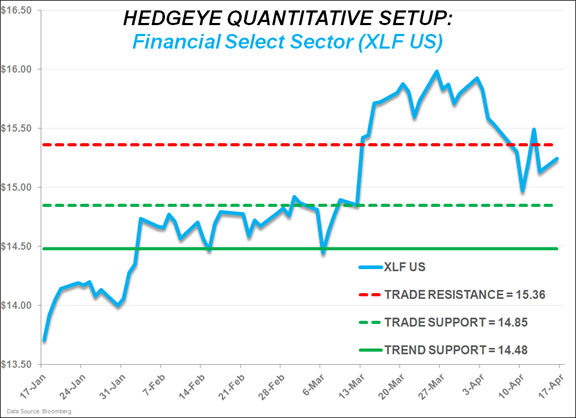

Our financials team, led by Josh Steiner, has provided their key takeaways for earnings in the financial sector this quarter, which are outlined in the bullet points below. Based on our quantitative levels, XLF is bearish on both TRADE and bullish on TREND.

1. Earnings Season Update. Roughly one third of financial companies have reported earnings so far. 7 of the 8 large or mid cap companies have beaten estimates on the bottom line. Revenue trends have been more mixed, with just over 1/3 beating estimates, 1/3 in-line and just under 1/3 missing. However, this is a bit misleading because of Debt Value Adjustment. With DVA, the big banks’ revenue lines are adversely affected by an accounting convention that requires them to recognize negative revenues when their credit default swaps tighten. First quarter saw sizeable CDS tightening, so the headwind was significant for all the large-cap capital markets sensitive names: C, JPM, BAC, GS, MS.

Other notable trends thus far include the regional banks outperforming the Moneycenter banks on both NIM (net interest margin) and loan growth. Regional banks M&T (MTB), Commerce (CBSH) and US Bancorp (USB) have all posted positive sequential loan growth this quarter, while Wells Fargo, JPMorgan and Citigroup have all posted negative growth. On the margin front, we’ve seen the strongest results from the regional banks where NIM has been flat to up quarter over quarter vs. a mixed bag at the Moneycenters with JPMorgan down 9 bps. Market reaction to the results has been roughly evenly split between gains and losses following the reports.

2. Looking Ahead. Financial heavyweights yet to report include Bank of America (BAC), Morgan Stanley (MS), Capital One (COF), American Express (AXP), MasterCard (MA) and Visa (V). Thus far we’ve seen strong first quarter results in both mortgage banking and consumer-related credit, i.e. credit card. Bank of America has sizeable exposures to both these categories, and considering the kitchen sink nature of their 4Q results, we wouldn’t be surprised to see strong results when they report Thursday morning. Morgan Stanley typically mirrors Goldman and JPMorgan, where results were frankly solid, but the reaction in the stocks was lackluster. As a further headwind, Morgan Stanley has less capital markets exposure, which was the source of Goldman’s improvement this quarter.

Looking at the credit card stocks, the playbook is always to look at Discover, as they are off-cycle and so we got their first quarter results a month ago. The big surprise there was much larger than expected reserve release. (Companies release reserves when they believe that credit quality is going to be better in the future than it is today. Released reserves flow through the income statement, adding to reported earnings.) We’d expect to see the same reserve release dynamic at Capital One and American Express. On the card volume side, intra-quarter updates thus far from Amex, Visa and MasterCard have all been reasonably consistent in suggesting activity has been stable compared to strong fourth quarter trends.

3. Sector Outlook. Financials have been among the strongest performing sectors YTD on the back of European discount reflation and an improving perception of the US economic recovery. The calendar also plays a role: distortions to the seasonal adjustment factors have caused the September through February data to look stronger than it is (and the March through August data looks worse) since the bankruptcy of Lehman Brothers. This is a contributing factor to why the XLF, the Financials sector ETF, peaked on February 21, 2011 and lost 35% of its value by October 3, 2011 and why it peaked on April 15, 2010 and lost 23% of its value by August 25th, 2010. For reference, the XLF recently put in a closing high of $15.98 on March 26, 2012. We think there’s a very good chance that this year plays out like the last two years.