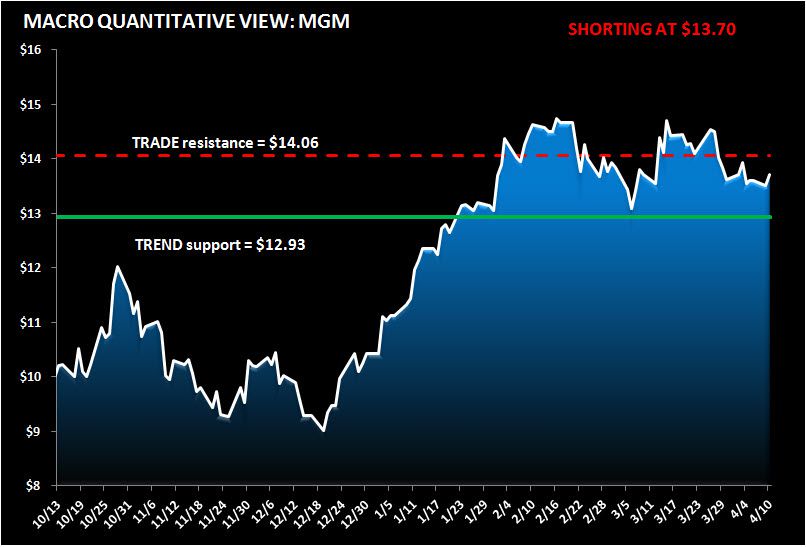

Keith shorted MGM in the Hedgeye Virtual Portfolio at $13.70. According to his model, the TRADE resistance is $14.06 and the TREND support is at $12.93.

While Q1 should be ok, we think the Street's estimates for Q2-Q4 are aggressive. Numbers just released from Nevada for February were in line with our projections while March faces a difficult comp despite 2 extra weekend days. The Q2 calendar is unfavorable and the US jobs picture looks a little bleaker. As it is, we are projecting 15% company wide EBITDA growth for 2012 and we are one of the lower estimates on the Street.