THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Consumer

Initial jobless claims came in at 348k versus consensus 350k and 353k the week prior (revised up from 351k).

Commentary from CEO Keith McCullough

Got global Growth Slowing? Markets are starting to:

- INDIA – Energy stocks (XLE) stopped making higher-YTD-highs on Feb 24 and India stopped going up on Feb 21; this morn India’s Sensex was down another -1.8% on fundamentals (Growth Slowing As Inflation Accelerates) and is down over 6% from its YTD high. India’s Yield Curve has pancaked.

- SPAIN – Growth Slowing was the most obvious message for the PMI reports across Europe for the month of March. Central Planners can arrest stock market deflations in the short-term, but in the long-run, their ideas to stop economic gravity are dead. Spain’s IBEX remains bearish across all 3 of our risk mgt durations (down -1.5% this morn)

- OIL – probably the only good news this morning is that Oil stopped going up. We sold our long Oil position and took our asset allocation to Commodities to 0% because the US Dollar looks like it could put on a big move to the upside again. Immediate-term support lines that broke for WTIC and Brent are $106.79 and $124.89, respectively.

Deflating The Inflation takes more time than a day. Tops in Energy and Basic Materials stocks are processes, not points. I shorted FCX yesterday too.

KM

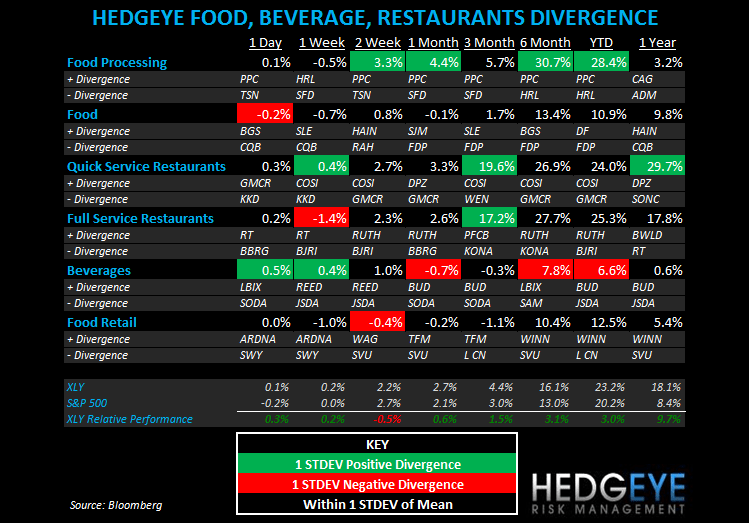

SUBSECTOR PERFORMANCE

QUICK SERVICE

MCD: McDonald’s CEO Jim Skinner is stepping down to be replaced by COO Don Thompson effective July 1.

SONC: Sonic reported 2QFY12 EPS of $0.03 versus $0.02. Company same-store sales were in line with preannounced results of 3.1% but 1% of that was due to the extra day in February due to the leap year and there was some favorable weather impact also. Sonic continues to perform inconsistently, from an operational perspective.

SBUX: The Starbucks AGM was another success for the company yesterday. FY12 guidance was unchanged. The company offered interesting commentary on international markets including the potential of drive-thrus in Europe as well as an initial look at its new Evolution Fresh concept. Oppenheimer raised its PT on Starbucks this morning to $62 from $56.

WEN: Wendy’s is releasing a new Spicy Chicken Guacamole Club. From a mix perspective, this product could help the company alleviate pressure from beef costs, although the price point was not disclosed.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

GMCR: Green Mountain gained 10% on accelerating volume as the company announced its agreement with Starbucks yesterday to expand their partnership to make, market, distribute and sell Starbuck’s Vue coffee packs for use in Green Mountain’s Keurig Vue single-cup machines.

KKD: Krispy Kreme stocks plunged after the company reported a 4QFY12 earnings miss on Tuesday.

COSI: Cosi gained on accelerating volume – again.

CASUAL DINING

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

RT: Ruby Tuesday shares gained on accelerating volume following Raymond James’ upgrade yesterday.

Howard Penney

Managing Director

Rory Green

Analyst