This note was originally published at 8am on March 09, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“That the chance of gain is universally overvalued, we may learn from the universal success of lotteries.”

-Adam Smith, The Wealth of Nations

The concept of risk management is, at least for me, a continual learning process. Strictly speaking, what I do is research but naturally when discussing ideas with teammates here at Hedgeye, risk is always on and something that is always foremost in our thinking.

Confidence in the market has increased over the last 6 months and commentary from financial media outlets of all kinds seems to be increasing in its assuredness that the recovery is finally showing some teeth. A notion confirmed today by Bank of America CEO, Brian T. Moynihan, as he suggests that the consumer using leverage again to increase spending. He said “purchases by the bank’s credit and debit-card customers have increased 5%-7% for each of the last five months.” If consumer are levering up again, it is not a positive!

The risk here, clearly, is that the market is attracting those that are trying to chase performance and not what the consensus believes, which is “we have turned the corner.” When thinking through what the reality of our position is, it’s important to always consider two things. First, recall how your counterpart gets paid. Second, it’s paramount to remind oneself that good luck is not a given. Unfortunately, we humans generally believe ourselves to be, individually, held above the rest in the pecking order of fortune. This trait, as Smith puts it, is “an ancient evil remarked by the philosophers and moralists of all ages”. For a contrite buyer of a market top, or the people whose money he or she loses, that is certainly an apt description and something we can all relate to in one way or another.

Looking back on this week it reminds me that there is something to learn every day in this business. Writing this morning piece is something that is forcing me to do something publically that I have tried to do privately at the end of each week, which is assess the week and any lessons that can be taken from it.

Sitting here after the first four days of the week, my macro question is “what is driving this market?”

On Monday, the S&P had its biggest one-day decline of 2012, -1.54%, on the notion that the bailout plan for Greece was going to unravel (a credit event related to Greece looks to be on the cards today). On Wednesday, the improving jobs picture – at least according to the ADP Employment report – helped the market move higher by +0.69%. Yesterday, the market rallied another 1% as private debt holders agreed to convert 85% of Greece’s debt to new securities in the “biggest sovereign debt restructuring in history”.

Ever is a long time and Greece certainly matters, if only because of the possible repercussions in broader Europe in the event of a disorderly default. However, the S&P500 being bid up yesterday despite claims disappointing was interesting.

It is impossible for anyone, least of all myself, to state with certainty why market prices moved in any direction on a given day, but the Wall Street Journal’s report that the Federal Reserve may engage in “sterilized QE” which will please all of the people (inflation hawks and doves) all of the time. Surely, that rumor of Fed intervention abounds anytime the equity market shows any weakness belies the supposed confidence that investors feel in being long this market.

The Hedgeye Financials team has conducted some tremendous research into the initial claims data that is usually so important for market sentiment; much of the recent upsurge in equity prices is attributed to improving employment conditions as shown by the trend in claims.

One would think, then, that a disappointing initial claim print yesterday – albeit one week’s data point – may have had more of an impact on a market that has gained so handsomely in recent months. The “Ghost of Lehman” (as the financials team has called it) distortion in the claims dataset, which has been a headwind and is set to turn into a headwind gradually in the summer months, may have helped boost equity prices over the last six months; the question at this point is whether or not a series of disappointing jobs numbers will lead to a commensurate retracement in the S&P.

That question is perverse to read and it feels perverse to write. Surely deterioration in the underlying fundamentals, especially the all important jobs picture, should lead to a sell off. The S&P is up 8.6% year-to-date and up 102% from the March2009 low. Still, with the QE is the go-to strategy the instant any “concerns” creep into the market, will a pause in the jobs picture have any impact on equity prices at all?

What’s increasingly difficult to discover at this point is truth. The truth is not always beautiful, as Lao Tzu wrote. In the case of our financial “markets”, the truth would likely be downright ugly. Maybe a truth, as Jack Nicholson might say, that we couldn’t handle. My aim is not to vilify actors in or prescribe solutions for the ills facing our economy. As a equity analyst, looking back on this past week and thinking about the pending jobs report, my conclusion is that the rumors of intervention by central banks is deterring people from truth and thus market prices might not reflect reality.

Even in vain, the quest for truth must be sustained. Yesterday was cheering on inflation - Dollar down, Euro up, oil up, gold up, and XLI and XLB were the best performers. It’s the type of move that has corroborated many of the points that our Macro team has argued recently. First, inflation slows consumption. McDonald’s – one of the most macroeconomic-immune companies of the past four years – mentioned inflation as an issue for its business in its press release yesterday. Second, at this point investors need to embrace uncertainty and stay nimble. With the VIX at 17, there is plenty of complacency in the market that “we have turned the corner” and not reflecting increased inflation.

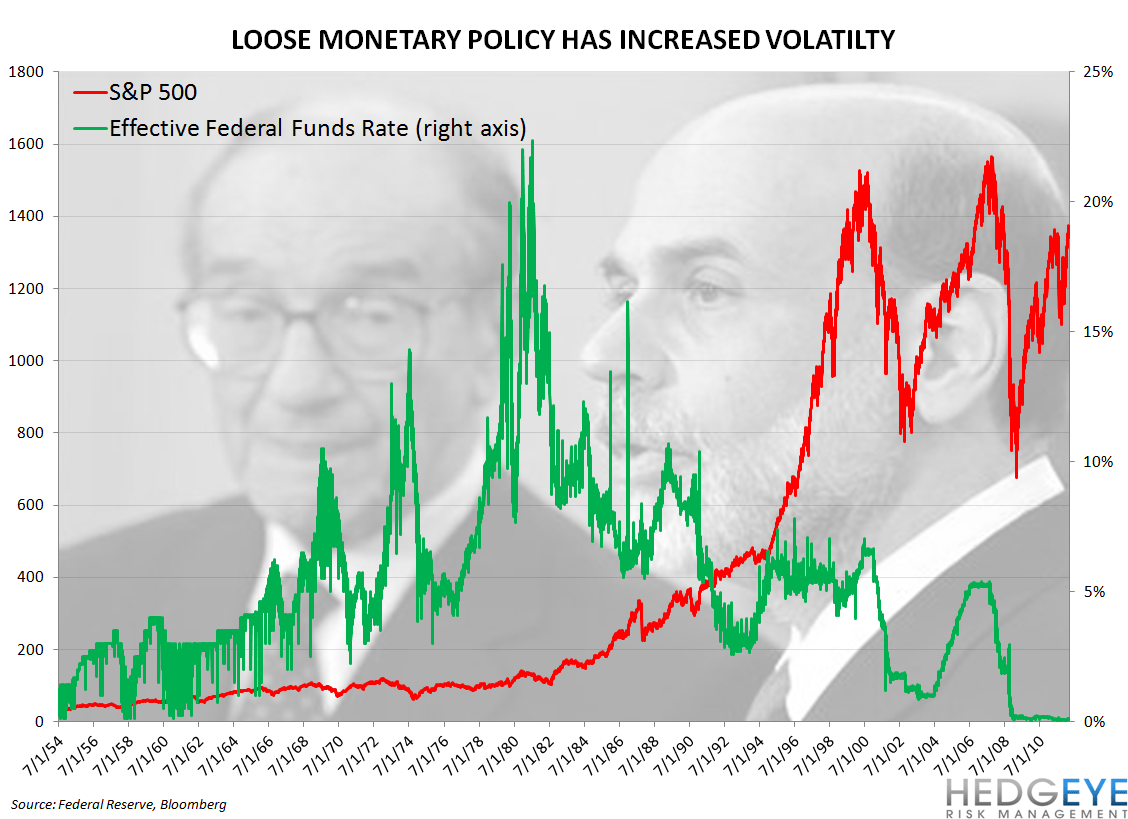

If good news is good and bad news is QE, surely the only way is up! Looking at a simple chart of short term interest rates versus the S&P shows that the frequency and amplitude of stock market cycles has increased coincident with the implementation of easy money policies. The lack of truth in financial markets is rendering trust impossible and that is illustrated clearly in the volatility of the past few years. As buyers up here, it is worth asking whether or not we are overvaluing the chance of gain.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, and the SP500 are now $1692-1717, $123.98-126.89, $79.02-80.12, and 1345-1382, respectively.

Function in Disaster; Finish in Style

Howard Penney