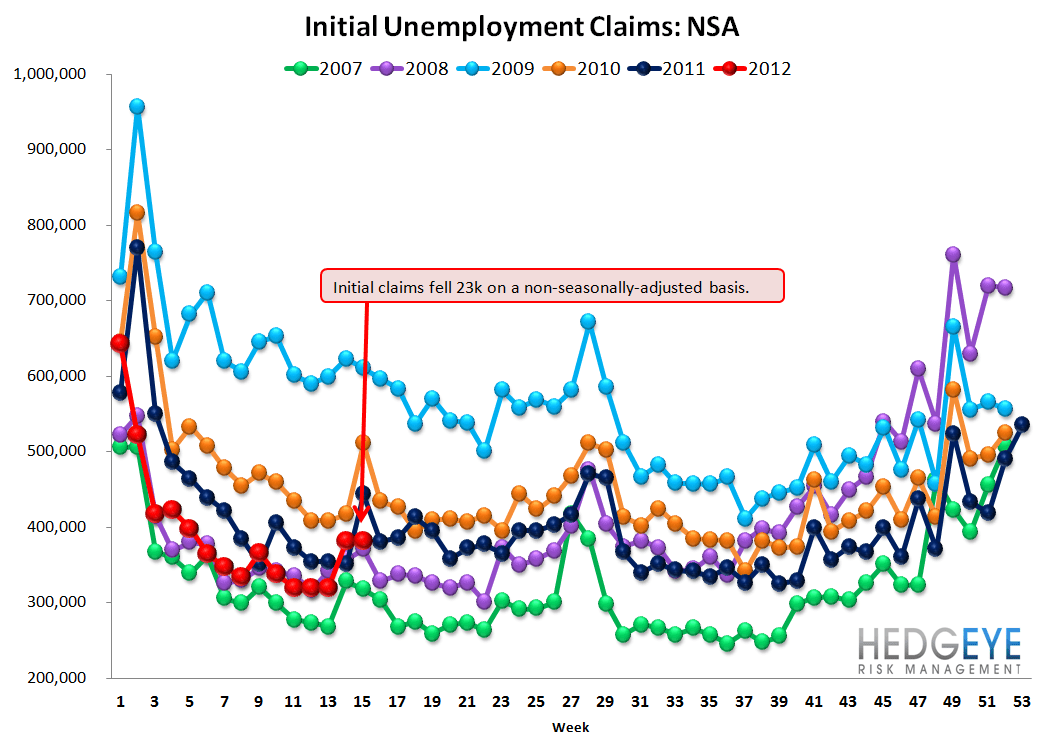

Two Weeks of Spring Break?

Last week we highlighted the uptick in claims being at least partially driven by Spring Break week, in which school bus drivers and cafeteria workers are eligible to collect unemployment benefits. Normally the seasonal adjustment factors appropriately capture this, but last week the adjustment seemed to be off by a week. You can see this in the NSA claims chart below. As such, we had expected this week to be down by roughly 10k, all else being equal. Instead, we got a 6k increase (before the +8k revision). Interesting. Again, looking at the NSA chart below, it seems that somehow those same workers collected benefits for two weeks this year. The bottom line is that even net of these adjustments, claims are rising quickly. In fact, they're rising faster than we would have expected even based on our observation of the faulty seasonal adjustment models the government is using. This suggests that underlying claims may be backing off their intrinsic rate of improvement, i.e. a bona fide deterioration in the jobs market. We'll need to see a few more weeks of data to confirm, i.e. move beyond this Spring Break dynamic, but let's keep a close eye on claims as a leading indicator for domestic employment health.

The headline number for initial claims this week was 386k, this is a 6k increase over the prior week's print of 380k (though a 2k decrease if you factor in the 8k upward revision to the prior week's number: 388k). Larger-than-average upward revisions to the prior week is also a recent trend. Rolling claims rose 5.5k WoW to 375k. On a non-seasonally adjusted basis, claims fell 23k to 368k.

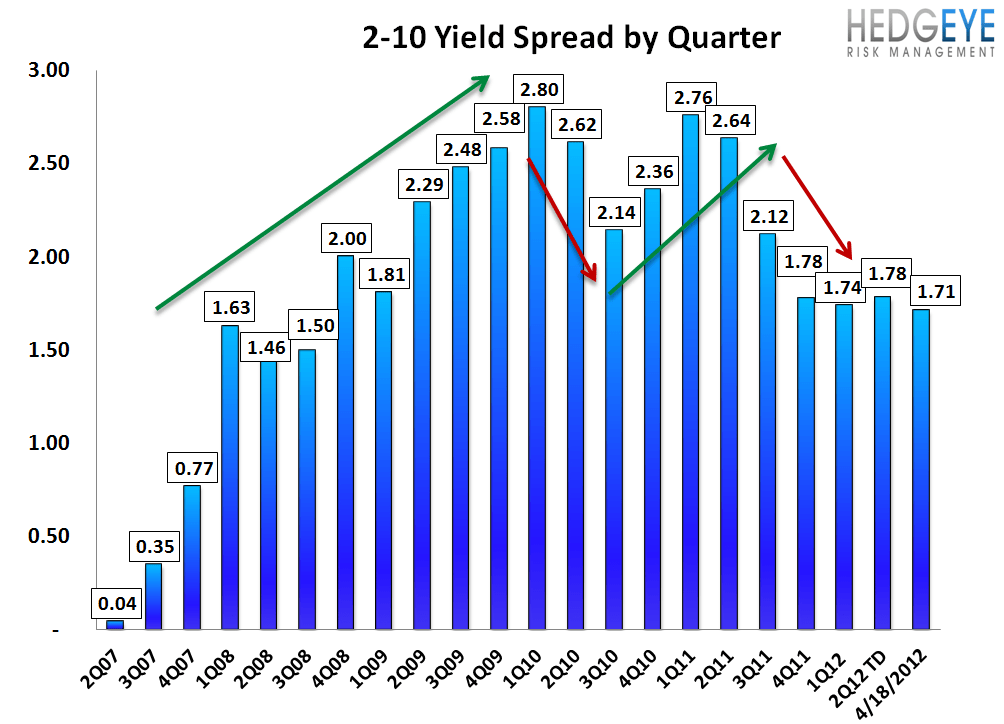

2-10 Spread

The 2-10 spread tightened 3 bps versus last week to 171 bps as of yesterday. The ten-year bond yield decreased 6 bps to 197 bps.

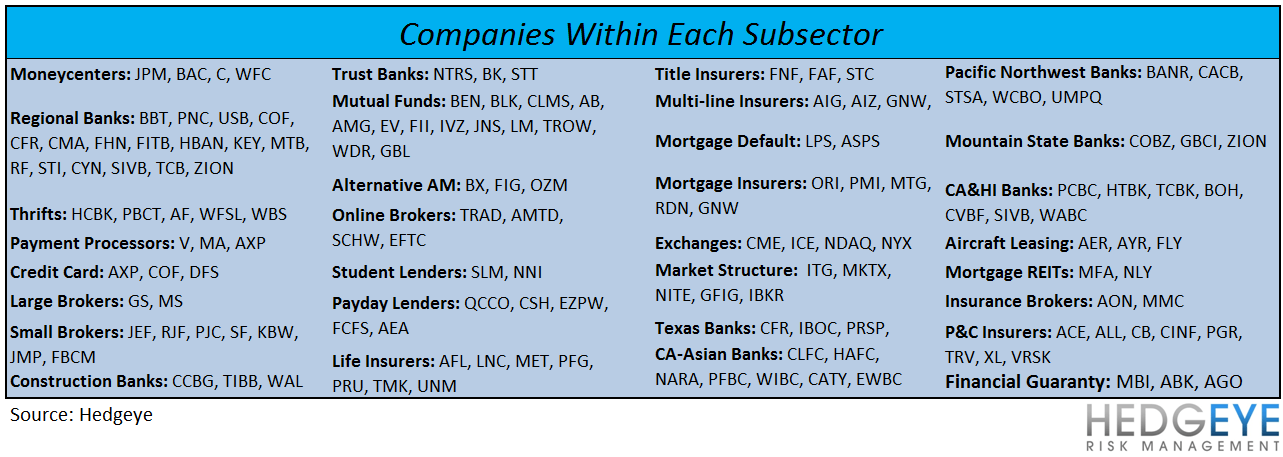

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky