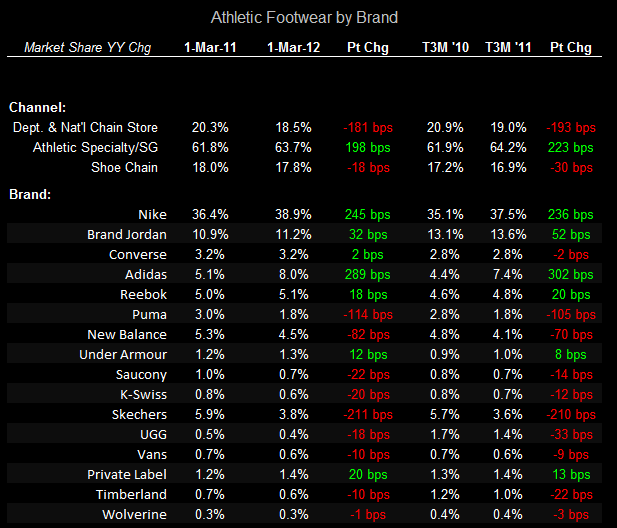

Robust 11% growth in March footwear sales within the athletic specialty channel confirm the anecdote from the FINL 4Q12 call citing March comps up 10% and reaffirms the bifurcation in performance across athletic footwear channels of distribution.

Throughout the month of March, weekly sales growth in industry athletic footwear sales averaged +MSD with ASPs +LSD. In reality, it seems sales were up closer to ~8% with ASP expansion in line with the weekly average. More importantly however, is that the athletic specialty channel continues to outperform the industry average (+11.3% vs. +7.8% in March) as well as the Department store and Shoe chain channels with both unit volume and ASP expansion supporting growth +7% and +4% respectively.

The athletic specialty channel has continued to support increased pricing with ASPs +4% to +6% over the past 3 months. On a call with FINL management Friday morning, the team was optimistic regarding sustainable price increases suggesting customers continued to show no resistance to increases provided the product showed newness and innovation (FINL ASPs were +3% in 4Q12). Similarly, Foot Locker reported customer response to additional price increases as “favorable” through February on the 4Q11 conference call with 2012 comp guidance predicated on both unit volume and continued ASP expansion.

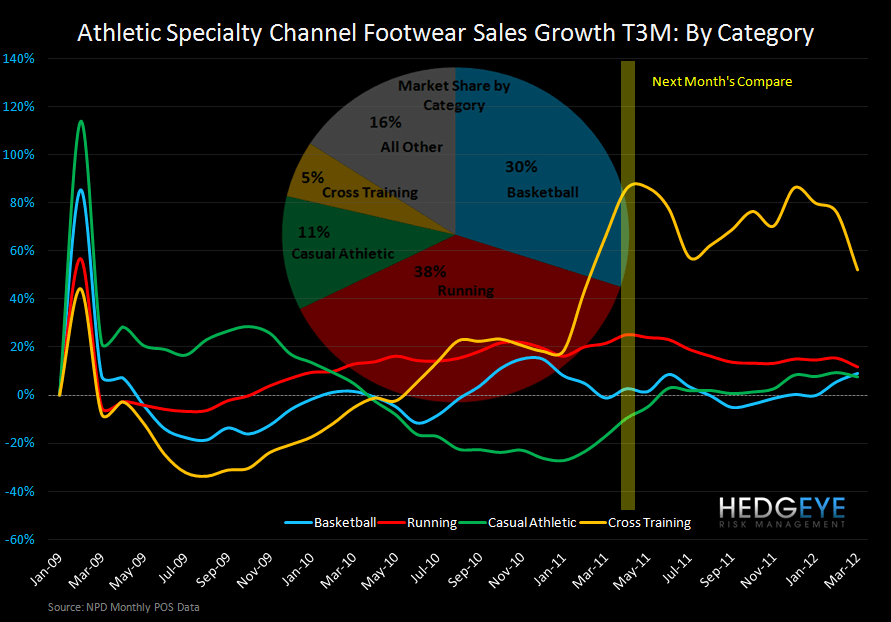

Although we saw a slight deceleration in sales growth in Running and Casual Athletic sales within the athletic specialty channel, sales growth remained up HSD with Basketball (30% of Athletic Specialty FW) improving sequentially. Additionally, should the performance spread across the 3 athletic footwear channels remain pronounced, last week’s industry sales growth of 22% driven by a 21% increase in unit volume suggests the Athletic Specialty channel started April Exceptionally strong. Although we expect weekly sales to slow meaningfully and potentially go negative starting next week due to the Easter tail wind shifting to a head wind (See our note "Athletic Apparel & FW: Easter Headwind Nearing") Athletic Specialty channel sales should remain +LSD.

While near term top line strength is necessary to offset planned capital spending in 1Q13 to support even a 30% decrease in earnings as guided on the Q4 call, we think the FINL risk/reward is favorable for investors with a duration of 1 year or greater.

Matt Darula

Analyst