Conclusion: Even if it will not be finalized until he gets all 1,144 delegates, Romney’s nomination as the Republican candidate for President is looking increasingly certain. His road to unseating President Obama is much less certain.

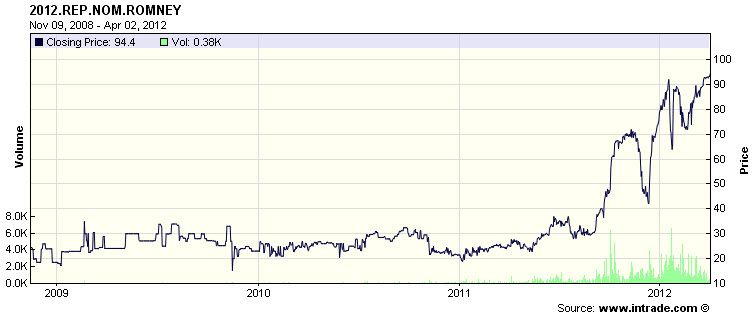

According to InTrade, the electronic predictive market, Mitt Romney is now at a greater than 94% probability of winning the nomination. We’ve posted the chart below previously, but this is the highest probability he’s ever held on InTrade. Currently, based on the delegates that have been awarded, Romney has 566 delegates, Santorum has 263 delegates, Gingrich has 140 delegates, and Paul has 67 delegates. In aggregate, Romney has 163 more delegates than all of his competitors combined.

Interestingly from a popular vote perspective, Romney has been struggling more broadly against the field than either InTrade or the delegate count would suggest. According to the most recent tally, Romney has received 4.1 million popular votes, Santorum has 2.9 million, Gingrich has 2.2 million, and Paul has 1.1 million. Even from a mathematical perspective the road to the nomination simply based on delegate votes for any other candidate is incredibly challenging, the popular vote shares however, do on some level, support the other candidates staying in the race.

Collectively, Romney has only received 39% of the popular votes in the nominating process, which shows that more than 60% of Republican voters have voted for someone other than Romney. The spoiler, so far, has probably been Newt Gingrich who by staying in the race has denied some key votes from the right wing of the Republican Party for Rick Santorum.

This weekend on Meet the Press, Santorum was very clear about his intention to stay in the race when he stated the following:

“If Gov. Romney gets that required number, then without a doubt, if he’s at that number, we’ll step aside. Right now, he’s not there. He’s not even close to it.”

Although there appears to be an ultimate inevitability to the Romney nomination, Santorum is also correct in his assessment as Romney is more than 500 delegates away from the magic number of 1,144 that he will need to clinch the nomination. As noted, Romney’s challenge has been in galvanizing the more conservative components of the Republican Party. Interestingly, we looked at the actual chart of which states he has won and, as the map below shows, Romney has won in the traditionally liberal parts of the country on the coasts, while Santorum has dominated in the middle.

Ultimately, the need for Romney to shift more to the right could come back and haunt him in the main race against Obama. One of the most telling signs of Obama’s momentum against Romney is in recent data from the battleground states. USA Today did a poll of key battleground states from March 22nd to March 26th. The results of the poll show Obama with a statistical significant advantage over Romney at 51%-42% of registered voters. Just a month ago, Obama trailed Romney by two percentage points.

Now clearly this is but one poll, but it does highlight a troubling trend for Romney in these key states versus Obama. The internals are even more disconcerting as they highlight that women, in particular, are moving away from Romney to Obama. In women under 50, Romney is only at 30% support and Obama has almost 2x the support in this demographic based on this battleground state poll. Clearly, this appears to be some backlash against Romney’s shift to the right, in particular related to recent comments to defund Planned Parenthood and his endorsement of an amendment that would allow employers to refuse to cover contraception in health care plans.

A recent poll from Quinnipiac University released late last week provided further validation of Obama’s strength in key swing states. Obama leads Romney 49 to 42 in Florida. In Ohio, Obama beats Romney 47 percent to 41 percent, and he beats Santorum 47 percent to 40 percent. In Pennsylvania, Obama and Romney are locked in a closer race, but Obama still edges Romney 45 percent to 42 percent.

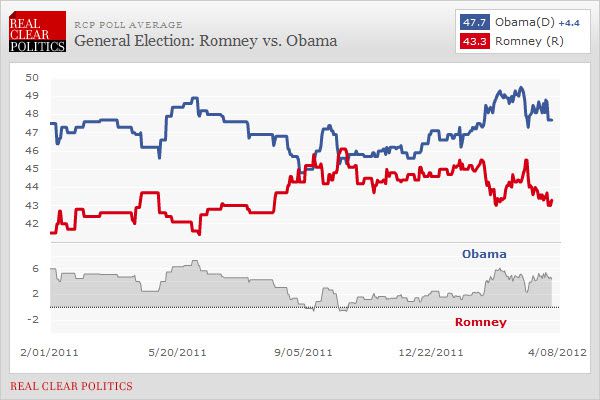

On a head-to-head national poll basis, the story is much the same in Romney versus Obama as in the USA Today Battleground poll. Based on the Real Clear Politics poll aggregate, Obama is at +4.4 spread versus Romney. Further, Romney has only outpolled Obama in 2 of 30 major polls taken since the start of February.

Certainly, a lot can happen between now and the general election, especially with President Obama’s approval rating being mired south of 50 and the price of gasoline escalating across the country. At the same time, Romney is clearly going to have to chart back to the middle so as to not totally lose important demographics like woman under 50. As well, which may be even more critical, he will need to increase his personal likeability, which according to a Washington Post poll shows Romney’s unfavorable rating has soared to an all-time high, leaving him 16 points underwater in the personal approval department.

Daryl G. Jones

Director of Research